Want to talk about a double whammy, just in time for the spring home buying season?

Well, it occurred to me that thanks to the ongoing conflict in the Middle East, both gas prices and mortgage rates have spiked higher.

And the irony is they both have a 6-handle again, assuming you live in a pricey state like California.

That one-two punch means it’s even less attractive to move forward with a home purchase today.

For the prospective home buyer out there, their cost of living just went up, whether it’s qualifying for a mortgage or simply driving across town.

6-Handle Mortgage Rates and Gas Prices Thanks to Surging Oil Prices

The economy works in mysterious ways sometimes, the latest example being 6-handle mortgage rates AND gas prices.

The cost of a gallon of gas and a 30-year fixed mortgage rate have essentially intersected thanks to this unexpected development.

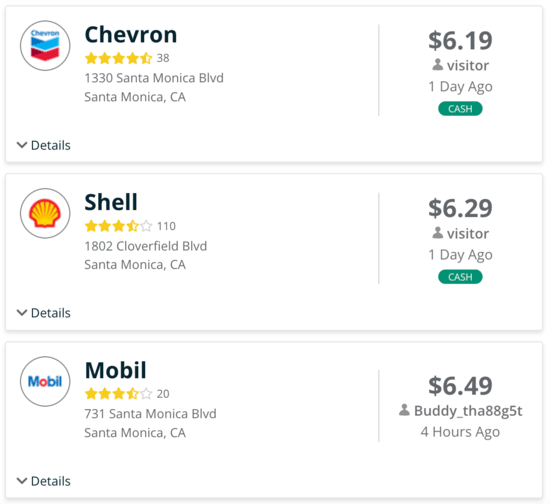

I was checking out gas prices on the GasBuddy website the other day and saw that a gallon of premium in Los Angeles now exceeded $6!

I immediately thought the prices looked a lot like 30-year fixed mortgage rates, which are also hovering around the low-to-mid 6s again.

As you can see in my screenshot, $6.19, $6.29, and $6.49 for a gallon looks strangely similar to a lender’s daily mortgage rates at the moment.

This is something that wasn’t an issue just over two weeks ago, when the 30-year fixed had finally fallen below 6% for the first time in several years.

Same with gas prices. I can’t remember the last time it set you back more than $6 per gallon to fill up.

It’s About More Than Just Mortgage Rates

This illustrates something I’ve been trying to articulate since mortgage rates spiked higher in early March.

A lot of this is psychological, as the difference in monthly payment between a rate of 5.99% and 6.25% is pretty minimal.

But now that the cost of living is going up, it’s going to become very real for prospective home buyers attempting to make a home purchase pencil.

If it costs another $20 (or more) to fill up at the pump, their stock portfolio is in the dumps, and inflation rears its ugly head again due to higher input costs on everyday goods, it becomes a collective problem.

All of a sudden, they’re being hit from all angles. They’re feeling the sticker shock at the pump, they’re too afraid to even look at the stock market…

And when they go check daily mortgage rates, the 5-handle rates have been replaced with 6-handle rates.

To make matters worse, it all seems to be getting worse.

First it was rates back above 6%. Then it was 6.125%, then 6.25%, and nearly back to 6.50% to end last week.

We got a little bit of a breather today, but who’s to say we don’t go to 6.50% next?

You get the feeling it’s going to get worse before it gets better, though if we can find some sort of resolution, that can change.

The one silver lining is that much (if not all) of this spike in mortgage rates and gas prices is related to the Iranian conflict.

If that can somehow get resolved, you begin to envision a path back to where we were before this got going.

It’s a very acute issue that hypothetically could be reversed if it proves to be short-lived.

That’s the larger question though. Will it turn out to be a blip or is it the start of something bigger?

- Mortgage Rates and Gas Prices Are Back in the 6s! - March 16, 2026

- Beeline’s Self-Service Mortgage Option One Step Closer to Loan Officer Extinction - March 13, 2026

- Mortgage Rates Just Flipped From Trending Down to Trending Up - March 12, 2026