Everyone wants to be the next big thing in the mortgage industry, promising a digital experience or even a funded loan in days as opposed to weeks.

We’ve seen signs of this disruption for years now, and while it has improved the customer experience somewhat and shortened turn times, things aren’t much different.

You still have to fill out a loan application, often with the assistance of a human, submit financial documents, and wait for weeks (or over a month) to get your loan funded.

The difference now is you can do some of these tasks remotely, or better yet, authorize your financial accounts to be plugged into the application so you don’t need to track down documents yourself.

But there’s still the usual frustration and timelines that have long plagued the mortgage industry.

While most disruptors have focused on speed and convenience, an emerging company called “LoanSnap” is focused on originating “smart loans” as opposed to “dumb loans” that cost consumers billions annually.

What Is LoanSnap?

- A direct mortgage lender and tech company based in Costa Mesa, CA

- It was formed after acquiring Irvine, CA-based DLJ Financial

- Currently licensed to do business in 19 states including AZ, CA, CO, FL, IL, and TN

- Relies on artificial intelligence (AI) to offer a so-called smart home loan to consumers

LoanSnap was formed after acquiring DLJ Financial, a mortgage lender that had been based in Irvine, California for some 21 years.

The company’s current location is in nearby Costa Mesa, CA, with corporate headquarters in tech-rich San Francisco.

It makes sense that they have locations in both cities, as the Bay Area is where startups are born and Orange County has long been mortgage-central.

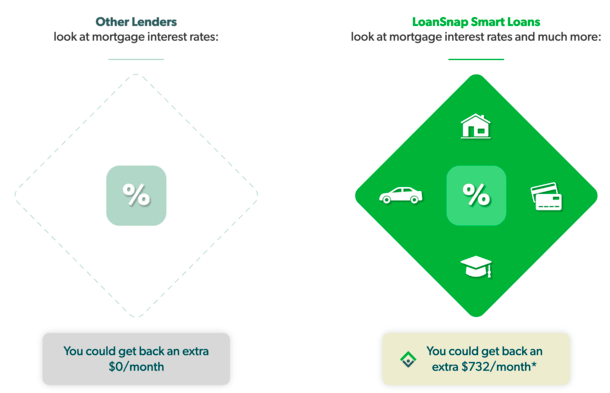

They offer a so-called “smart loan” that factors in all your monthly bills, such as credit cards and student loans, to ensure you get the best home loan.

In LoanSnap’s own words, it’s a mortgage that relies upon artificial intelligence (AI) “to analyze a consumer’s financial situation instantly and recommend the best options for their unique needs — all while addressing common financial issues like too much debt.”

Put another way, it goes beyond just the lowest mortgage rate or the fastest turn times and considers a customer’s entire financial situation.

After all, the borrower’s home and accompanying mortgage can often serve as their nest egg, dictating other investments and financial decisions.

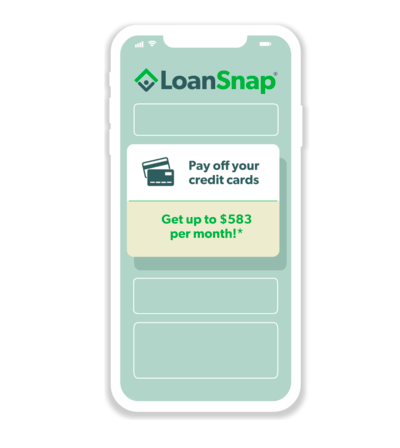

It can also be leveraged to pay off other high-interest debt, which is where LoanSnap figures in.

At the start of the loan application on their website, they say, “Welcome! Let’s start by identifying where you’re losing money so we can help you own your financial future.”

What they mean by that is you’re probably paying more interest on your credit cards, student loans, and car loans than you are/would be with a low-rate mortgage.

After all, mortgage rates are close to 3%, while credit cards are often 20%+ and auto loans and student loans are maybe 5%+.

They add that most folks “don’t realize they can move their credit cards or loans to their mortgage and save thousands in interest payments.”

So instead of pitching the lowest interest rates, they give you a full view of all your accounts to help their customers avoid losing money.

What Types of Mortgages Does LoanSnap Offer?

