In an effort to boost home loan lending to lower- and moderate-income borrowers, Fannie Mae has created a new program called “HomeReady.”

Fannie didn’t release all the details yet, but they expect to roll out the program later this year, integrating it with their automated underwriting system Desktop Underwriter (DU).

What we do know is that the program will automatically flag potential borrowers for inclusion in the program by utilizing the DU findings.

This means borrowers who would otherwise be denied a mortgage might actually qualify thanks to the expanded guidelines offered via HomeReady.

Additionally, lenders will be able to underwrite the loans with more certainty knowing that they won’t violate Fannie’s guidelines, potentially leading to costly buybacks.

HomeReady will eliminate or cap certain loan level pricing adjustments (LLPAs) such as those associated with credit score, LTV, and so on.

That should translate to a low mortgage rate for a traditionally higher-risk borrower, which should actually boost their chances of staying current on the loan.

That strange dilemma has always caught my attention and made me think – higher risk borrowers are charged higher interest rates, thereby creating costlier payments that are in essence more difficult to pay each month.

But you can’t have it any other way, unless there are programs like this around. Maybe that’s the point.

Anyway, in exchange for the lower rates, borrowers taking part in HomeReady will need to complete a mandatory online education course called Framework, which should prepare them for the home buying process and provide post-purchase support. It costs $75.

The course meets the standards of the National Industry Standards for Homeownership Education and Counseling and the HUD Housing Counseling Program.

HomeReady Allows Non-Borrower Household Income

Now onto some of the HomeReady Mortgage details that are noteworthy. For what Fannie calls the “first time,” a non-borrower household member’s income can be considered when determining the borrower’s DTI ratio.

This appears to be aimed at multi-generational and extended households that Fannie claims, “have incomes that are as stable or even more stable than other households at similar income levels.”

HomeReady will also allow income for non-occupant borrowers, such as parents of a borrower, to be used to supplement qualifying income.

The program is available to both first-time home buyers and repeat homeowners, and only requires a 3% down payment, an option now available to all Fannie Mae borrowers.

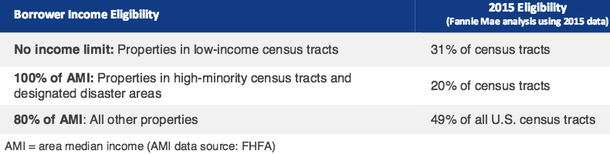

However, there are some income limits tied to this new program.

If the property is located in a designated low-income census tract, HomeReady will be available to borrowers at any income level.

Additionally, properties in high-minority census tracts or designated natural disaster areas will be eligible for HomeReady financing at or below 100% of area median income (AMI).

For properties that aren’t in these census tracts, HomeReady borrowers can only have an income at or below 80% of the AMI.

Fannie estimates that roughly half of census tracts nationally will be subject to the 100% AMI limit or have no income limit at all.

In any case, there are already maps posted on the Fannie Mae website that detail the income limits (or lack thereof) from state to state.

Additional details will be disclosed to lenders in coming weeks via a Selling Guide announcement, with Desktop Underwriter inclusion and loan deliveries expected in late 2015.

HomeReady Mortgage Program Highlights

[checklist]

- Automated identification of HomeReady-eligible loans via DU

- Risk-based pricing waived for borrowers with LTVs >80% and credit score >=680

- LLPA cap of 150 basis points for loans outside the parameters above

- 3% minimum down payment for purchases

- 95% max LTV for limited cash-out refinances

- No minimum borrower contribution (on 1-unit properties)

- Cash on-hand acceptable as source of funds for down payment and/or closing costs

- Income from non-borrower household member allows DTI ratio of 45-50%

- Non-occupant borrowers also permitted

- Reduced MI coverage requirement above 90% LTV

- Homeownership education course mandatory

- HomeReady loans can be bundled with standard loans in same MBS pools and whole loan commitments

[/checklist]

My husband and I are looking into this loan. The house we are looking at is 3/4 mile outside the “no limit” zone, which is an 80% ami eligibility zone. He just happens to make 81%. Do they underwrite these guidelines or is it a pretty strict line?

Holly,

Not sure because it’s so new, but maybe an exception can be made if it’s that close. Good luck!

Interesting post – I loved the specifics – Does anyone know if my business could possibly acquire a sample Fannie Mae Guide Underwriting DU copy to complete ?