If you talk to most interested parties, whether it’s a real estate agent, a home builder, or someone else who stands to make money from your decision, they’ll probably tell you that it’s always a good time to buy.

In fact, that it’s a great time to buy. That real estate always goes up, and even if there are some near-term hiccups, the trajectory is clear. Up.

And they could be sort of right. If you look at long-term home price charts, values rise over time, despite downturns here and there. Can’t argue with history…

There Are Better and Worse Times to Buy Real Estate

However, one thing is abundantly clear. There are certainly better and worse times to buy a piece of real estate.

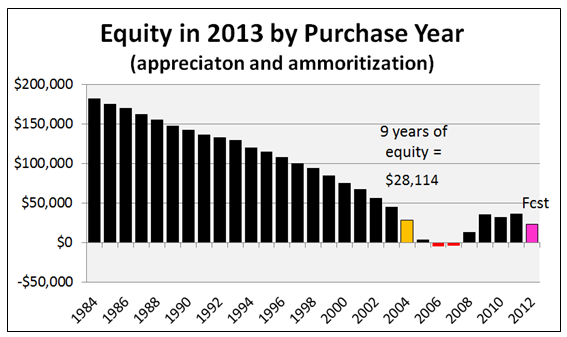

Case in point, this chart from none other than the National Association of Realtors, the perennial cheerleaders of real estate.

It shows the home equity a buyer of a median priced home would have accrued based on purchase year.

The chart starts in 1984, which is 30 years ago. Most mortgages have 30-year terms, so for the individual who kept their original mortgage and paid it off, they’d be free and clear.

[Should I pay off my mortgage or invest instead?]

They’d also own a property that would have appreciated somewhat significantly, even with occasional pullbacks, including the latest severe drop in home prices.

Additionally, inflation would make their home equity appear even greater. For this buyer, it was a good time to buy and hold. They probably have a nice little nest egg.

Conversely, let’s look at NAR’s example, which is a borrower who purchased a median-priced home back in 2004 and held it for nine years, which is the median tenure of a homeowner per the group’s annual Profile of HomeBuyers and Sellers.

For the record, their calculations assume a 10% down payment and a 30-year fixed mortgage payment at the average prevailing rate.

Their hypothetical buyer would have accrued just $28,114 in equity over nine years from both home price appreciation and paying down the mortgage principal with regular monthly payments.

While it’s certainly better than being underwater, which the average 2006 and 2007 buyers are, it’s not nearly as good as the recent buyer.

They compare the 2004 buyer to one who purchased a median-priced home in 2012, who would already have accrued more than $23,000 in home equity through price gains and regular mortgage payments.

Not only that, but the average 30-year fixed mortgage rate in 2004 was 5.84%, compared to 3.66% in 2012, per Freddie Mac.

So the more recent buyer would be paying far less interest and a lot more principal each month, which means more home equity faster.

In summary:

2004 buyer: $28,114 home equity (5.84% mortgage rate)

2006 buyer: negative equity

2007 buyer: negative equity

2012 buyer: $23,000+ home equity (3.66% mortgage rate)

Based on these numbers, it doesn’t always appear to be a good time to buy real estate. Or more specifically, there are better and worse times to buy a home.

In NAR’s own words, even after going through a massive recession, “housing remains an effective vehicle for building equity and wealth.”

Their argument being that time heals all wounds…after all, eventually every one of these buyers will have positive home equity, no matter when they purchased.

Read more: How to build home equity.

Props for writing this post. Most in the industry would afraid to make this declaration, but it’s absolutely true and should be shared.

I second that. Real estate agents and mortgage lenders push people to buy homes even when it makes no sense.

Depends what you mean by “good.” If you want to own and like a particular house a lot, you’ll probably be happy you bought, even if prices dip some after purchase.