A new study from credit reporting agency TransUnion revealed some interesting insights about credit card use and mortgage performance.

The report titled, “TransUnion Minimum vs. Actual Payments Study,” found that roughly four in 10 consumers pay off their credit cards in full each month. Of the remaining six, about two will only make the minimum payment due.

Those who pay off their credit cards in full each month are known as “transactors, “ while those who carry debt from month to month are known as “revolvers.”

TransUnion found that the latter group tends to get into trouble on other loans, such as auto loans and mortgages.

To measure just how much worse these revolvers performed, the company came up with two new metrics.

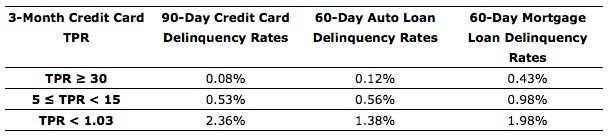

The first, known as “Total Payment Ratio” (TPR), is calculated by dividing a consumer’s aggregate monthly credit card payment by the total minimum due on all their credit cards.

So if a consumer has five credit cards with a combined minimum payment due of $250, but pays a total of $2,500, their TPR would be 10.

Per the study, this would land the consumer in the middle bracket, which has heightened risk of mortgage delinquency, as seen in the chart above.

It is consumers with TPR’s north of 30 that perform best on other loans, with mortgage delinquencies significantly lower than those with much smaller TPRs.

The worst group is those with TPRs below 1.03, otherwise known as those making the minimum payment, or perhaps a tiny bit more.

For these revolvers, the 60-day mortgage loan delinquency rate jumps to 1.98%, compared to fractional rates in other categories.

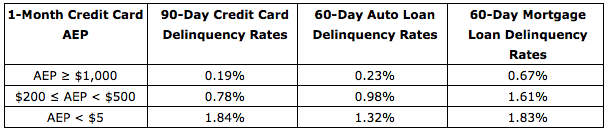

Then there’s the second metric, known as “Aggregate Excess Payment” (AEP). This is essentially the difference between the total minimum due and the total payments made on all of a consumer’s credit cards.

So for a consumer who owes a minimum of $250, but makes total payments of $2,500, their AEP would be $2,250.

At the same time, if a consumer only has minimum payments that total say $50, and makes a $300 payment, their AEP would be just $250.

Per the second chart, this would make them a greater mortgage default risk, even though they made much more than the minimum payment due, and perhaps the total amount actually due.

[A Mediocre Credit Score Will Cost You Big on Your Mortgage]

Two Important Takeaways

In other words, the best mortgage borrowers are those who pay much more than they owe each month, and at the same time make large payments.

It’s obvious that those who pay much more than what is due are lower credit risks, but the large amount is a more interesting takeaway.

You basically have to make an excess payment of $1,000 or more to wind up in the lowest mortgage default bracket in their study.

So this means the best consumers are those that are capable of carrying large amounts of revolving debt and subsequently paying it all off quickly.

For the record, mortgage underwriters like borrowers who are able to demonstrate history of supporting sizable debt, not simply those with high credit scores.

If your credit history only includes a few low-limit credit cards, you’ll have a harder time qualifying for a mortgage than if you have other installment loans, like auto loans/leases, and prior mortgages.

These big loans prove that you are/were able to manage large amounts of debt, which is exactly what a mortgage is, a giant chunk of debt.

So while making on-time payments in full is great, it seems you’re still missing something if you aren’t actively spending on your revolving credit lines.

All of this is important, as it could change the way mortgage lenders look at prospective borrowers in the future.

It doesn’t mean you have to go out and spend like crazy on your credit cards, but big spenders who pay off their bills in full appear to be the best mortgage borrowers.

Read more: How your credit score affects your mortgage.