Everything has been coming up roses for mortgage rates in 2026, but that could soon change if the Greenland situation spirals out of control.

At the moment, 30-year fixed mortgage rates are hovering around 6%, which is basically a three-year low.

That led to a surge in home loan applications last week, with both existing homeowners looking to refi and prospective home buyers jumping in.

Ironically, President Trump’s latest proposal to buy $200 billion in mortgage-backed securities (MBS) got us there.

But his latest threat to impose new tariffs on numerous European countries could send mortgage rates higher again.

New 10% Tariffs Threatened If Greenland Can’t Be Purchased by the U.S.

You’ve likely heard of the threats to take Greenland from Denmark, with Trump floating a new round of tariffs if they don’t agree to a sale.

In a Truth Social post, he said, “Starting on February 1st, 2026, all of the above mentioned Countries (Denmark, Norway, Sweden, France, Germany, The United Kingdom, The Netherlands, and Finland), will be charged a 10% Tariff on any and all goods sent to the United States of America.”

“On June 1st, 2026, the Tariff will be increased to 25%.”

This is in reference to the aforementioned countries visiting Greenland “for purposes unknown” and impeding a sale to the United States.

Trump has argued that the purchase of Greenland is imperative for “Safety, Security, and Survival of our Planet.”

And that countries like “China and Russia want Greenland, and there is not a thing that Denmark can do about it.”

Long story short, Trump wants to buy Greenland and if Denmark and its apparent European allies stand in the way, a new round of tariffs will be unleashed.

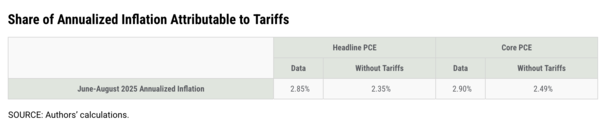

While we can argue whether or not tariffs cause inflation until the cows come home, the St. Louis Fed laid out a pretty good case.

Per the St. Louis Fed, “Over the June-August 2025 period, tariffs explain roughly 0.5 percentage points of headline PCE annualized inflation and around 0.4 percentage points of core PCE annualized inflation.”

Not to mention Fed chair Powell said last summer that they weren’t able to cut rates as freely as possible because of the unknown impacts of the tariffs.

So whether you believe tariffs cause inflation or not, there’s a decent argument they keep interest rates higher than they might otherwise be (CPI vs. mortgage rates).

Mortgage Rates Don’t Exist in a Vacuum

About a year ago, we saw mortgage rates go on a rollercoaster ride thanks to the on-again, off-again tariffs.

But they were arguably stuck at higher levels because of tariffs or the threat of new tariffs.

We saw the 30-year fixed climb above 7% on several occasions last year, leading to another dismal year for home sales.

Once a lot of that talk began to wane, and inflation data continued to cool, mortgage rates began moving lower.

Today, they’re about one full percentage point below those year-ago levels, but that’s in part due to worsening labor (jobs reports) and perhaps many of Trump’s policies now baked in.

And as mentioned, the latest proposal for Fannie and Freddie to buy billions in MBS to lower mortgage rate spreads.

However, mortgage rates don’t exist in a vacuum and the MBS deal could be completely overshadowed by this new tariff threat.

As the St. Louis Fed noted, tariffs accounted “for a meaningful share of recent inflation.”

The threat of new tariffs (and larger ones) means inflation estimates could get murky and the Fed might pull back on additional rate cuts.

In the meantime, 10-year bond yields could move higher on the uncertainty, pushing the 30-year fixed higher in the process.

The beneficial effects of the MBS buying could be completely absorbed and we could see mortgage rates climbing back into the 6s instead of falling deeper into the 5s.

As I’ve said many times, this would be yet another gut-punch for prospective home buyers (and sellers) and the housing market at large.

So hopefully we get some clarity on this situation ASAP to avoid ruining yet another spring housing market.

(photo: David Stanley)