The latest mortgage Q&A: “Do mortgage rates change daily?”

It’s that time again folks, where I answer your burning mortgage questions.

Mortgage rates are hot news right now. After the 30-year fixed surpassed 8% in October, a near-21st century high, it has since come down to below 7%, though just barely.

The hope is this trend continues into 2024 and rates eventually dip below 6%.

But as always, expect the unexpected when it comes to mortgage rates or you’ll be caught off guard.

Lately, mortgage rates have been extremely volatile as a result of ongoing inflation concerns, the end of the government’s MBS buying program, and the economy at large.

So when shopping for a home loan, it’s now more important than ever to keep a close eye on rates, because they can and will change daily (learn more about how mortgage rates are determined).

Mortgage Rate Sheets Are Printed Monday Through Friday

- New lender rate sheets are released daily throughout the week

- Monday through Friday unless it’s a holiday (not on weekends)

- Sometimes interest rates will be different, sometimes they’ll remain unchanged

- It depends what transpired the day before and/or the morning of the release

Each morning, Monday through Friday, banks and their loan officers get a fresh “mortgage rate sheet” that contains loan pricing for that day.

I know because when I first started in the industry, I got tasked with handing them out to fellow employees (back when we used paper).

I’ll never forget kicking the printer every time it broke, which as far as I can remember was also Monday through Friday.

Anyway, these rate sheets contain the day’s mortgage rates, which are critical to anyone working in the biz.

Without them, loan officers can’t provide quotes to borrowers unless they’re using some sort of computer system, which is likely now the case for many.

Whether on paper or digital, mortgage rate pricing is updated daily based on market conditions. This is no different than how stock prices or bond prices fluctuate.

For example, if the jobs report is released on Friday and shows a huge jump in unemployment, rates should fall (weak economic news is good for interest rates).

But if the same report reveals that wages surged, this is bad for rates because it implies that inflation is rising.

Long story short, root for bad news if you want rates to be lower.

Mortgage Rates Can Change Throughout the Week

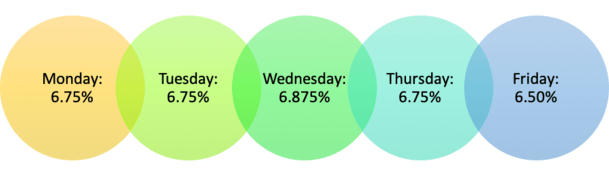

Here’s a hypothetical look at how mortgage rates could change from Monday to Friday.

Imagine you’re doing some mortgage rate shopping and the 30-year fixed is priced at 6.75% to start the week.

You aren’t thrilled about the rate and you heard a weak jobs report is coming Friday. It’s a risk, but you’re okay with floating your rate until then because you don’t close for a few weeks anyway.

On Tuesday, rates remain unchanged, but then they inch up an eighth point on Wednesday. Go figure!

But Thursday sees rates fall back to Monday’s levels. And on Friday, rates rally and drop a full quarter percent.

You like what you see and lock the 6.50% rate. Things worked in your favor!

Note that this is just one possible scenario. Rates could also move higher during the week or do nothing at all.

Each Loan Program Gets an Updated Price Daily

All loan programs offered by a given bank will be featured on their rate sheets or in their pricing engine.

This includes fixed-rate mortgages like the 30-year fixed and 15-year fixed, along with other loan types such as adjustable-rate mortgages.

The same goes for jumbo loans, FHA loans, VA loans, and any other loan programs offered.

Each type of loan will have its own section on the rate sheet with corresponding pricing for that day.

This details how many discount points must be paid, or conversely, if a lender credit is offered at a certain rate.

There will be a date on these rate sheets that makes it clear that the pricing pertains to that day only.

In terms of daily rate movement, expect fixed mortgages to move more than ARMs on a 24-hour basis seeing that the latter come with initial teaser rates and the former are fixed for up to three decades.

You might also see a slight difference in pricing between conforming mortgages backed by Freddie Mac and Fannie Mae, even though they’re nearly the same product.

So ask for pricing on each if both are offered. Usually, a seasoned loan officer or broker will do this on your behalf.

These rate sheets are also what mortgage brokers rely on to get pricing updates from the banks and wholesale lenders they work with.

Check Out Daily Mortgage Rates on Lender Websites

- It’s okay if you don’t have access to lender rate sheets

- Visit lender websites to access their daily mortgage rates if published

- Keep track of them over time and make note of any changes

- This can be helpful to determine their direction or any obvious trends

If you’re a consumer without access to mortgage lender rate sheets, don’t fret. You can visit their websites daily instead to see both home purchase and refinance rates.

While typically updated each day, these aren’t as reliable as an actual rate quote because they make lots of assumptions.

This is similar to an ad for a monthly car payment that requires X down payment and Y credit score.

But you can at least glean some information, like mortgage rate trends if you see that they’re rising or falling over time. Just know trends can reverse quickly.