- Home purchase loans, mortgage refinances, and HELOCs

- The cash out refinance appears to be their chief offering

- You can get a conventional loan, non-conforming loan, FHA loan, or a VA loan

- Available on single-family homes and condos/townhomes

At the moment, they offer home purchase loans, mortgage refinances, and HELOCs.

That includes both rate and term refinances and cash out refinances, the latter of which is utilized to pay off other high-interest bills you may have.

The cash out refinance seems to be their weapon of choice to eliminate other debt, and explains the how and why of analyzing a consumer’s complete financial situation.

Once they know about your other debts, they can instantly recommend the best loan options that consider interest rates on all your outstanding debt, thereby saving you money.

In a sense, it’s marketing the cash out refinance as something unique to the company, while just about every mortgage lenders offers them.

Of course, things are a little less liquid in that department at the moment due to COVID-19, but that will likely change over time as the situation normalize.

It also means larger loan amounts for LoanSnap, which equates to more money for them.

In terms of loan type, they offer FHA loans, VA loans, and non-conforming loans. I assume they offer conforming loans backed by Fannie Mae and Freddie Mac as well.

They also offer second mortgages in the form of a home equity line of credit (HELOC), which can be used to pay off other bills like student loans, auto loans, and credit cards.

You can get a home loan on a single-family residence or a condo/townhouse. It’s unclear if they lend on second homes and investment properties.

In terms of where they’re available, they lend in 19 states with plans to expand to more soon.

At the moment, they’re licensed in Arizona, California, Colorado, Florida, Georgia, Illinois, Iowa, Kansas, Michigan, Nebraska, Ohio, Oregon, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Washington, and Wisconsin.

LoanSnap Mortgage Rates

While LoanSnap says it looks beyond mortgage rates to help its customers save money, essentially by saving them on other, higher-cost loans, it doesn’t reveal its rates.

Obviously it’d be nice to get an idea of where they stand pricing-wise, but there’s no daily rate section on their website as of now.

So if you want to pricing, you’ll need to either apply or give them a call. My recommendation is to get pricing first before spending time on an application.

Note that cash out refinance rates are often higher than purchase rates, so if you’re comparing rates among lenders, be sure it’s apples-to-apples.

Also take a look at their customer reviews to see what other customers thought about their interest rates and fees for more clues.

With regard to lender fees, they also leave us in the dark, so be sure to inquire about fees and rates when you call and speak with a loan officer.

LoanSnap Reviews

Despite being a relatively young company, they’ve already amassed a decent number of customer reviews.

On LendingTree, they’ve got a 4.6-star rating out of 5 from nearly 300 reviews, with a 92% recommended score.

At Trustpilot, they have a 3.8-star rating, which the site considers “great,” but not quite excellent.

Over at Google, it’s a similar 4.1-star rating, which is certainly good but not the highest customer satisfaction tier.

On Zillow, they have just a dozen or so reviews and a 4.27-star rating.

While they’ve been accredited with the Better Business Bureau since 2009, they aren’t currently rated.

LoanSnap Received an Investment from The Chainsmokers

- Company has raised millions of dollars via several funding rounds

- Latest investment comes from fund backed by pop group The Chainsmokers

- Also supported by True Ventures, group behind Peloton and Fitbit

- Expect them to become a household name in the mortgage world with that backing

In a bid to perhaps become the coolest mortgage lender out there, aside from maybe Rocket Mortgage, they announced a new investment round that included pop duo The Chainsmokers.

The popular group that makes electronic music is apparently also interested in making money, as evidenced by their early stage technology investment firm known as MANTIS.

In mid-May, LoanSnap raised an additional $10 million, co-led by True Ventures and MANTIS.

To show just how serious they are, True Ventures is the Silicon Valley-based venture capital firm behind Peloton, Blue Bottle coffee, and Fitbit.

Their backers also include Richard Branson and Joe Montana’s Liquid 2 Ventures, so it appears they came to play.

Expect to hear the name LoanSnap if and when searching for a mortgage in the near future.

(photo: Jason White)

This is a con. Loansnap is a mortgage broker looking for sales leads. There us no AI. It’s a con.