Just a day after a “blowout” jobs report was released, mortgage rates are falling again.

I noted yesterday that mortgage rates did a very good job navigating what could have been a bad day.

Instead, they held firm and didn’t see a big pop as might be expected when jobs numbers greatly exceed expectations.

And today things got even better for rates as the 10-year bond yield slid nearly six basis points.

That means 30-year fixed mortgage rates remain very close to 6% and can still slip into the 5s soon if conditions warrant it.

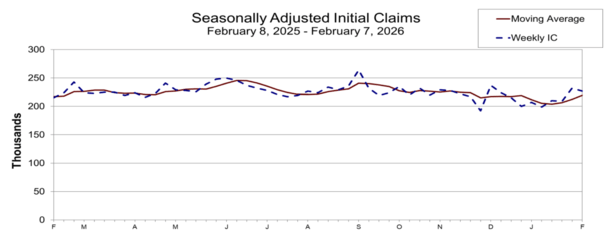

Jobless Claims Come in Higher Than Expected, Pushing Mortgage Rates Lower

We got more jobs data today courtesy of the weekly jobless claims from the U.S. Department of Labor.

They reported that seasonally adjusted initial jobless claims totaled 227,000, above the 225,000 expected but below the previous week’s revised level of 232,000.

That was apparently enough for bond yields to improve, though other factors could be at play, such as the CPI report coming tomorrow.

Remember, mortgage rates can move lower when inflation is less of a threat.

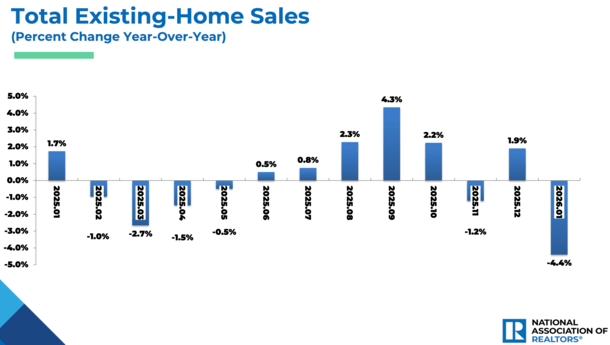

Or the fact that existing home sales came in ice cold for January, with a sales pace of just 3.91 million versus a forecast of 4.15 million.

Home sales were also down 4.4% compared to a year earlier, one of the worst prints in recent history.

Note that existing home sales are based on actual closings from Multiple Listing Services (MLSs) and likely went under contract in November and December.

Mortgage rates improved quite a bit since then and January saw mortgage rates in the sub-6% category for the first time in several years.

So it is possible we see a bump in February as those transactions close…

CPI Could Further Help Mortgage Rates Tomorrow

It’s been a busy week for data thanks to the government shutdown. And it culminates with the January CPI report on Friday.

The forecasts are calling for relatively stable inflation numbers, including a 0.3% month over month increase, which would be the same as the December reading, along with a 2.5% year-over-year increase.

One thing to keep an eye on is tariff-related inflation. The Fed will generally be okay with that as it’s viewed as a one-time pass-through event.

We just don’t want to see a reacceleration of inflation, especially if job growth is questionable as well.

But if we get a decent CPI reading, that coupled with the jobs “victory” could push 30-year fixed rates ever closer to the 5s.

I got to thinking that the way mortgage lenders absorbed the hot jobs report tells me they’re more comfortable with interest rates at these levels.

Had it been 2024 or even last year, mortgage rates may have skyrocketed on a big jobs beat.

That tells me it’ll be easier to withstand hot reports and perhaps easier to keep inching lower into the 5s if reports come in cooler-than-expected.

This is especially true because 10-year bond yields are higher today to compensate for current conditions and mortgage spreads are tighter.

That means there’s room for bond yields to ease if economic data is cooperative, and taken together with tighter spreads, could get us that long sought-after 5% mortgage rate!

Read on: Do mortgage rates change daily?

- Are Mortgage Rates Approaching a Top? - March 27, 2026

- Better and Coinbase Launch Token-Backed Mortgages - March 26, 2026

- Mortgage Rates Will Soon Be Above Year-Ago Levels - March 25, 2026