Mortgage Q&A: “When to refinance a home mortgage.”

With mortgage rates at or near record lows, you may be wondering if now is a good time to refinance. Heck, your neighbors just did and now they’re bragging about their shiny new low rate.

The popular 30-year fixed-rate mortgage slipped to 2.80% last week, per Freddie Mac, well below the 3.75% average seen a year ago, and much better than the 4-6% range seen years earlier.

Historically, mortgage interest rates have never been lower, making a mortgage refinance a veritable no-brainer for many homeowners out there.

In other words, there’s a good chance you won’t be holding off from refinancing because interest rates are too high (unless you just recently refinanced).

But even if you did, there’s a possibility it could make sense to refinance a second time.

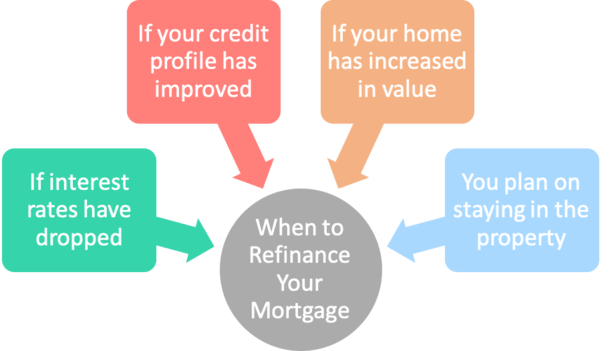

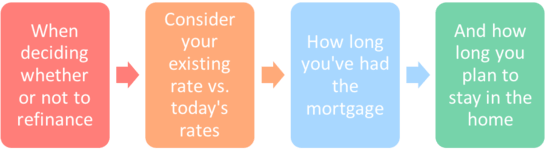

Should I Refinance My Mortgage Now?

- Consider your current interest rate relative to today’s available rates

- Along with required closing costs and how long it will take to break even

- Think about how long you plan to keep the mortgage/property

- And any other factors like removing mortgage insurance or shortening your loan term

Well, the answer to that question depends on a number of factors that will be unique to you and only you.

First, what is the interest rate on your existing mortgage(s)? Is it higher or lower than current mortgage rates?

If it’s higher, how much higher? If it’s lower, is your current loan adjustable? Or do you want to refinance for another reason, perhaps to tap equity?

Once you’ve got those basic questions answered, let’s talk about the new loan. What will the rate and closing costs be on the new mortgage?

Have you started shopping rates yet? Do you even know if you qualify?

How long do you plan to keep this new mortgage? What about the house? Are you sticking around for a while?

Assuming you’re still here, it might be a good time to take a look at a common scenario to illustrate the potential savings of a refinance.

Let’s look at a quick home refinance example:

Loan amount: $200,000

Current mortgage rate: 4.25% 30-year fixed

Refinance rate: 2.75% 30-year fixed

Closing costs: $2,500

The monthly mortgage payment on your current mortgage (including just principal and interest) would be roughly $984, while the refinanced rate of 2.75% would carry a monthly P&I payment of about $816.

That equates to savings of roughly $168 a month if you were to refinance. Not bad. But we aren’t done yet.

Now assuming your closing costs were $2,500 to complete the refinance, you’d be looking at about 14 months of payments, give or take, before you broke even and started saving yourself some money.

Yes, you need to consider the cost of the refinance too…

So if you happened to refinance again or sold your home during that window, refinancing wouldn’t make a lot of sense.

In fact, you’d actually lose money and any time you spent refinancing your mortgage would be wasted as well.

But if you plan to stay in the home (and with the mortgage) for many years to come, the savings could be substantial. Just imagine saving $168 for 200 months or longer.

This “break-even” point is key to making your decision, at least financially speaking.

You also need to consider whether it makes sense to buy down your interest rate by paying points, which will increase the time to this break-even point.

For example, those who paid upfront points on their refinance a year ago might be kicking themselves, knowing they’ll benefit from a subsequent refinance thanks to today’s even lower rates.

So sit down and determine your future housing plans before you decide to refinance to determine if it’s the right move.

If you don’t know what your plan is for at least the next few years, you may want to hold off until you do.

[The refinance rule of thumb.]

How Long Have You Had Your Existing Mortgage?

- You also have to consider how long you’ve had your current home loan

- This can play a big role in determining whether a refinance makes sense

- Take note of how much it has been paid down since that time

- And how much of each payment is going toward interest

Here’s another consideration. If you’ve already paid down your mortgage substantially, it might not make sense to refinance, assuming you want to pay the thing off.

Even if rates are super low, as there’s a good chance you’ll pay more interest overall if you “reset the clock” and start your full loan term over again. But this isn’t always the case.

To determine if a refinance is still the right move, get your hands on an amortization calculator.

That way you can see what you’ll pay in interest if you keep your mortgage intact versus what you’ll pay in interest with the new mortgage, factoring in what you’ve already paid on the old mortgage.

You can also use my refinance calculator to plug in all the pertinent numbers, including what we discussed above, to get a quick answer.

If your calculations reveal that you’ll pay more interest over the entire term of the refinance mortgage, there’s an easy strategy to reduce both interest paid and the term of the new mortgage.

Simply make the same monthly mortgage payment you were making before the refinance, with the excess going toward principal each month.

This will shorten the loan term and could save you a lot of money. I explain this method on my mortgage payoff tricks page, which you can read about in more detail.

If you can afford it, you may also want to look into shortening the loan term by going with a 15-year fixed mortgage.

For example, if you’re already 10 years into your 30-year mortgage, reducing the term to a 15-year fixed will ensure you don’t extend the aggregate term.

And with mortgage rates so low, you may be able to retain your low monthly mortgage payment and pay the mortgage off even earlier than expected.

Also, 15-year mortgage rates are lower than those on the 30-year fixed.

Other Mortgage Refinance Considerations…

- Even if interest rates are comparable to what you already have

- It could make sense to refinance out of an ARM or an interest-only loan

- The same is true if you want to get rid of mortgage insurance

- Or if you’d like to consolidate two mortgage loans into one

If you’re currently in an adjustable-rate mortgage, or worse, an option arm, the decision to refinance into a fixed-rate loan could make a lot of sense.

Even if the monthly savings aren’t tremendous, getting out of a risky product and into a stable one could pay dividends for years to come.

Or if you have two loans, consolidating the total balance into a single loan (and ridding yourself of that pesky second mortgage) could result in some serious savings as well.

You’ll have one less mortgage to worry about and ideally a lower combined monthly payment.

The same might be true if you have mortgage insurance and want to get rid of it. Many homeowners will execute an FHA-to-conventional refinance to drop MIP and reduce monthly payments once they’ve got some equity.

Additionally, you might be able to get your hands on a no cost refinance, which would allow you to refinance without any out-of-pocket costs (the rate would be higher to compensate).

In this case, if the rate is lower than your existing rate, you start saving money immediately.

As mentioned earlier, a cash-out refinance could also contribute to your decision to refinance if you are in need of money and have the necessary equity.

Heck, with mortgage interest rates this low you could even make the argument to tap equity and invest it elsewhere for a better return.

Again, you’ll want to aim for a lower rate and cash back, but there could be a scenario where borrowing from your home is the best deal, even if you don’t save much or anything mortgage payment-wise.

This is really just the tip of the iceberg. There are countless reasons to refinance your home loan, including many seemingly unconventional ones you may have never thought of.

Whatever the reason, be sure to put in the time (and the math) to ensure it’s a good decision for you and not just the bank or a loan officer pushing you to do it!