Mortgage Q&A: “What is a lender overlay?”

If you’ve been studying underwriting guidelines recently to determine if you’re eligible for a mortgage, it’s important to understand that they can vary widely from bank to bank.

Even if you think you qualify based on the guidelines set forth by the FHA, USDA, VA, or Fannie Mae and Freddie Mac, you may be denied by an individual lender.

Let’s learn more about why this can happen and what you can do about it.

Different Mortgage Lenders Assume Varying Levels of Risk

- Just like any other line of business out there

- Mortgage lenders have varying risk appetites and specialties

- Some will accept lots of risk in exchange for higher interest rates

- While others will stick to more conservative lending even if they lose customers in the process

In a nutshell, mortgage lenders have different appetites for risk, along with different specialties, so what one lender will gladly approve, another may not touch with a 10-foot pole.

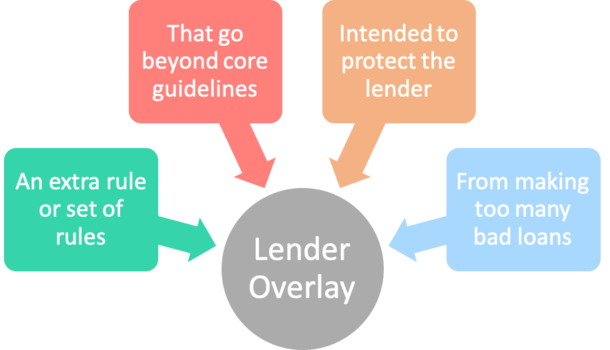

One important concept you should familiarize yourself with is the “lender overlay,” which is essentially an expanded guideline (or set of guidelines) on top of what Fannie Mae, Freddie Mac, or the FHA/VA will allow.

Think of it as a second coat of paint, applied after the primer. The primer is the bare minimum necessary, but you don’t see people driving around too often without that second coat.

The same goes for mortgages. Fannie Mae, Freddie Mac, and the FHA/VA all set underwriting guidelines for residential mortgages, but they don’t actually lend directly to consumers.

Their job is to purchase and/or securitize the home loans that fit their guidelines, which is why they exist to begin with. Essentially, to keep the mortgage market liquid.

By doing so, lenders are able to sell their loans more easily, knowing they fit certain pre-determined criteria, which allows them to originate more loans via that increased liquidity.

When it comes down to it, individual banks and lenders are the ones doling out loans, so they impose their own rules on top of those guidelines, known as overlays.

They do this to protect themselves from costly buybacks, assuming the loans sour after being sold, and to remain in good standing with their selling partners.

FHA Says Yes, We Say No!

- Just because your loan meets FHA underwriting guidelines

- Doesn’t mean the bank is willing to lend to you

- They may have their own buffer in place

- That goes above and beyond what the FHA will accept

You may have read that the FHA will accept credit scores as low as 500 as long as you’re able to put 10% down.

While this is true as far as the FHA goes, the particular lender you may be speaking with could require a minimum FICO score of 640.

What gives? That’s a 140-point difference, which is certainly a significant margin.

Well, this happens to be their comfort zone. Perhaps they’ve looked at default data and found that borrowers with credit scores below 640 miss mortgage payments frequently.

If they want to maintain a good relationship with the FHA, they’ll throw in that credit score overlay to ensure they only make quality loans, even if the FHA doesn’t require them to do so.

This reduces buyback risk and ensures they’ll continue to be able to do business with the FHA in the future.

After all, the last thing a lender wants is to lose its ability to make certain loans, assuming they plan to sell them off to the FHA, or Fannie and Freddie.

The opposite was true for Wells Fargo, which in the past imposed a minimum credit score of 600 for FHA loans, before succumbing to pressure from HUD to lower their minimum credit score to 500, assuming other criteria were met.

Ultimately, it’s tough for lenders because they may need to satisfy affordable housing goals while also ensuring the loans they make aren’t significant default risks.

There Are All Types of Lender Overlays

- There are a countless number of different lender overlays

- Banks and lenders impose them to ensure default levels stay in check

- The most common overlay is for minimum credit score

- They’re also typical for things like max LTV or max DTI

The credit score example is just one of the many lender overlays you’ll come across – there are literally hundreds of overlays required by individual banks and lenders throughout the country.

They range from credit score (most common), to max loan-to-value, to max debt-to-income ratio, and much more.

For instance, a streamline refinance may have no appraisal or credit score requirement, but a specific lender may still want a certain minimum score and an appraisal.

Additionally, the guidelines may indicate that you can get a new mortgage just days after a short sale if you remained current on payments, but most lenders will impose overlays to deny you.

Lenders may also restrict the type of loan you can select, such as an adjustable-rate mortgage in certain situations.

And even those nifty solar panels on the roof could present a problem if the lender doesn’t want to deal with the associated solar panel lease.

In every situation, the lender is looking to mitigate risk to ensure loan quality is upheld and maintained.

Look for Lenders Without Overlays

- Lender overlays are very common in the mortgage world

- But some lenders advertise the fact that they don’t impose them as a selling point

- While they may be able to fund your loan, pay attention to pricing to ensure it’s a good deal

- It might make more sense to improve your borrower profile before applying for a home loan

Now you should have a better concept of the master guidelines issued by Fannie, Freddie, and the FHA/VA versus those imposed by individual lenders.

Ultimately, it’s important to understand that all lenders won’t take on the same risks.

So if one lender denies you, there’s a chance another will approve you, and vice versa.

Unfortunately, it’s difficult to dig through all the guidelines and overlays of each bank and lender out there.

If you have a particularly difficult loan scenario, it may be wise to enlist a mortgage broker who can shop your loan with multiple banks at once to avoid any potential roadblocks.

This will save you spinning your wheels as brokers often know who to call to find a home for your loan.

There’s usually always a lender willing to do what another won’t, though the mortgage rates can and will vary.

Perhaps the best thing you can do as a borrower is minimize situations where overlays may surface.

In other words, keep your credit score in good shape, ensure you maintain a steady job, keep money in the bank, and stay current on your rent or mortgage.

That way it won’t matter what the guidelines are – you’ll be good to go regardless of where you apply.