Over the weekend, the United States and China reached a temporary deal to cut tariffs tremendously.

Instead of an astronomical 145% rate, the U.S. will now impose a much more reasonable 30% rate on imports from China.

This should get business (and ships) moving again, though it should be noted that it’s only a 90-day pause.

Investors cheered the news, believing more severe economic fallout such as a recession could now be averted.

But the risk-on move has hurt bonds, and by nature mortgage rates, which have seen reduced demand in the process.

Risk-On Trade Means Mortgage Rates Might Go Higher

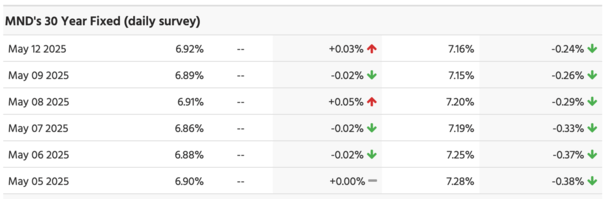

At last glance, the 10-year bond yield was about 20 basis points (bps) higher than it was before the trade deals began being reported last week.

We got a U.K. trade deal on May 8th, which resulted in a bump, followed by a China deal today, which led to another bump up.

Mortgage rates correlate very well with the 10-year bond yield, and as such have risen a bit as well.

However, because of the trade deals and the perceived reduction in volatility, mortgage spreads have improved to offset those gains.

So some of the increase you’d expect from higher bond yields means mortgage rates aren’t actually much higher.

Ultimately, the 30-year fixed has been pretty flat over the past week, at least according to MND.

We’re basically just hovering around 6.875% to 6.90%, where we otherwise might be pushing 7% again.

In other words, the trade deals are semi-neutral for mortgage rates at this juncture.

The market is kind of digesting it as a return to normalcy, which isn’t majorly bullish or bearish for mortgage rates.

At the same time, it’s important to remember this a temporary deal and before long, folks will be asking questions about what happens next.

This could mean relatively flat interest rates for the rest of the second quarter as investors take a wait-and-see approach.

Economic Data Will Matter Again, with an Asterisk

With the trade tensions and tariffs now off the boil, economic data will retake center stage.

This means things that normally matter to mortgage rates, like the jobs report and the CPI report will dictate the direction of rates again.

Speaking of, CPI is due out tomorrow and that will be something to watch to determine how inflation is doing.

The one problem though is because of the past couple months, we might see anomalies in the economic data.

Will we see an uptick in inflation related to supply chain disruptions? Will we see an increase in unemployment?

What will economists make of it? Will they write it off as a temporary trade-related issue and not something to take too seriously?

And what about the Fed? How will Jerome Powell and company look at this data as it is unveiled?

If anything, it could push out any expected policy decisions as the data smooths and tells a clearer story.

That too could mean stubbornly flat mortgage rates for the next few months, at a key time of the year when home buying is historically strongest.

It will also dampen refinance activity, especially rate and term refinances that are harder to pencil for recent home buyers.

But Mortgage Rates Could Still Trend Lower as the Year Progresses

- One major mortgage rate headwind has been removed thanks to the trade deal

- Just keep in mind it’s only temporary and could rear its head a few months from now

- In the meantime spreads could improve and rates may slowly tick down as economic data comes in each month

- But we might see stubborn movement through summer as caution remains and other issues like the spending bill surface

Despite what now feels like a little bit of a holding pattern for mortgage rates, they may slowly ease as the year progresses.

If we actually reach a permanent deal with China and get this tricky stuff behind us, the economic data will be the driver once more.

Even before the trade war got underway, economic conditions were clearly cooling. If they continue to show signs of cooling this year, interest rates might tick down as well.

Remember, slowing economy = lower mortgage rates, all else equal.

Perhaps more importantly, the Fed will be able to do its job with fewer distractions from big unknowns.

They’ll be able to look at the data in front of them to determine if rate cuts are necessary, without holding back because of the unknown economic effects of tariffs.

It’s basically one less headwind for mortgage rates, along with the possibility of tighter spreads. Two positives.

Ideally, what it looks like is gradual cooling while avoiding a full-blown recession, but even that can’t be ruled out. There’s also the big, beautiful bill to worry about.

What we might see is the Fed resuming rate cuts, which could be preceded by falling mortgage rates, similar to what we saw last August and September.

And that could get us closer to some of the 2025 rate predictions, including my own, that put the 30-year fixed mortgage closer to around 6% by year end.

(photo: Aidan Jones)

- Are Mortgage Rates Approaching a Top? - March 27, 2026

- Better and Coinbase Launch Token-Backed Mortgages - March 26, 2026

- Mortgage Rates Will Soon Be Above Year-Ago Levels - March 25, 2026