This morning, the House Financial Services Committee heard testimony from five housing industry leaders regarding the new QM rule.

The hearing, titled, “How Prospective and Current Homeowners Will Be Harmed by the CFPB’s Qualified Mortgage Rule,” essentially allowed “witnesses” to vent about the new mortgage rules that went into effect on January 10th.

What stood out the most to me was a comment made by Bill Emerson, CEO of Quicken Loans, who spoke on behalf of the Mortgage Bankers Association (MBA).

He made a number of claims, but perhaps the most noteworthy was his assertion that non-QM loans have mortgage rates 4-5% higher than QM loans.

Emerson said certain rate sheets he received indicated that non-QM loans cost “significantly more,” unless they’re for low-default/high credit quality borrowers.

Rates Between 8-10% for Non-QM

Assuming the standard 30-year fixed is pricing around 4.5%, a non-QM 30-year fixed would go for between 8.5% and 9.5%, or even higher if the loan was deemed higher risk for whatever reason.

Such loans would also require very high down payments or significant home equity to gain approval.

Clearly this pricing isn’t going to lead to very many QM loan closings, which is why so many industry participants are against the new rule as it stands.

Emerson also noted that many jumbo loans wouldn’t qualify for the QM distinction because DTI ratios often exceed 43%.

However, because these borrowers tend to have great credit and abundant assets, he believes jumbos will still be available in the non-QM market at competitive rates.

Unfortunately, this could lead to unintended consequences, as wealthier borrowers will receive more favorable terms and better access to credit, raising fair lending concerns.

“The solution is to broaden the availability of QM loans to low- and moderate-income borrowers,” he testified.

“In addition, the CFPB should develop means for jumbo loans to be treated as QMs if, for example, they meet agency standards although they are not eligible for purchase.”

The QM rule allows loans that exceed 43% DTI so long as they are approved by Fannie Mae and Freddie Mac. This exception is scheduled to remain intact for seven years.

Max Points and Fees Under QM Also a Problem

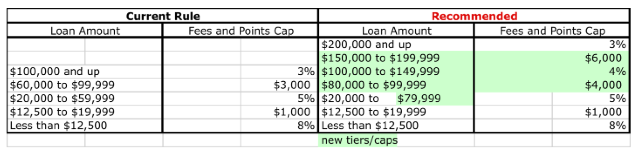

Emerson also took issue with the cap on points and fees, especially with smaller loan amounts.

As it stands, the QM rule allows up to 3% in points and fees on loans of $100,000 and up.

He argued that for loan amounts above $100,000, but still smaller than average, the cap will likely be exceeded, pushing the loan out of the QM realm.

As a result, many low- and moderate-income borrowers will be hung out to dry. As an alternative, he’d like to see higher points/fees thresholds at smaller loan amounts, as pictured above.

Another issue related to the cap on points and fees is that third party charges for things like title insurance and other settlement costs are exempt unless they’re paid to an affiliate of the lender.

Quicken has a lot of affiliates it works with to provide these services, making it more difficult for them to keep costs in line with the new QM rule.

With regard to max mortgage rates under QM safe harbor, Emerson thinks the spread of 200-250 basis points over the Average Prime Offer Rate (APOR) is more suitable than the current 150 basis points.

Again, borrowers with poor credit and/or small down payments could be forced outside the QM box, pushing them to accept even higher, non-QM rates.

Of course, it’s a slippery slope if you start changing all the rules that were just created. If we allow a huge range of interest rates and points and fees, we’re almost back to square one again.

But one thing seems to be clear. Most lenders won’t originate very many non-QM loans, at least while regulators and bankers work to get the kinks out.

In the short term, that could make it harder to get a mortgage.

Read more: Quicken Loans Rocket Mortgage review.