Mortgage Q&A: “Are mortgage rates negotiable?”

Here’s a popular question everyone looking for a mortgage wants to know (or should want to know).

And it’s an especially important one if you’re actively shopping for a home loan, since the clock is probably ticking and you’ve got work to do.

Can you get an even lower rate than the quote you just received? Or do lenders really have their hands tied? Let’s dig right in.

You Should Be Able to Negotiate Your Mortgage Rate

- Yes, mortgage rates are negotiable in most cases

- If anyone tells you otherwise they’re probably fibbing

- There’s always wiggle-room like there is with any other product you buy

- But you won’t know this unless you take the time to ask!

In most cases, mortgage rates are 100% negotiable, like many other costs involved with obtaining a mortgage, such as the loan origination fee.

This was especially true back before the mortgage crisis, but a little more complicated these days thanks to compliance issues.

There are also some online lenders today that don’t use loan officers, nor pay out commissions based on rates. So in these cases, you can’t really negotiate with the company directly.

But if there is an individual involved, which there often is, there’s a good chance you’ll be negotiating.

Like anything else you shop for, you may be told that prices/rates are firm, or are as low as they can go. Psssh.

This isn’t the case, as mortgage rates can always be adjusted up or down in a variety of different ways, and commissions and fees can often be lowered or waived.

Even if the rate can’t be flat-out lowered, you can buy down your interest rate by paying mortgage discount points.

This isn’t pure “negotiation” because you’re actually paying prepaid interest upfront to lower costs during the loan term, but it does prove that mortgage rates can be adjusted.

The opposite is also true – like in the case of a no cost refinance, where you pay nothing out-of-pocket, but take on a higher mortgage rate to compensate the originator for that lack of costs.

Ask for Multiple Mortgage Rate Quotes When Negotiating

- Get several mortgage quotes from a few different lenders/brokers

- This allows you to negotiate effectively among them

- Otherwise you really have nothing else to go on while attempting to secure a lower rate

- Aside from simply asking/begging for a lower rate and/or costs

A more pure form of negotiation involves comparing rates for the same product from a variety of different banks and lenders.

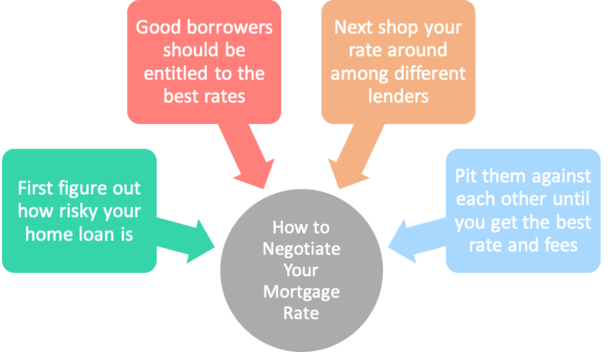

Before you do that, it’s important to understand if your home loan is low-risk or high-risk.

Simply put, lower-risk loans are entitled to the best interest rates available, whereas risky loans will be subject to pricing adjustments that can drive the rate much higher.

Once you have an idea of what you should be charged, you can start making phone calls.

First, you’ll want to obtain multiple rate quotes from a single lender, by asking for a series of interest rate/cost combinations, as discussed above.

So if the loan officer or mortgage broker offers you a rate of 4.75% on a 30-year fixed with $2,500 in closing costs, you can ask for other options.

What would the mortgage rate be with no closing costs, or just $1,000 in closing costs? What if you paid $5,000 in closing costs?

After getting all those quotes, jot them down, then shop around with other lenders to see who has the best mortgage rate and lowest fees.

Go Back to the Lender Who Provided the Best Quote

Once your shopping is complete, you can go back to the lender who offered you the best deal and ask for a slightly lower rate or reduced closing costs.

You can do this by using another bank or broker’s offer as leverage, even if it doesn’t really exist.

There’s a chance you’re not getting the rock-bottom rate the first time around, so why just accept it as the best offer?

Always haggle! Especially when something has the potential to hit your pocketbook for the next 360 months!

Mortgage brokers in particular should really be able to negotiate rates because they work with multiple lenders and may have flexible compensation plans.

This means they can provide you with rate quotes from a variety of different banks at once, and if the rate(s) isn’t good enough for you, they might just come up with a lower one from a different lending partner of theirs.

For example, they may get paid more from Bank A, which happens to offer slightly higher rates than Bank B, which happens to pay them a slightly lower commission.

Of course, you’ll never know this if you don’t take the time to ask or complain that the initial rate is too high!

Conversely, someone working at a big bank may just be limited to what their computer program tells them.

In this case, they may not actually be able to go lower, but that doesn’t mean you can’t just pick up the phone and try other lenders.

Use the Competition to Your Advantage When Negotiating

- You basically want to scare one lender into lowering their rate/fees

- To do so you’ll need to make a compelling argument to use the “other guy”

- If convincing enough, the lender may say they’re willing to go lower

- It’s possible they’re already offering their best rate/price, but you won’t know unless you ask

The mortgage industry is a very competitive space, so mortgage lenders and their representatives will always be willing to work with you to snag your business, assuming you actually qualify.

They may make a little less in the way of commission, but still enough to want to close your loan.

Don’t believe it when they tell you they’re “just breaking even” or “not making enough” to do the deal. This is simply their justification to make more money while you pay more.

In the end, they need your business more than you need theirs, so remember that during negotiations.

