While prospective home buyers continue to grapple with high mortgage rates and limited supply, existing owners are getting richer.

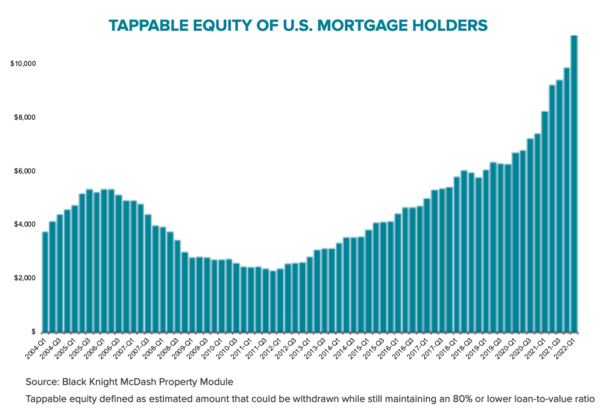

A new report from Black Knight revealed that the average American homeowner is sitting on more than $207,000 in tappable equity.

The phrase “tappable equity” means an amount that leaves a 20% equity buffer in place, aka 80% loan-to-value (LTV).

This is generally what banks and mortgage lenders will allow homeowners to borrow to ensure they have some skin in the game.

The question though is how do you tap into that equity, especially in a rising rate environment?

Does a Cash Out Refinance Still Make Sense?

- Mortgage holders withdrew more than $75 billion in the first quarter of 2022 via cash out refinances

- The cash out refinance share jumped to 75% during Q1 as rate/term refis waned

- Early Q2 data suggests higher mortgage rates will dampen demand going forward

As noted, American homeowners are sitting on a staggering amount of available home equity.

At last glance, it was over $11 trillion, or roughly $207,000 per mortgage holder.

That figure is up from $127,000 at the start of the pandemic, and more than 2X the levels seen back in 2006 during the prior market height.

Here’s the problem though – mortgage rates have also basically doubled since the start of the pandemic, making a refinance a tough sell.

Still, cash out refinance volume doubled over the past 12 months, with such loans accounting for 75% of all refinances in the first quarter of 2022.

That was up from a 61% share in the fourth quarter of 2021 and 36% from a year earlier.

Of course, refinance lending overall was down 54% in the first quarter from the same period a year earlier, thanks to an 80% drop in rate/term refis.

Meanwhile, cash-out refis were off just 4% on an annual basis. However, the number of transactions fell for the second consecutive quarter, and growth in overall equity withdrawals slowed.

Ultimately, a cash out refinance won’t make sense for a lot of homeowners if their existing mortgage rate is in the 2-3% range.

Sure, it’s nice to tap into that equity, but not if you have to replace your first mortgage rate with a 5-6% interest rate.

What About a Second Mortgage, Such as a HELOC or Home Equity Loan?

The alternative a lot of borrowers are looking at now that mortgage rates are no longer on sale is a second mortgage.

Banks and mortgage lenders are also ramping up their offerings to account for this trend.

There are basically two main options available to homeowners; a home equity line of credit (HELOC) and a fixed-rate closed second.

The HELOC works similarly to a credit card in that you can borrow only what you need, pay it back over time, or simply keep it open for a rainy day.

The downside to the HELOC is that it features an adjustable interest rate, which is tied to the prime rate.

Whenever the Fed moves rates higher, the prime rate will go up by the same amount.

The Fed is expected to raise rates .50% in June and July to tame inflation. This will translate to a 1% increase in HELOC rates.

Of course, they might be done after that, and if the economy goes into a recession, they could turn around and lower rates too.

So HELOCs might have a somewhat telegraphed price assumption over the next year or so.

If you are risk averse, there’s the home equity loan, which allows you to borrow the full amount at closing.

You get a lump sum of your equity, but no additional draws in the future. The upside is that the interest rate is typically fixed.

The downside is that the interest rate is likely higher than a HELOC to account for the fixed rate advantage.

And as noted, you borrow the full amount, whether you need it or not. This means paying interest on the full amount.

Still, either option may be advantageous to a cash out refinance, which disrupts your first mortgage.

Use a Home Equity Sharing Company?

There are also so-called “home equity sharing companies” where you trade a portion of future home price appreciation for cash today.

One such company in this emerging industry is Point, which allows you to get payment-free cash.

However, you do give up a share of your (hopefully) rising property value in exchange, and they charge an upfront transaction fee that is deducted from your proceeds.

The cost of borrowing then depends upon when you pay it back, via home sale, refinance, or simply buying them out. And how much your property appreciates during that time period.

There was a similar company called Noah, which paused applications a while back. It’s unclear if they’ll resume lending at some point.

Other names in the nascent field include Hometap, Unison, and Unlock.

Personally, I don’t love the idea of giving up future gains, especially when they’re unknown. But it’s an option nonetheless.

Seniors Can Consider a Reverse Mortgage to Tap Available Home Equity

One final option to consider, assuming you’re a senior (62+) is the reverse mortgage.

Not only does it allow you to tap your available home equity, but it also comes with no monthly payments.

This is obviously a plus if you’re retired or close to retirement and want to keep your home, but need cash.

It may also be easier to qualify for a reverse mortgage versus a traditional mortgage, especially for fixed income borrowers.

Like the options discussed above, it’s possible to take out a reverse mortgage as a line of credit, or opt for a lump sum payout.

Additionally, you can opt for an adjustable-rate mortgage or a fixed-rate mortgage. So there’s lots to consider.

There are pros and cons to all those options, and which one you choose will be based on your individual needs and risk appetite.

Reverse mortgages can be more complicated than a traditional mortgage, so shopping around could come with the added benefit of education.

It may also allow you to see more loan program options and scenarios to choose from, including proprietary offerings.

To sum things up, it’s not nearly as cheap as it was just a few months ago to tap your home’s equity, but there are still opportunities on the table.

Take the time to educate yourself about each to determine which, if any, is best for you.

Read more: Cash Out vs. HELOC vs. HEL