You’ve heard the news – mortgage rates jumped from close to 6% back in September to over 7% in less than a few months, before climbing even higher.

And they don’t appear to be heading back down anytime soon, despite some mild improvement this morning thanks to a cooler-than-expected CPI report.

While that’s still up for debate, the trend is clearly NOT your friend when it comes to securing a low interest rate on your home loan.

But that doesn’t mean you just throw the rules out the window and apply with any bank or lender willing to approve your mortgage application.

Nor should you just accept the first lowish interest rate presented to you, as enticing as it might be.

This is actually a great time to be even more aggressive when it comes to lender selection, especially as home buying competition remains fierce in many parts of the country.

1. Shop Your Mortgage Rate! Seriously

I’ve said it once and I’ll say it again, and again after that. Because apparently folks aren’t getting the memo.

You have to take the time to compare rates from multiple lenders if you want to secure the lowest interest rate on your mortgage.

There are real studies that prove this – it’s not just boilerplate advice.

A recent study from Freddie Mac revealed that getting just two quotes as opposed to one could save you thousands over the life of your loan.

And it actually gets better the more you shop. Three quotes saves even more. Sure, it’s no fun, but neither is paying a sky-high mortgage payment for the next three decades.

Don’t complain about the rates not being as low as you heard if you haven’t put in the time to shop.

If you make the effort to track down a coupon code for a simple online purchase, you should take the time to gather multiple mortgage rate quotes. Period.

A lower mortgage rate can have a much bigger impact on your finances since it stays with you for years, if not decades.

This is especially true now as lenders may be offering a wider range of rates during this volatile market period.

2. Improve Your Credit Scores, Then Apply for the Mortgage

Also a cliché in the mortgage industry, but a very real and important tip. It’s no secret that those with higher credit scores gain access to lower interest rates.

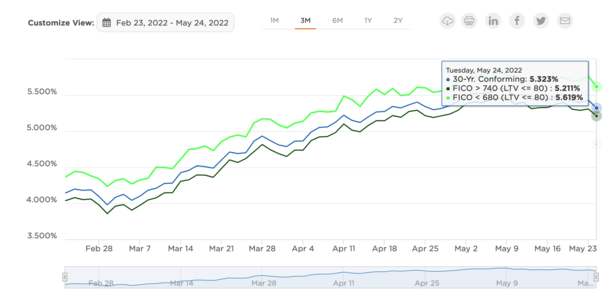

Just take a look at this chart above of real-time rate lock data from Optimal Blue.

Notice the borrowers with 740+ FICO scores have average rates of 5.211%, while the sub-680 borrowers have average rates of 5.619%.

That’s nearly a half-point higher simply because they haven’t addressed whatever credit issues are holding them back.

Rates are even higher today, but the same principle still applies. Higher scores equal lower rates!

So if you’re not doing your absolute best credit score-wise, you’re doing yourself a disservice. Take the time to work on your credit if it’s not where it should be.

Generally, a 780+ FICO score is sufficient to obtain the lowest mortgage rates possible, at least when it comes to your credit score.

If for some reason you can’t make the changes necessary before getting a mortgage, work on your scores after you get your loan and look into a rate and term refinance once things improve.

Just be mindful about paying points if you don’t plan to keep the loan for a long time. In this scenario, a temporary buydown could be the winning formula.

3. Come in with a Larger Down Payment

While perhaps not as easy as maintaining excellent credit history, a larger down payment can result in a lower mortgage rate, which will save you money each month for a long, long time.

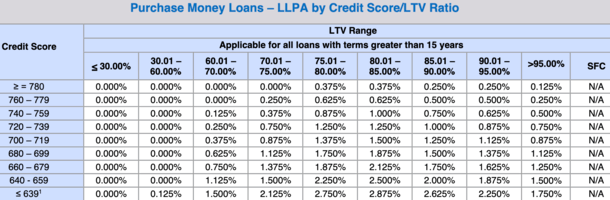

In the table above are loan-level pricing adjustments. You’ll notice they’re lower if your loan-to-value ratio (LTV) is lower. Same goes for credit score. Fewer adjustments equate to a lower interest rate on your loan.

