Mortgage Q&A: “Are mortgage points worth it?”

When taking out a mortgage, whether for a new home purchase or to refinance an existing loan, one decision you’ll have to make is if it’s worth paying mortgage points to obtain an even lower interest rate.

Before we get into that, it’s important to note that the term “points” gets thrown around loosely, and can refer to the loan origination fee and/or discount points.

The loan origination fee is the commission charged by the bank or loan officer in exchange for working on your loan, whereas discount points are optional costs used to buy down your interest rate.

It’s an important distinction because the loan origination charge is basically unavoidable (they need to eat, right?).

Whereas paying discount points (prepaid interest) is entirely optional depending on the interest rate you desire.

Note that not all lenders charge loan origination fees, but that could just mean the cost is already baked into the (higher) interest rate.

Either way, take the time to compare lenders’ rates and fees to ensure you get the best combination of both.

Key Takeaways on Paying Mortgage Points

- Discount points lower your mortgage rate in exchange for an upfront fee

- Example: Upfront cost of $5,000 to save $100/mo. on your mortgage

- This would take 50 months to break even and begin saving money

- If you keep the loan past the break-even period (cost ÷ savings) you “win”

- Be careful paying points if you think you’ll refi/sell in a short period

- Shop around to ensure paying points actually saves you money

- You could find a lender that offers a low rate without points

- High mortgage rates in 2025 makes paying points tempting, but a temporary buydown might be a better move if refinancing is likely

Jump to paying mortgage points topics:

– When You Break Even Determines If Points Are Worth It

– Factor in Your Tax Bracket and Savings Rates

– It Might Not Be a Good Idea to Pay Mortgage Points in 2025

– Make Sure Paying Points Actually Lowers Your Rate

– Situations Where Paying Mortgage Points Can Be Worth the Cost

– Benefits of Buying Mortgage Points

– Disadvantages of Buying Mortgage Points

Do You Want an Even Lower Mortgage Rate? Pay Points!

- You can obtain a below-market mortgage rate if you pay points at closing

- Points are a form of prepaid interest that reduce your interest expense on the loan

- Instead of paying more each month, you pay more upfront

- This will save you money over the life of the loan via reduced interest

Let’s assume you’re shopping for a $300,000 mortgage.

While mortgage rate shopping, you’ll probably pay the most attention to the big, glaring rate in front of you, such as 5.99%.

But if you look under that rate, or in the small, fine print, you should see more details about the rate, such as the fact that it requires you to pay two mortgage points!

[Watch out for rates you have to pay for!]

In this case, those two points are mortgage discount points, which lower the rate to that amazingly low 5.99% you see advertised.

But those two points will cost you $6,000, using our $300,000 loan example, as each point is equal to one percent of the loan amount.

If we’re talking about a larger loan amount, such as $500,000, it’s all of a sudden $10,000. Ouch!

Assuming you don’t want to pay those two points, your actual mortgage rate will probably be markedly higher, perhaps 6.75% instead.

And the bank or lender may inform you that you have to pay “points” to get that low, advertised interest rate on your mortgage.

Kind of Like a Car Lease Where You Pay for a Lower Monthly Payment

It reminds me of a car lease where you’re told payments are only $299 per month for 36 months, but it requires $2,500 cash at signing. Is it really just $299?

If you want to accurately gauge the deal, you need to consider that upfront cost. In the case of the car lease, it’s another $69 per month, or about $368 per month once factored in.

Your buddy might have scored the same monthly payment with nothing down, so it’s not really apples-to-apples.

The same goes for mortgages – how much are you paying to get the rate you want to brag about?

Anyway, back to our mortgage example, when looking at difference in payment, we’d be talking about savings of $150 per month if you opted for the lower 5.99% rate while paying two points.

Tip: Keep in mind that the discount points are paid in addition to any lender fees charged for origination, processing, underwriting, and so forth.

When You Break Even Determines If Points Are Worth It

- When paying points you need to consider the “break-even point”

- This is the date in which you recoup the upfront cost of the points

- How long it takes will depend on the rate reduction and price paid

- Be sure to consider how long you plan on staying in the home/mortgage while making the decision

While 5.99% certainly sounds a lot better than 6.75%, it’s actually only a $150 difference when you make your mortgage payment each month.

Not as awesome as it looked, eh. And guess what? You just paid $6,000 upfront, out-of-pocket for that $150 monthly discount.

And money spent today is more expensive than the same money spent in the future thanks to our friend inflation.

It’s also long gone the minute you spend it, trapped in your home at a time when money may be tight thanks to other closing costs and housing-related expenditures.

