Mortgage Q&A: “What is lender-paid mortgage insurance?”

Several years back, a rule went into effect that made mortgage insurance permanent on most FHA loans for the entire life of the loan. Ouch!

Before this game-changer, FHA loans were the cat’s meow because of the low mortgage rates offered, coupled with mortgage insurance premiums that were not only more affordable, but removed once the loan amortized to 78% LTV.

But in an effort to reduce losses, the FHA ended its so-called easy money policies and clamped down on borrowers taking advantage of a program originally intended for the underserved.

As a result, borrowers began giving conventional loans a lot more attention, seeing that private mortgage insurance (PMI) automatically terminates at 78% LTV.

Homeowners with these types of loans can also request PMI removal at 80% LTV (based on original amortization schedule) or even sooner if the home appreciates in value.

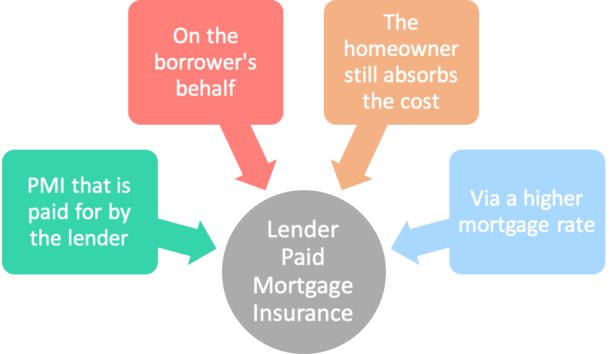

And even better, there’s a thing called “lender-paid mortgage insurance” on conventional loans where borrowers don’t have to pay for their own coverage!

That certainly sounds too good to be true, but there is a catch.

Lender-Paid Mortgage Insurance Isn’t Free

- The phrase “lender-paid” is somewhat deceiving/confusing (it’s not free coverage)

- Your mortgage lender isn’t doing you a favor out of the goodness of their heart

- The borrower still pays for this insurance coverage, just not directly out-of-pocket

- Instead the lender will pay the premium on your behalf, which should increase your mortgage rate

When you see the term lender-paid mortgage insurance, your first impression might be that the mortgage lender pays for it, and you don’t. Hooray!

The reality is that the lender does indeed pay for the mortgage insurance (on your behalf), but so do you, in the form of a higher mortgage rate.

So instead of securing an interest rate of say 3.75% on your 30-year fixed, you agree to a rate of 4% with no mortgage insurance costs paid out-of-pocket.

This is similar to a no cost refinance, where the lender pays all the closing costs, but you wind up with a higher interest rate.

Simply put, while it sounds like you’re getting something for free with lender-paid mortgage insurance, it’s more about how you pay for this coverage.

Lender-Paid vs. Borrower-Paid Mortgage Insurance

| $100,000 Loan Amount | Borrower-Paid MI | Lender-Paid MI |

| Mortgage rate | 3.75% | 4% |

| Mortgage payment | $463.12 | $477.42 |

| Mortgage insurance cost | $52 | $0 |

| Total monthly payment | $515.12 | $477.42 |

Now let’s look at lender-paid (LPMI) vs. borrower-paid mortgage insurance (BPMI) to see how they stack up in the real world.

This is just one example to illustrate the difference, so do your own math with real numbers if and when it comes time to make this important decision.

Let’s pretend you’ve got a loan amount of $100,000 at a loan-to-value ratio (LTV) of 90%. We’ll say the monthly MI premium is $52. Here’s how it would look.

Option A (Borrower-Paid Mortgage Insurance):

30-year fixed @ 3.75%

Monthly mortgage payment = $463.12 + $52 = $515.12

Option B (Lender-Paid Mortgage Insurance):

30-year fixed @ 4%

Monthly mortgage payment = $477.42 + $0 = $477.42

As you can see, the option with lender-paid mortgage insurance is actually cheaper (by about $40) in terms of total monthly payment, despite a higher mortgage rate.

This is the beauty of a long mortgage term – you can absorb upfront costs quite easily by paying them monthly instead.

However, the borrower-paid option will eventually become cheaper once the monthly mortgage insurance premium no longer needs to be paid.

But that would only be the case if you keep your home loan long enough to see that benefit.

Tip: How long you plan to keep the mortgage matters a lot when it comes to deciding between LPMI and BPMI.

Advantages of Lender-Paid Mortgage Insurance

- You don’t pay mortgage insurance directly (no out-of-pocket costs)

- May equate to a lower total monthly housing payment

- May qualify for a slightly larger loan amount

- Higher tax deduction possible if you itemize

One of the biggest advantages of LPMI is that you don’t have to pay mortgage insurance premiums.

As we saw from the example above, this can equate to a lower monthly mortgage payment in some cases, which is generally a good thing.

Of course, if you go with borrower-paid mortgage insurance (BPMI), your monthly mortgage payment will be lower once the mortgage insurance is no longer required.

So LPMI is generally only a money-saver if you don’t plan to stay in your home that long, or if think you may refinance sooner rather than later.

[Homeowners move every six years on average.]

If you elect to go with LPMI, you may also be able to qualify for a larger loan amount (or be able to purchase a more expensive home), seeing that the monthly payment can be lower.

A lower payment means a lower DTI ratio, which means you can get more loan for your income. While it may not be a huge difference, if things are close, the LPMI option could come in handy.

Another pro for LPMI is that there is the potential for a larger tax deduction, seeing that you’re paying a higher interest rate each month.

It’s a bit counterintuitive, but it should still be mentioned – this was especially pertinent before mortgage insurance premiums became tax deductible in 2007.

Tip: For those who earn more than $100,000 annually, the deductibility of mortgage insurance begins to diminish after that point, making the argument for LPMI even stronger.

Disadvantages of Lender-Paid Mortgage Insurance

- You can’t cancel LPMI since it is built into your mortgage rate

- Your mortgage rate will be higher as a result (maybe around .25% higher)

- You will pay more interest to the mortgage lender over the full loan term

- It’s non-refundable because it is paid for by your lender upfront

The clear disadvantage to LPMI is that it cannot be canceled, ever. Kind of like the mortgage insurance on most FHA loans nowadays.

Because LPMI is built into the interest rate, the “cost” is there forever, or at least until you sell your home or refinance the loan.

You don’t get to call your lender once your LTV hits 80% and ask or a refund or a lower interest rate.

And even if your monthly payment is lower to start, it will eventually be higher than the BPMI option, as we saw in our example.

Additionally, you’re stuck with a higher interest rate for the life of the loan, which means more interest must be paid to the lender.

Using the $100,000 loan amount example, you’re looking at an additional $5,148 in interest paid over the full 30 years. On a larger loan, it’s an even more significant cost to consider.

If you hold your mortgage for the full term, you will likely pay more with the LPMI option, even with the tax deduction factored in. Of course, how many people do that these days?

So that’s that – be sure to compare all mortgage insurance options with your mortgage broker or loan officer to determine what’s best for your personal situation.

Don’t just assume one is better than the other without actually doing the math and laying out a plan.

Read more: FHA loan vs. conventional loan