I’ve long said that the banks weren’t interested in mortgages anymore.

Their distaste for home loans probably began post-2008 when several were forced to close their doors. Remember Bear Stearns, Wachovia, or Washington Mutual?

Others had to take massive losses due to faulty loans that should have never been made, leading to new regulations put in place to avoid a similar disaster.

While those new rules have served their purpose, over time more and more nonbanks have entered the fray.

And with the product menu dominated by agency-backed loans, mortgages have more or less became a commodity.

This pushed former mortgages heavyweights out of the game, allowing nonbanks like Rocket and UWM to thrive.

A new proposal to adjust capital requirements for banks could change that. And that could be yet another tailwind for mortgage rates.

Banks Have Lost Interest in Mortgages

It’s no secret that banks just don’t love mortgages anymore. Aside from the fallout of the early 2000s housing crisis, mortgages became pretty homogenous.

Just about every loan these days is a boring old 30-year fixed-rate mortgage backed by either Fannie Mae, Freddie Mac, or Ginnie Mae (VA/FHA/USDA).

In other words, you can get the same mortgage anywhere, and many non-banks are faster and less bureaucratic than the banks.

They also just want to originate your mortgage and move on. Banks, on the other hand, want to cross-sell and get you to open a checking and/or savings account and make a deposit.

The problem is today’s consumers aren’t interested. Sprinkle in increased risk and stringent capital rules and banks have largely thrown in the towel.

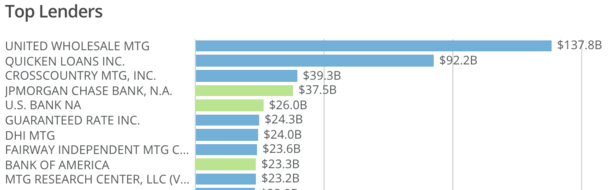

This explains why the top mortgage lender in the nation is a nonbank, a wholesale nonbank no less.

I’m referring to United Wholesale Mortgage, which knocked Rocket Mortgage off its perch in 2024, as seen in the chart above from Richey May.

Before that, San Francisco-based Wells Fargo was the king of mortgages. But they dealt with a series of lawsuits that led to them intentionally reducing their mortgage footprint.

At present, only three of the top 10 mortgage lenders in the nation are banks.

Lots of Banks Have Stopped Mortgage Lending Entirely

We’ve seen several banks exit mortgage lending in recent years, including Seattle-based WaFd because it wasn’t worth the risk (they cited holding their loans versus nonbanks selling them off immediately).

More recently, Popular Bank stopped making mortgages, as did Ally Financial.

And just this month, Amalgamated Bank said it is directing customers seeking a mortgage to use its new nonbank partner Embrace Home Loans.

It’s understandable between the lack of profit, the capital constraints, and the nonbanks beating them on price, technology, and execution.

Maybe that will change though.

Easing Capital Requirements for Banks Could Lead to a Mortgage Boom

During a speech at the American Bankers Association 2026 Conference for Community Bankers, Federal Reserve Vice Chair for Supervision Michelle W. Bowman said they’re looking at ways to get banks back in the game.

She noted that in 2008, banks originated about 60% of all mortgages and held servicing rights on 95% of balances.

By 2023, banks originated just 35% of mortgages and serviced only 45% of outstanding balances.

Aside from nonbanks dominating the space, they are also seen as higher risk because they aren’t depository institutions.

To entice banks, Bowman noted that they could adjust existing capital framework that “would increase bank incentives to engage in mortgage origination and servicing.”

The end result might be big banks vying for your loan again, which could mean greater access to loan options and possibly lower mortgage rates.

Simply put, if there’s more competition for your mortgage, chances are rates will be lower.

And because banks hold loans on their books, they can offer options beyond the same old boring Fannie, Freddie, and FHA stuff.

Perhaps competitive adjustable-rate mortgages, jumbo loans, or outside-the-box loans with more flexible underwriting (within reason).

Either way, more players in the space would boost your chances of landing a better deal on your mortgage.

Read on: Who are the top bank mortgage lenders in the country?

- Mortgage Rates Get Relief Thanks to Jerome Powell! - March 31, 2026

- How Mortgage Rates Could Have a Winning Week - March 30, 2026

- Are Mortgage Rates Approaching a Top? - March 27, 2026