I talk about mortgage rates a lot because I know they are top of mind for home buyers (and existing homeowners).

Even if the difference in monthly payment is negligible, consumers seem to be obsessed with mortgage rates.

It’s why we see headlines constantly, and weekly surveys, and daily rates posted everywhere.

There’s this odd fascination with mortgage rates and even a rivalry amongst homeowners to secure the lowest rate possible.

And the reason why, in my view, is homeowners are highly emotional and that magical rate means a lot, even if the difference in payment amounts to little.

66% of Prospective Home Buyers Won’t Buy If Mortgage Rates Rise

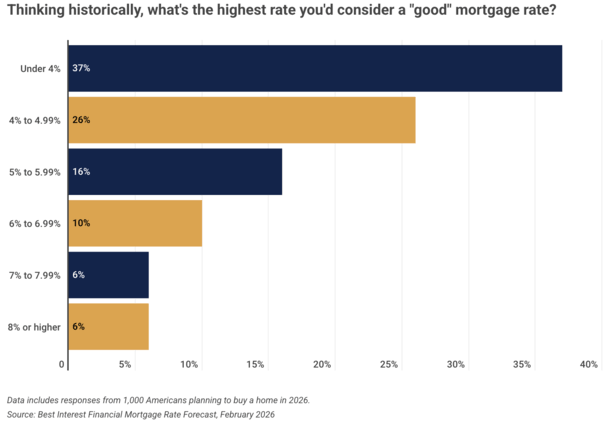

That brings me to a new survey from Clever Real Estate and Best Interest Financial, which polled 1,000 American adults who plan to purchase a home this year.

The poll was conducted in early December, when the 30-year fixed averaged roughly 6.25%.

That’s pretty much where it stands today as well, despite a nice little short-lived drop in early January when Trump announced a new MBS buying program.

What stood out in the survey was the fact that two-thirds of those surveyed would postpone a home purchase if “mortgage rates rise even slightly from today’s level.”

Yes, you read that right. If mortgage rates increase just a little bit, the majority of home buyers are out!

This illustrates just how emotional today’s home buyers are, not to mention fickle.

Now it’s always wise to take a survey with a grain of salt because what respondents say and what they do might be completely different.

But it does give you pause about this so-called “housing market reset” we’re supposed to experience this year.

And it does make you wonder how strong the housing market is if it all boils down to mortgage rates.

The Housing Market Is Fragile and Might Not Be Able to Absorb Another Mortgage Rate Shock

I’ve said for a while that the housing market is fragile and that all those moments where mortgage rates rose back above 7% were a gut-punch for prospective buyers.

And yes, it’s mostly psychological. But we saw this happen last year due to tariffs and a wider trade war.

It took place in spring no less when the most prospective home buyers were out and about looking to take the plunge.

It also happened in the spring 2024 when the 30-year fixed climbed above 7.50% briefly, taking the wind out of the housing market’s sails then too.

So if it were to happen this year, or even if the 30-year fixed were to climb back above 6.50%, it could spell disaster.

The more this has happened, the less home buyers can bear. It’s like being dragged under water time and time again, leading to exhaustion and the inability to withstand another barrage.

Simply put, home buyers can’t take it anymore so we really need mortgage rates to settle in at current levels (or lower) and stop with the up and down stuff we’ve seen the past few years.

Monthly Payment Difference Is Negligible, But Emotional Impact Is Big

If we consider a 30-year fixed with a $500,000 loan amount set at 5.99%, the monthly principal and interest payment is roughly $2,995.

Meanwhile, a rate of 6.25% for the same scenario is about $3,079, or just $84 higher per month.

I think if you asked a prospective home buyer to pay $84 more per month they’d likely say sure, no problem.

They might not be thrilled to pay more, but they would be able to handle it.

However, when they see a rate of 5.99% versus 6.25%, their mind might begin to play tricks on them.

That 5.99% looks way more appealing than that 6.25%, even if the monthly payment isn’t much different in the grand scheme.

And this survey highlights just how important home buyer psychology is.

If it came down to it, I doubt many would care about an additional $80 if it meant securing their dream home.

But the messaging is important. People want to believe they’re getting a good deal and not overpaying for a home.

- Mortgage Rates Hit 2026 Highs, Look Headed Back to 6.50% - March 19, 2026

- A Home Builder Is Offering to Cover Your First 12 Mortgage Payments - March 18, 2026

- Pending Home Sales Eke Out a Beat Thanks to Lowest Mortgage Rates Since 2022 - March 17, 2026