While browsing the web the other day, an ad popped up on the screen for a company called EquityKey.

Normally I’m not too moved by banner ads, but this particular ad aligned nicely with the type of stuff I talk about on my blog.

In a nutshell, EquityKey allows homeowners to tap into the equity in their property without taking on a monthly payment.

It’s kind of like a reverse mortgage (for senior citizens), but works quite a bit differently because it’s tied to future home price appreciation.

How EquityKey Works

I dug into the details on their website to see how the program actually works.

As noted, in exchange for a share of your home price appreciation, the company will provide you with an upfront lump sum payment.

This upfront payment is not a loan, meaning no interest is collected and no monthly payments are due, but it does need to be paid back when you sell.

Additionally, you will part with anywhere from 30% to 75% of future appreciation, so it can obviously cost you quite a bit to cash in today.

You can receive up to 17.25% of your property’s current value, so for a home valued at $500,000, the max you could receive would be $86,250.

With a typical home equity line of credit or second mortgage, you’d have to make a monthly payment on the loan balance each month. However, when it came time to sell your home, you’d keep all the equity less the outstanding loan(s).

How Your Property Is Valued

With EquityKey, you avoid the monthly payments but part with appreciation, which is measured using the S&P/Case-Shiller Home Price Index.

When you make an agreement to share your equity, EquityKey will take the designated index for your property location and use that value as the Beginning Index Value for the transaction.

Your home will also be appraised at the time of taking out the equity, and these two figures will determine how much appreciation EquityKey receives when you sell.

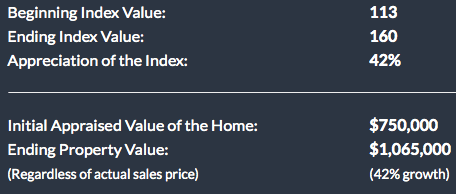

The example posted on their website features a San Diego property appraised at $750,000 with a Beginning Index Value of 113 in the year 2000, per S&P/Case-Shiller data.

When the hypothetical property was sold in 2012, the Ending Index Value was 160, representing a 42% increase.

EquityKey would receive whatever percentage of appreciation you allocated when you made the original agreement with them.

This is regardless of what you actually sell your house for. So you are basically incentivized to take care of your property so it fetches a good sales price, and doesn’t underperform the index.

Additionally, you are entitled to the equity beyond the index value of your home. In other words, if that hypothetical home in San Diego sold for $850,000 because of a hot real estate market and pristine upkeep and/or improvements, that $100,000 belongs to you.

However, if that same home were to sell for just $700,000, you’d still be on the hook for the $750,000 valuation. Clearly this could make selling a bit more difficult.

There’s also a pretty important caveat. If you sell, transfer, or change ownership in the first six years after your agreement with EquityKey, the so-called “Minimum Settlement Amount” will apply.

It’s a little unclear what this amount is, but I believe it’s the amount they originally paid you, plus a fee to cover origination and investment return if appreciation isn’t large enough to cover those costs.

My Thoughts

At the end of the day, this sounds like a fairly expensive way to tap into your equity. Sure, you don’t have to make payments each month, but you also part with a good deal of your home price gains, which is one of the major benefits of owning a home.

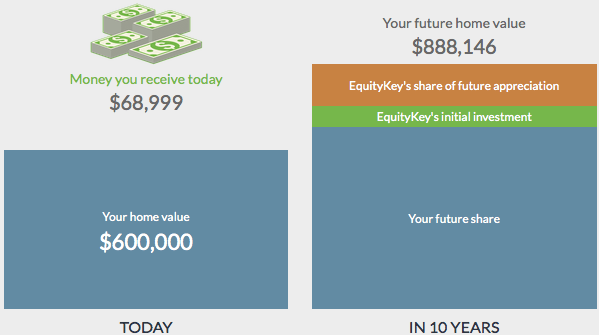

In the illustration above, you’d get $68,999, but you’d have to pay that back and part with $144,073 in home price appreciation, which is 50% of the projected gain over 10 years.

So it might make better sense to just go with a HELOC or a standard cash-out refinance if you can handle the increase in monthly payments. The interest expense would likely be much lower than the appreciation given up.

This product could make sense for someone unable to pull equity via the traditional methods, or perhaps for someone lacking income to make monthly payments, assuming they really needed the money.

And I suppose a homeowner could “win” if their home value went down because EquityKey won’t take a cut if that’s the case, nor require repayment if the home value drops by more than the payout you originally received.

But the chances of that are probably slim, and you’d have to question why you would stay in a home if the value were destined to drop big time.

EquityKey Program Details

[checklist]

- You can receive up to 17.25% of property’s current appraised value

- You part with 30-75% of future appreciation

- Primary residences and second homes are eligible

- Max LTV/CLTV at time of application is 80%

- No underwriting or origination costs, but third-party costs still applicable

- Takes roughly 4-6 weeks to fund

- You can refinance, but typically not above 60% LTV

- Might pay a fee if you sell in less than six years

[/checklist]

Not included in this article is the fact that these guys go after elderly people who often have little understanding of the terms of the agreement. In finance these type of “lenders” are called bottom feeders, they target people who are elderly, not tech savvy, have assets but are unaware of the options they have for tapping into them. If they contact one of your elderly relatives it would be wise to step in and educate them on alternatives. There is very little that is beneath these guys. They have had these types of arrangements in the UK and Europe, but the laws protecting the elderly from financial predators are much more robust than they are in the US