It’s been some time since I’ve done mortgage Q&A, so without further delay, let’s explore the following question: “Do you need 20% down to buy a house?”

If you chat with anyone older than 50 (maybe 60), they’ll probably tell you that you need to (or should) put 20% down if you want to buy a house.

For them, it’s the normal, or should I say traditional, down payment needed to secure a mortgage.

And while it might be conventional wisdom when it comes to home buying, it’s not necessarily the reality anymore.

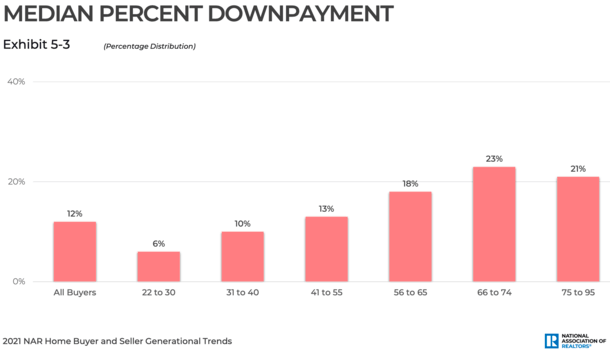

In fact, the median down payment is just 12%, per the National Association of Realtors (NAR) 2021 Home Buyer and Seller Generational Trends report. Despite this, a lot of people still seem to think you need 20% down to purchase a home.

You Don’t Need a 20% Down Payment…

A few years back, the NAR 2017 Aspiring Home Buyers Profile report found that 39% of non-owners believed they needed more than 20% for a mortgage down payment on a home purchase.

And 26% assumed they needed to put down 15-20%, while 22% said they needed a down payment of 10-14% in order to buy. None of those answers are true.

A 2020 study from NAR also had a whopping 35% of respondents going with the 16% to 20% down payment tier, easily the number one answer.

In reality, you may not even need a down payment if you take out a certain type of home loan, or receive gift funds for the down payment.

Even if a down payment is required, it’ll be a lot less than 20% in most cases, most likely less than 5%.

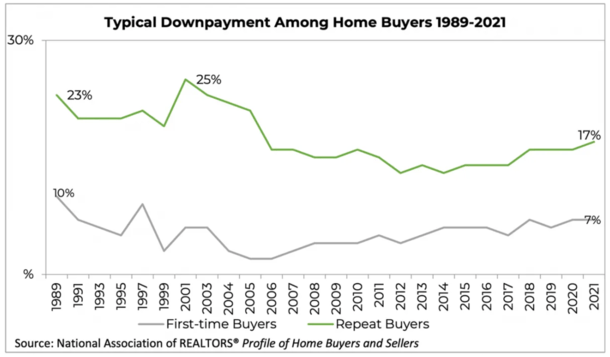

Last year, the typical down payment for first-time home buyers was just 7%, while it was 17% for repeat buyers, per NAR.

It’s common for repeat buyers to use the proceeds from their original home to buy a replacement, making it easier to come up with a larger down payment.

Conversely, first-timers often have a tough time coming up with funds because they can’t tap into home equity.

You’ll notice both figures have moved lower over the years, though average down payments have ticked higher recently, perhaps due to home buyer competition in this hot housing market.

20% Down Payments Used to Be the Norm

- Your parents probably put down 20% or more when they bought a house

- But back then home prices were a lot lower than they are today (and interest rates a lot higher)

- You might only need to put down 3% or 3.5% when you purchase a property these days

- But there are still key advantages to putting down at least 20% like no mortgage insurance and a lower interest rate

Back in the day, it was customary to come in with 20% down (or more) when purchasing a property.

But property values were significantly lower those days, and mortgage rates a lot higher.

Times have changed as home prices skyrocketed and mortgage lenders got more competitive (and less risk-averse).

Leading up to the housing crisis seen in the mid-2000s, a zero down mortgage was a common theme. In fact, there were lenders that named themselves after that lack of a down payment…

Of course, we all know what happened next – home prices tanked and low down payment options began to evaporate.

That led to increased FHA loan lending, which requires only 3.5% down if you have at least a 580 FICO score.

And over time, Fannie Mae and Freddie Mac introduced a competing product that allows for loan-to-value ratios (LTVs) as high as 97% (just 3% down).

So we’ve kind of come full circle, though we’re not quite at the zero-down stage just yet.

Though lenders have offered mortgages with just 1% down, such as Quicken, Guaranteed Rate, and United Wholesale Mortgage thanks to the use of grants.

Should You Put Less Than 20% Down on a Home?

- You may not need to put 20% down on a home purchase in many cases

- But it will cost you more money monthly if you don’t via a higher rate, PMI, and a larger loan amount

- It may also make your offer less desirable to home sellers if they have competing bids with larger down payments

- So it can beneficial to put down more, especially in a seller’s market

We’ve already answered the original question. You don’t need a 20% down payment to purchase a home.

In fact, you don’t need any down payment in some cases if you consider a home loan from the VA or USDA, both of which offer 100% financing.

You also don’t need to put down 10% or even 5% thanks to widely available programs from the FHA and Fannie and Freddie.

The median down payment is quite a bit lower, around 12% at last glance, and even lower (6%) for the 22 to 30 age cohort.

This age group also said saving for the down payment was one of the most difficult steps of the home buying process.