Not everyone has extra money lying around to do this, but if you do, or you can save more before buying, it can work to your benefit when it comes time to apply for a mortgage.

You might even be able to get gift funds from a parent of relative to make this happen.

Those who are able to put down 20% or more can obtain lower interest rates and avoid mortgage insurance at the same time.

It’s actually a triple bonus because not only do you avoid pricing adjustments at the 80% LTV+ threshold and the PMI, you also wind up with a lower loan amount.

That means less interest is charged thanks to a smaller outstanding balance.

If refinancing your mortgage, you might be able to execute a cash in refinance and lower your LTV to snag a better interest rate.

4. Pay Some Discount Points (But Be Careful)

While somewhat counterintuitive, if you pay more now you can save later on your mortgage.

What I mean by that is offering to pay discount points at closing.

They’re basically a form of prepaid interest that will lower your interest rate for the life of your loan.

For example, if the 30-year fixed is pricing at 6.75%, but you can pay 1% of the loan amount today for a rate of 6.25%, it could save you a lot more money over the duration of the loan term.

Just be sure it makes sense financially, and that you plan to stay in the home/mortgage long enough to recoup the upfront cost.

If you don’t actually keep the home loan or the house for more than a few years, this could actually cost you.

And with rates so high at the moment, with dare I say a chance to drop in the next 12 months, it might be best to settle for a market rate sans points and hope to refinance to a cheaper loan later.

If all works out, you might be able to take the 7% today at no cost and refinance into something in the 6% range later this year. Maybe even high 5s!

5. Consider All Loan Programs

Yes, the 30-year fixed is in the 7% range now. But no, it’s not the only loan program available to home buyers and those looking to refinance an existing mortgage.

There are lots of different home loan types out there, many with lower interest rates than the 30-year fixed.

For example, the 15-year fixed prices closer to the mid-to-high 5% range, and adjustable-rate mortgages like the 5/1 and 7/1 ARM may also be significantly cheaper than fixed-rate products now.

They also provide a fixed rate for several years before you have to fret about a rate adjustment.

Consider an ARM if you want to save money, especially if you don’t plan on staying in the property for a long period of time.

Your interest rate may never actually adjust if you don’t keep it past the initial teaser period. And you could save a lot of money during those years.

If you’re in search of an ARM, consider a credit union, as they tend to offer bigger discounts compared to larger banks.

Again, you can refinance the ARM into a fixed-rate loan if mortgage rates get better in the near future.

6. Negotiate Harder

You can negotiate mortgage rates and fees. Maybe not all banks and lenders allow you to do this, but many do.

It’s also possible to compare mortgage brokers and have them compete for your business with their many wholesale lender partners.

And they may have varying compensation levels despite working with the same wholesale partners.

For example, one might get paid 1% for each loan, while another gets paid 2.5%. The broker earning less will have a lower rate for you!

If you take the time to ask, or simply put your foot down, someone will come up with something better than the next guy/gal.

If you don’t bother attempting to negotiate, you’ll never know what’s possible. If the lender says they can’t budge, move on to one that will. It’s that simple.

Never accept the first rate you’re shown, like anything else in this world.

It doesn’t hurt to ask for lower, especially when it comes to a mortgage. After all, you could be saving money every month for the next 30 years.

7. Lower Your Max Purchase Price

If you want to save money, you might have to make some concessions. That could mean lowering your max purchase price if you’re in the market to buy a home.

I’ve already noted that it could be wise to lower your maximum price threshold on those Redfin and Zillow apps in anticipation of a bidding war. Or perhaps a higher-than-expected mortgage rate.

And while there’s no clear correlation between home prices and mortgage rates, a higher home price will obviously drive up your monthly housing payment.

Either lower your max bid or negotiate more with the seller, or do both. If you can secure a lower purchase price, you’ll need less mortgage. That lower loan amount will save you money.

It’s important to negotiate on the home’s purchase price AND the mortgage. Don’t concede in any area along the way if you want to save money.