There are also loan originators who work on volume, so for them, just getting your deal, even if they aren’t making a whole lot on the loan itself, could boost their profits and be well worth their while.

Be sure to compare mortgage rate quotes online, visit local banks, and speak to a few mortgage brokers.

It’s a big deal to get a mortgage, so why stop at just one or two quotes? Negotiating is a lot easier when you’re pitting multiple lenders against one another.

All that talking the talk may also make you a fiercer opponent when speaking to subsequent lenders. You’ll actually sound like you know what you’re talking about.

Just make sure you actually lock your mortgage rate when you’re happy with the deal.

If it’s not locked, the interest rate isn’t guaranteed. And if anything, it’s more than likely going to rise from the quote you originally received.

This failure to lock might be why we hear so many “bait and switch” stories from borrowers. A few days go by, the market worsens, and the original rate is no longer available. Often it’s the truth!

At the end of the day, everything in life is negotiable if you’re willing to speak up and ask for a lower price, or in the case of a mortgage, a lower rate.

It always amazes me how folks simply accept what’s thrown in front of them. The first price is never the best price!

Tip: What mortgage rate can I expect?

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

I would like to compare rates for pre approval how many lenders do you suggest I make outreach to. Also should I space them out or can i apply for examples 3 pre approvals in one day online.

Netta,

It’s entirely up to you. You can shop around without actually applying or providing paperwork just to get a feel for different lenders, though rates won’t be set in stone until you actually apply and lock. There’s no need to space things out as FICO already considers multiple applications for a mortgage in a short period of time as one shopping event with regard to your credit.

Who is the largest loan company?

Anna,

Wells Fargo is the largest residential mortgage lender, if that answers your question.

Thanks for this info Colin. I linked through to this after looking into Costco’s mortgage “program” to try to determine if it was worth re-upping to an Exec membership to get the lender fees down to $350 (their current offer). Since that article was written in 2012, what do you think about their current program. Is it still a marketing arm for First Choice Bank? I’m looking at a cross-country move, purchasing a new home so I went to Quicken for my pre-approval, but their closing costs and APR are pretty high. They promised to be more aggressive when I make a firm offer on a home.

Lynn,

Not sure who Costco works with these days…I think they’ve had partners come and go. You could simply try to negotiate with other lenders outside Costco instead of paying for a membership you might not otherwise need. For example, another lender not affiliated with them may offer no lender fees and a better rate, without having to bother with the executive membership fee.

Thank you, Colin. I readily admit my limitations…my strength is in writing and these high-stakes monetary negotiations make my head spin, so I sincerely appreciate your quick response and advice!

Colin,

Two days ago my mort guy moved my cash at closing from $219 to $805 – and I’m supposed to be closing tomorrow. This is after our interest rate has gone from 4.25 up to 4.5 then after I said something about the change adjusted to 4.375 – this is with an excellent credit score and we are in a very comfortable equity position with our appraisal. Currently I see other lenders with a 20 yr at 3.5% 3.7% – needless to say – I told him that the change was unacceptable and the closing is off.

Is it within my rights to shop for a new mortgage? Our lock in date expired on 4/15/17 at 5pm.

Kerrie,

You’re always welcome to shop around, but there might be consequences, such as relinquished fees for appraisal and application, so you have to weigh the pros/cons of going elsewhere. If a different lender can give you a lower rate and absorb any lost fees it can make sense to go some place else.

Feeling a little frustrated. I thought that interest rates were based merely on down payments and credit scores. I applied for a loan with Wells Fargo, was quoted a 4.25% rate with just 11% down.

Since the mortgage insurance was quite expensive, I decided to come up with 20% down. The loan officer told me that my rate will go up to 4.50% because there’s a “downward rate adjustor” for loan amounts higher than $175K and because my down payment will make my loan amount below $175K, then my rate goes up. I’ve been researching online if there’s such a thing as a rate adjustor and couldn’t find anything.

Lorenzo,

Sometimes you can be “penalized” for a very low loan amount because its smaller size means it is less profitable to the bank. If that’s the case, you can either negotiate with Wells or shop other banks to see if there are better offers for your particular scenario.

Hi Colin

My husband and I are building a home in an active adult community called Robson Ranch which has an in-house lending company. Of course they are recommending we use them (because outside companies aren’t familiar with these types of deals). The process is in several steps. By the time we go to closing, we will have already invested about $45,000 (deposit and options). We have excellent credit and a great DTI ratio, so I believe that we should shop around for a great int.rate.

Please give me your thoughts.

Christa,

It’s always recommended to shop around to ensure you get a good deal and explore all your options. And yes, builders will likely want you to use their own financing department, which has its pros and cons I’m sure. The pros are that they really want to close your loan, I assume, the cons are that the pricing might not be as good as other lenders. You can also always negotiate with them directly, or get some other quotes and then try to negotiate if they’re significantly better. Good luck!

Hi Lynn,

I’m wondering who you ended going through. I just talked to someone from Quicken and when I asked about APR he just stated that it’s just the closing cost. So now I’m wondering. I had my credit pulled July 28 and September 24th. I am now thinking of shopping around. Is it ok to get my credit pulled again. I had Quicken offer me a lower Interest rate, but that was without pulling my credit

Robin,

If multiple mortgage lenders pull your credit in a short timeframe, generally 45 days, FICO treats them as a single inquiry. This allows consumers to shop around without worrying about a potential credit score ding.