Well, it looked like the 30-year fixed was destined for the 5s until it didn’t.

We were ever so close when 10-year bond yields nearly breached 4% earlier this week.

But just like that, the 10-year, which serves as a bellwether for mortgage rates, snapped back to 4.10%.

That meant a national average sub-6% mortgage rate would have to wait, again…

However, we are hovering very close to that key threshold and it might just be a matter of time.

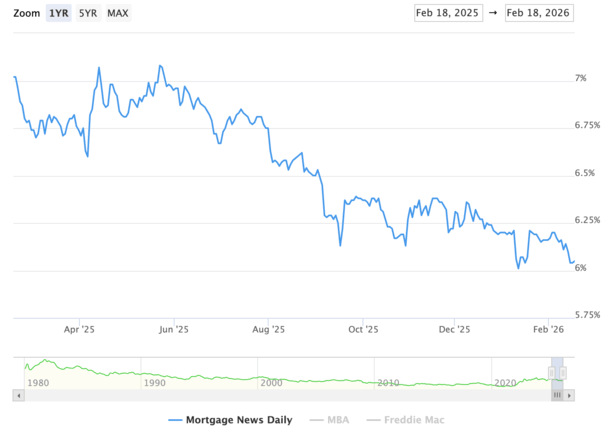

The Elusive Mortgage Rate That Starts with a ‘5’

There seems to be a lot of resistance at the 5/6% barrier for the 30-year fixed, just as there has been for the 10-year bond yield at 3/4%.

Whenever we get close, we seem to take a step back. The widely cited daily survey from Mortgage News Daily has been stuck just above the 5s for much of 2026.

At last glance, just five basis points above that key level.

Meanwhile, Freddie Mac’s weekly Primary Mortgage Market Survey® (PMMS®) it at three-year lows, averaging 6.01% this week, but still just north of the 5s.

It’s not that being in the 5%-range would do anything materially different for monthly mortgage payments.

After all, a rate of 6% versus a rate of 5.875% would only amount to $32 per month on a $400,000 loan amount.

Clearly that wouldn’t make or break a home purchase, and probably shouldn’t sway a mortgage refinance either.

But it could send a signal to prospective home buyers (and existing homeowners pondering a refinance) that mortgage rates are low again!

So it’s more a psychological thing than it is a monetary thing. If you can afford to buy a home with a 5.875% mortgage rate, you can afford to buy a home with a 6% mortgage (I hope!).

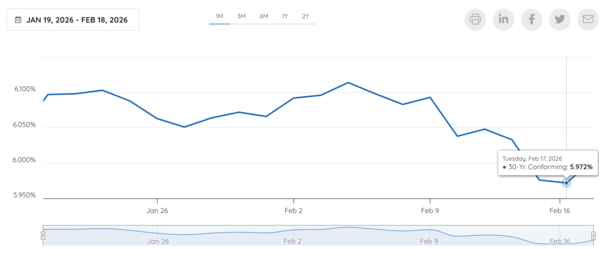

Optimal Blue Mortgage Rates Went Sub-6% This Week (Actual Rate Locks)

Of course, it depends what mortgage rate gauge you use.

I look at several, including Optimal Blue’s Mortgage Market Indices (OBMMI), which is calculated from actual locked rates from consumers nationwide.

They actually got that highly-sought after sub-6% rate both on Friday of last week when it hit 5.976%, and this week when it hit 5.972%.

The thing is, nobody cites this index in the media so you’ll never hear about it.

And because you need that headline “Mortgage rates fall below 6%” on the front pages, it won’t mean much.

Of course, it was the lowest level seen since 2022, the same year the 30-year fixed was in the 3% range.

So clearly mortgage rates have made some serious progress since ascending to 8% in late 2023.

But they are still about double the levels seen in early 2022, which presents an ongoing affordability problem.

Does the Housing Market Need a Sub-6% Mortgage Rate to Get Going?

Perhaps that’s why the housing data released thus far in 2026 has been pretty dismal.

Last week, we got existing home sales from the National Association of REALTORS, which came in a lot lower than expected, showing an 8.4% decline in January from the month prior and 4.4% year-over-year.

And today, NAR told us that pending home sales (new signings) fell 0.8% in January MoM and 0.4% YoY.

Not exactly the hot start we were all hoping for in the New Year, given these tend to close within one or two months of the signing (aka March and April).

I don’t know what the excuse was for lackluster existing home sales in January, which typically includes contracts signed in November and December, but you might be able to blame the weather for January’s pending sales.

It’s just that we’re beginning to run out of time since next week will practically be March!

So if the housing data doesn’t get better, one might start to worry that 2026 will be another dud, with home sales continuing to sit near the lowest levels in 30 years.

This is why I want to see a sub-6% 30-year fixed. To determine if it can provide that much-needed spark for home buyers (and sellers) in 2026.

- Mortgage Rates Get Relief Thanks to Jerome Powell! - March 31, 2026

- How Mortgage Rates Could Have a Winning Week - March 30, 2026

- Are Mortgage Rates Approaching a Top? - March 27, 2026