Also negotiate with your own real estate agent! Sure, they are on your team, but they also need to fight for you. And do what it takes to seal the deal.

You can also input a higher mortgage rate than necessary when shopping to stay within budget, in case rates go up even more.

8. Consider a Second Mortgage

Back in the early 2000s, it was common to take out a first and second mortgage concurrently, with the latter known as a piggyback mortgage.

The purpose was to keep the first mortgage at a loan-to-value (LTV) of 80%, thereby avoiding PMI and costly price adjustments. This method could also be employed to stay at/below the conforming loan limit.

If your down payment is limited, it could make sense to tack on a second mortgage to save some dough.

The blended rate between first and second mortgage sans PMI and higher pricing adjustments could be just the ticket to savings.

If you’ve been considering a cash out refinance, but don’t want to lose your low fixed rate, a standalone HELOC or fixed-rate second mortgage such as a home equity loan could help you keep your first mortgage intact.

And with the Fed still expected to cut rates a couple more time this year, the HELOC rate should move lower over time.

9. Pay It Back Faster

I dedicated an entire article to this one recently. If mortgage rates are high, it makes sense to pay back the mortgage faster.

But if your fixed-rate mortgage is super low, well, take your time in paying back your loan. Or at least don’t rush it. After all, you might earn more on your money in a high-yield savings account.

So why pay it back faster? It’s simple really – the faster you pay the mortgage, the less interest you pay.

You basically want to pay back a low-rate mortgage as slowly as possible, and a high-rate mortgage as quickly as possible, assuming there aren’t better places for your money.

For example, if you get stuck with a pesky 7% mortgage rate, which is actually pretty decent historically, you can make extra payments each month to lessen the blow.

It’s possible to pay more each month to offset the higher rate and effectively turn it into something like a 4% mortgage rate.

10. Let It Ride

Lastly, you could wait things out and/or float your mortgage rate if you’ve already applied. You don’t have to accept today’s rates if you’re not entirely happy with them.

Most economists expect mortgage rates to move lower throughout 2025, but as I’ve said a few times in the past, we’re often surprised at the time we least expect it.

Just consider the recent pullback after it seemed mortgage rates were headed back to the 5% range. Once the spring home buying season wraps, rates could reverse course.

Typically when new highs are being tested, there are periods of relief along the way. And vice versa. They may not last very long, but it is possible to experience dips and opportunities.

Of course, this can be a risky game to play. But if we’re talking about a refinance, which is entirely optional, you can bide your time and only strike when the timing is right.

Keep an eye on the market, mortgage rate data, and look out for trends and try to lock your interest rate accordingly (how to track mortgage rates).

Bonus: Apply for a Mortgage in February

After some research looking at historical data, I discovered that mortgage rates tend to be lowest in winter, especially in the month of February.

This is typically a slower time of the year for mortgage lenders, and when they’re not as busy, they may lower their rates to drum up business.

In other words, passing more savings onto their customers instead of keeping their rates elevated.

So you might be able to shave an additional .125% or .25% off your mortgage rate if you apply in the later months of the year. This isn’t always true, but it’s something to consider if you’ve got time or flexibility.

It’s actually beneficial for another reason – other than a potentially lower rate, things should be quieter.

This means you might get a more attentive broker/loan officer and a smoother loan process that could move along quicker.

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026

- Light Data Week Means Mortgage Rates Will Be Dictated by Middle East - July 20, 2026

There’s a lot of good help with this article. Credit improvement is helpful and obviously even if someone is a first-time borrower they should know that they have to resolve 30-day late payments on their credit report prior to closing. Take advantage of the option of shopping interest rates. One argument I had with this article is mortgage insurance is not always a bad thing. It’s a minimal cost that you can ask grow into your monthly mortgage payment and should something go wrong you always have the safety net of something able to pay your mortgage payment until you get back to work and have a paycheck once more. It may not be a priority but it’s not always a bad thing.

Charlie,

This is in reference to PMI, which protects mortgage lenders, not the insurance that protects borrowers if they’re unable to make payments.