Now assuming you can muster a 20% down payment, should you come in with less?

This answer is a bit more elusive because it depends on a variety of factors, which include your household balance sheet and your financial goals.

Perhaps it’s better to frame the question the other way around.

Why You Should Put 20% Down on a House

In short, the less you put down on a home, the more you pay each month via your mortgage payment. This happens for three main reasons:

– Larger loan amount (less down means more financed)

– Higher mortgage rate (rates tend to rise as down payments fall)

– Mortgage insurance (added cost to account for risk)

If you put down less than 20%, you wind up with a bigger loan amount (obviously), a higher mortgage rate (usually) because of pricing adjustments, and you have to pay mortgage insurance to protect the lender.

This means your monthly housing costs go up, but you keep more cash in-hand, or at least not in your house.

Let’s assume the home you want to purchase is selling for $350,000 and you plan to take out a 30-year fixed mortgage. This comparison chart shows us how things might look.

3% Down vs. 20% Down: The Math

| $350,000 Home Purchase | 3% Down Payment | 20% Down Payment |

| Down payment | $10,500 | $70,000 |

| Loan amount | $339,500 | $280,000 |

| Mortgage rate | 4.125% | 3.875% |

| Monthly P&I payment | $1,645.39 | $1,316.66 |

| PMI | $125 | n/a |

| Total monthly cost | $1,770.39 | $1,316.66 |

| Difference | +453.73 |

As you can see from the chart above, the 3% down mortgage payment is roughly $454 more expensive each month thanks to those three things I mentioned.

That higher payment equates to an additional $27,223.80 spent over the course of five years.

Additionally, because the loan balance and mortgage rate are higher, more of your payment goes toward interest every month.

After 60 months, the 3% down mortgage would have a balance of $307,684.69, whereas the 20% down mortgage would be whittled down to $252,738.50.

The tradeoff is basically more money in your pocket versus the home, and the ability to buy more house now in exchange for a higher monthly payment.

This assumes you lack the down payment funds, but can afford the higher payments, which can be a common scenario for young high-earning individuals without significant savings (HENRYs).

At the same time, I’ve argued that it’s possible to buy more house if you put more money down because less income is required.

This assumes income is the problem and not assets, which can result in debt-to-income issues, which are prevalent and often grounds for denial.

Of course, it’s entirely possible for a low-down payment to be voluntary, for a homeowner who wants to park their money elsewhere.

That decision really comes down to how you value your housing investment, and if you think you can do better putting the money in the stock market or some other place.

For those who don’t have that choice, take comfort in the fact that you don’t need a 20% down payment to buy a home, or anywhere close to it.

But you will pay extra for that convenience, and you might have more hurdles to clear, such as convincing a seller to take your offer when another prospective buyer offers to put down 20%.

Alternatively, you could get a gift for a portion of the down payment and get the best of both worlds.

Can You Put More Than 20% Down on a House?

- You can put as much down as you’d like (or even buy all-cash to avoid the mortgage entirely)

- There are advantages to putting down more than 20% on a home purchase

- Such as a lower mortgage rate thanks to fewer pricing adjustments

- And an even stronger offer if buying a home in a hot market

- Also a lower monthly payment and much less interest paid

You sure can. It’s generally possible to put down as much as you’d like on your home purchase, though if you put down too much you could run into issues with minimum loan amounts from lenders.

Of course, this probably isn’t going to be an issue in most cases with property values so high these days.

I’ve heard of home buyers putting down 50% just because they are debt-averse, but again, most folks don’t have that type of cash lying around.

The obvious benefit of putting a large down payment on a house is that you’ll have a smaller mortgage balance and pay less interest as a result.

You’ll also enjoy lower monthly payments, which will free up cash for other expenses or investments.

Conversely, you’ll have that much more money locked up in your property, which you’ll only be able to access if you sell or take out another home loan.

When it comes to mortgage rate pricing, it’s possible to obtain a slightly lower interest rate when you put down more than 20%, though it likely won’t be much.

We’re talking .125% to .25% lower depending on the scenario in question, so there are diminishing returns, especially when interest rates are already low.

But if you have bad credit the pricing impact can be greater with a larger down payment, so in those cases it could make sense to put down more than 20%, assuming you’ve got the cash available.

However, once you’re at 65% LTV (35% down payment) the pricing incentives tend to stop, so there wouldn’t be a benefit mortgage rate-wise after that threshold.

In summary, consider how much money you want locked up in your home, what your money could be doing (earning) otherwise, and how much it’ll cost you to put less down.

Lastly, don’t forget home sellers favor those who come in with larger down payments!

Read more: 2021 home buying tips to get the deal done.

Pros of Putting Down 20% on a Home Purchase

– Smaller loan amount

– No mortgage insurance required

– Lower mortgage rate

– Pay less interest over the life of the loan

– Ability to tap equity or take out a HELOC

– Lower closing costs

– Better chance of getting your offer accepted in a hot market

– More lender choice and loan options available

Cons of Putting Down 20% on a Home Purchase

– Requires a lot more money up front

– May make you house poor (little leftover for repairs/maintenance)

– Money tied up in the home that could lose value (and thus access to it)

– Could invest that money elsewhere for a better return

– Inflation makes dollars worth less over time

– Difference in monthly payment may not be all that substantial

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026