It’s been an eerily quiet week or so for mortgage rates.

Almost too quiet, as if you think something’s lurking around the corner.

After a very volatile March (when they surged higher) and much of April (when they surprisingly recovered), they’ve done basically nothing.

It makes you wonder what comes next and what the catalyst could be, if anything at all.

Mortgage Rates Have Been Strangely Flat Lately

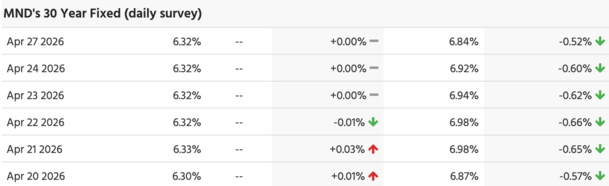

It’s been a very uneventful week or so for mortgage rates after they experienced major volatility for two straight months.

They jumped from sub-6% levels in early March all the way up to around 6.625%.

Then recovered nicely to around 6.30% in the month of April, which isn’t bad considering the war in the Middle East still very much hangs in the balance.

And oil remains at over $100 per barrel, if not even higher. But have since done very little, as evidenced above from MND’s daily rate index.

The latest development on that front was the UAE leaving OPEC, a signal that the Strait of Hormuz issue likely won’t be resolved quickly.

So countries are taking matters into their own hands, and in the UAE’s case, it was an opportunity to break free and play by their own rules.

But it could also mean even more tension in the region and greater uncertainty for energy markets moving forward.

That could eventually mean increased production and lower prices, but more geopolitical unknowns in a region now feeling much less stable.

Jobs Report Next Friday Is the Biggie

The Middle East situation will continue to be the wildcard, though 10-year bond yields haven’t done much for about a month.

It seems to be a wait-and-see approach there, which would explain why the 30-year fixed simply drifted lower thanks to tighter spreads.

But that could change next Friday, May 8th, when we get the April jobs report.

The Fed has been more focused on labor than inflation and with Powell set to lead his last meeting as Fed chair this week, it might be an important data point for incoming chair Kevin Warsh.

Everyone expects Warsh to be more dovish and push for cutting rates and if he gets a soft jobs report, it gives him a stronger argument to cut sooner.

If that jobs report comes in hot, then he’ll have a tougher time convincing his fellow Fed members to resume cutting.

So arguably this jobs report comes at a crucial time for the changing of the guards, with Warsh expected to take over in mid-May.

The Fed doesn’t set mortgage rates, but they rely on economic data and if it’s weak, bond yields will react to Fed rate cut expectations.

If you’re rooting for lower mortgage rates, you’ll want a cold jobs report with fewer jobs created and higher unemployment.

Yes, that’s cynical, but that’s the only way to get mortgage rates lower right now outside of a major positive development in the Middle East.

Lock or Float Right Mortgage Rates Right Now?

I spoke about locking vs. floating a mortgage rate the other week and basically my stance hasn’t changed too much.

Given rates are still pretty low if we zoom out, just above 6.25% for a 30-year fixed, it’s hard to see a ton of downside potential.

Remember that a sub-6% rate was basically the best we had seen in 3.5 years, right before mortgage rates doubled from 3% to 6% in early 2022.

So they’ve made a ton of progress since then, especially since we had near-8% rates in late 2023.

And with $110-barrel oil and lots of unknowns regarding the Middle East, one could argue that rates about .25% higher than these lows aren’t too shabby.

Sure, they could improve further, but how much further? Another .125%? It would be hard to imagine they return to sub-6% with the current state of affairs.

I continue to think we’re pretty lucky they’re as low as they are all things considered.

Conversely, if things sour they could re-test recent levels of 6.50% to 6.75% or higher, especially since mortgage rates are historically highest in spring!

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026