More than two dozen trade groups have called for the reduction or elimination of loan-level pricing adjustments (LLPAs) on Fannie Mae and Freddie Mac loans, a move that could push mortgage rates even lower than they already are.

Put simply, mortgages lenders rely on risk-based pricing to set the eventual mortgage rate you receive. So all else being equal, a borrower purchasing a single-family home with 40% down will receive a lower interest rate than an investor purchasing a four-unit property with 20% down.

It makes sense to charge borrowers a higher interest rate if they present more risk of default, despite the fact that a higher interest rate may actually lead to an increased risk of default. That’s just the way it is.

But powerful groups like the Mortgage Bankers Association, the National Association of Realtors, and many more want to reduce or eliminate LLPAs going forward, per a recent letter to FHFA boss Mel Watt.

LLPAs Can Raise Effective Mortgage Rates Significantly

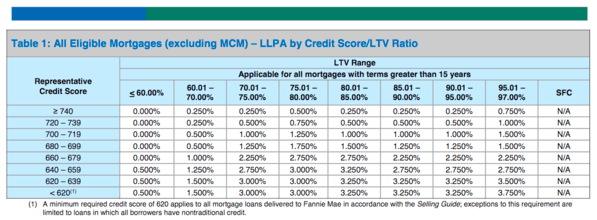

As mentioned, LLPAs affect the final mortgage rate a borrower receives. So a borrower with a 620 credit score purchasing a home with just 3% down via Fannie Mae’s 97% LTV offering may get hit with a 3.5% pricing hit to compensate for that risk.

That adjustment alone may increase their interest rate by around 1% or more. Generally, these pricing hits are built into the interest rate and a pricing hit of 1% may translate to a rate increase of 0.25% or so.

The groups argued in their letter that the LLPAs could total up to 4% of the loan value for some borrowers, which seem to hit first-time home buyers, along with low- and moderate-income buyers, the most.

Part of this phenomenon could be attributed to the fact that new buyers don’t know the rules of the game right off the bat, and often apply for mortgages with poor credit or a limited down payment.

The result is a much higher interest rate than wealthier buyers, or those with better credit and more to put down, such as move-up buyers.

At the same time, Fannie and Freddie have increased g-fees by roughly 164% between 2009 and 2014, another fee that is typically passed along to the borrower via a higher interest rate.

Together, this means higher effective mortgage rates for borrowers, despite the massive declines seen since the financial crisis nearly 10 years ago.

Tip: What mortgage rate will I receive with my credit score?

Mortgage Quality Pristine, Yet Fees Continue to Be High

The general argument is that mortgage quality couldn’t be better, yet Fannie and Freddie continue to charge (and raise) fees for the loans they purchase and securitize.

You would think in light of better loan quality and lower defaults they could ease some of these loan-level fees, but that has yet to be the case.

And these groups believe it’s gotten so bad that some qualified borrowers are being “priced away” from conforming loans and ostensibly into cheaper government loans such as FHA.

The issue is especially touchy seeing that these LLPAs generate enormous profits for Fannie and Freddie, which are under government conservatorship and shouldn’t really be raking it in.

Their implied goal should be to promote homeownership and ease credit for a large swath of borrowers, at least, that’s the theory.

And thanks to strong mortgage underwriting, enhanced mortgage insurance capital requirements, and improved reps and warranty framework, Fannie and Freddie should be comfortable enough to adjust their pricing policies.

But Would This Invite More Risk?

The counterargument here is that risk-based pricing is a necessary evil in the mortgage space (and elsewhere) that reflects borrower quality. After all, a mortgage borrower with a 620 credit score probably has a higher chance of default than a borrower with an 820 credit score.

Same goes for down payment size – the borrower who puts down 40% is likely less risky than the borrower putting down 10%. And interest rates have to account for that.

Sure, you could offer everyone the same rate and thus lower monthly mortgage payments for the riskier band of borrowers, which could effectively lower default rates.

But it could usher in new risk if borrowers are given ultra-low interest rates despite exhibiting high-risk borrowing attributes.

It could also promote hazardous lending because there wouldn’t be any downside to putting next to nothing down, or for maintaining poor credit.

At the same time, there wouldn’t be any upside for borrowers to be more conservative in their borrowing habits. They could essentially buy more home if they put less down and make speculative investments with greater ease.

Not to mention that interest rates are already close to new record lows, so arguing to lower them even more at the moment might seem a bit ill-timed. Perhaps they could lower LLPAs to align with today’s risk, but eliminating them entirely seems shortsighted and dangerous.