Prospective home buyers may want to bookmark some of these pages that feature today’s mortgage rates to chronicle them over time and stay in the know.

Mortgage rates can change daily, but only during the five-day workweek.

This is similar to the stock market or any other financial market for that matter. They’re constantly in flux and as such, pricing can change from day to day, potentially by a lot.

While mortgage rates do not change during the weekend, pricing can definitely be a lot different between Friday and Monday depending on what happens between then.

In other words, pricing you receive on Friday could differ tremendously from the pricing you receive on Monday if something takes place over the weekend. Or if a big report or news story is released Monday morning.

Ask for Mortgage Rate Updates Daily

- Ask for rate updates daily until you lock in your rate

- Rates can move higher or lower based on a number of factors

- Economic news, weekly/monthly reports, trading trends, and even geopolitical activity

- All of these can significantly impact rates throughout the week

If you’ve decided to float instead of lock your mortgage rate, you’ll need to track rates daily.

This means waking up every day and checking rates, similar to how you’d check your stock portfolio.

The best way to know where mortgage rates are for a given day is to call your bank or broker and ask.

Don’t be afraid to call every day to keep track of mortgage rates, as it’s their job to keep you informed.

Sure, they might be annoyed that you’re constantly asking for updates, but it’s their duty to provide you with this information.

And it’s probably one of the more important jobs they’re tasked with once the loan application has been submitted.

Pricing is paramount and they should be able to guide you accordingly. The good LOs and brokers track MBS prices daily and pay attention to rate trends.

Can Mortgage Rates Change After I Apply?

Absolutely, and if you don’t lock your rate when you apply, you are subject to those market changes until you do.

Don’t just assume that the last rate quote they gave you, or the initial one to get you in the door, still stands. It could be completely different a week or even a day later.

Of course, rates can move up and down, so sometimes waiting can be beneficial.

Other times, it’s best to lock in the rate and not take chances. For example, if rates are super low and not expected to get much better.

When applying for a home loan, you’ll be given the option to lock in your rate or float it until you’re ready to lock.

Those who choose to float their rate (as opposed to lock) will need to pay attention to daily rate movement until they do lock.

Conversely, those who lock won’t have to worry what rates do thereafter, assuming they close their loan by the lock expiration date.

Simply put, your mortgage rate is subject to change until it’s locked. Once you do lock in your rate, be sure to get written confirmation.

It’s extremely important because it will determine how much you pay each month and over the life of the loan.

And if you’re just barely scrapping by eligibility-wise, you won’t want to chance mortgage rates going up between application and loan closing.

Tip: Freddie Mac’s weekly survey just details what rates average during the week from several lenders, not necessarily the daily rate available to you.

Mortgage Rates Can Change During the Day

- Intraday mortgage rate changes are also possible during periods of volatility

- This can happen if significant economic events take place during market hours

- Like Fed meetings, major policy changes, or unexpected geopolitical events

- These can affect demand for bonds and/or mortgage-backed securities (MBS)

So we know mortgage rates have the ability to change on a daily basis. But sometimes mortgage rates may even change more than once during the same day if major economic reports are released.

Things like Federal Reserve meetings (check their schedule), the monthly jobs report, or a big bump in the 10-year Treasury yield or MBS prices may cause rates to rise or fall from morning to afternoon.

This could result in a .25% swing on the 30-year fixed, pushing it from 6.50% to 6.75%. Or the rate could fall from 6.50% to 6.25%.

And that could greatly impact what you pay each month for the next untold number of years.

In other words, your interest rate is never really secure until it is locked and you receive written confirmation from the lender.

For example, a mortgage rate quote provided in the morning may no longer be valid that same afternoon.

If you drag your feet and tell the loan officer you’ll get back to them, even if just hours later, the rate may be ancient history.

So pay close attention to the economic calendar to see what might transpire in a given week.

There’s No Guarantee Until It’s Locked!

Remember, if you want a guaranteed interest rate on your mortgage, you need to lock it in.

By locking, I mean speaking with your mortgage broker or loan officer, agreeing on certain terms, and getting confirmation in writing!

I can’t stress this enough; often times borrowers will be “promised” a certain interest rate or simply be told that interest rates are “X” and not to worry.

But when it comes time to close the loan, for whatever reason, interest rates may have gone up, and the promised rate is no longer available, often putting the borrower in a tough spot.

If rates increased, borrowers just bite the bullet and reluctantly agree to the new rate because they’re so far along in the loan process.

That’s why it’s imperative to lock in your mortgage rate when you’re comfortable with it.

Finally, be sure to take the time to compare rates and compare lenders too.

All too often, a borrower will just fill out a single mortgage application and call it a day. That’s fine if you don’t care about saving money, but my guess is you do care.

Take a moment to calculate the difference between two rates that are just an eighth or quarter apart using a mortgage calculator.

You might be shocked at the difference in interest over the life of the loan, which should illustrate the importance of putting in the time to shop mortgage interest rates.

Read more: What mortgage rate can I expect?

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026