So why would someone want to drop several thousand bucks for a relatively small payment reduction? Well, assuming they stick with the mortgage long-term, the savings will come. It’ll just take a while…

The month at which you start saving money and essentially make those points worth the upfront cost is called your “break-even point.”

Factor in Tax Bracket and Savings Rates to Calculate Break-Even Point

- You need to consider your individual tax bracket to properly determine the break-even date for paying mortgage points

- This way you can figure out the actual savings assuming you itemize your taxes

- You also need to look at savings account yields or what your money would earn elsewhere

- Perhaps the $10,000 is better off in an investment account

The proper break-even point factors in your income tax bracket and current savings rates, not just the difference in monthly payment. It also accounts for faster principal repayment.

Remember, a lower interest rate means more of each payment goes toward whittling down the outstanding balance. This is another perk to paying points.

Of course, if you invest the money in stocks or bonds or whatever else, it could shift the break-even point tremendously.

If you want a good idea of when you’ll hit this magical point, look for a break-even calculator online that takes into account all those important details.

In our example, with a tax bracket of 24% and a current savings account yield of 4.75%, it would take roughly 34 months to break even. Or for paying mortgage points to be worth it (make sense financially).

Simply put, if you don’t plan on spending at least three years in your home, or more importantly, with the mortgage, it’s not worth paying the points.

However, if you’re the type who wants to pay as little interest as possible over the life of your loan because you’re in it for the long-haul, paying mortgage points can be a smart move.

In fact, if you see the mortgage out to its full term, you’d pay roughly $50,000 less in interest versus the higher rate mortgage. That’s where you “win.”

But before you get too excited, there’s another factor to consider. What it rates drop by a considerable amount after you take out your loan?

It Might Not Be a Good Idea to Pay Mortgage Points in 2025

- Mortgage rates are predicted to go down between now and the end of 2025

- The 30-year fixed is forecast to fall from around 7% to 6.5% or lower later this year

- If you pay points now you might leave money on the table if you refinance later

- It could make more sense to pay as little as possible at closing if you anticipate refinancing

Now might not be a great time to pay points seeing that rates are still close to their 21-century highs and will likely move lower throughout 2025.

Of course, we all thought mortgage rates would go down last year, and the year before that…and they didn’t.

Meaning a lot of homeowners who expected to refinance their mortgage didn’t. And those who didn’t pay points continue to be stuck with larger monthly payments.

But the latest 2025 mortgage rate predictions put the 30-year fixed about 0.5% to 1% lower by the end of the year.

So a rate and term refinance could be in the cards for those who take out a mortgage today.

Instead of paying mortgage points, a temporary buydown could be the better move. Any funds that aren’t used are typically just refunded if you refinance.

The only real drawback is if you’re unable to refinance for whatever reason. One worry is if home prices fall, you might not have the required equity to qualify.

Make Sure Paying Points Actually Lowers Your Mortgage Rate

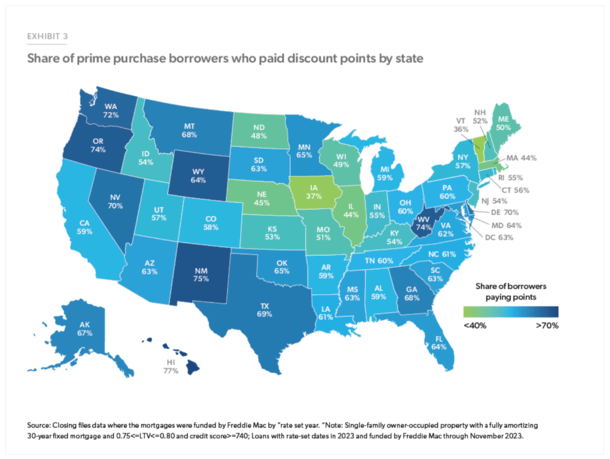

One final note. Freddie Mac just conducted a study focused on discount points because they’ve become a lot more common lately.

In fact, roughly 58.8% of purchase mortgage borrowers paid discount points in 2023, compared to just 31.3% in 2021.

The share was even higher for rate and term and cash-out refinance borrowers at 59.9% and 82.4%, respectively.

Most importantly, they discovered that “the interest rate differential between borrowers who pay discount points and those who do not pay discount points is very small.”

In other words, many home buyers are paying points but not getting a much lower rate.

They found that the average effective rate on home purchase loans for borrowers who paid discount points was 6.69% versus 6.86% for those who didn’t pay points. That’s a difference of just 0.17%.

To sum things up, the decision to pay mortgage points is a complex one that requires some thought. And some future planning. It’s also not a one-size-fits-all answer.

If mortgage rates are expected to fall, paying points is generally a bad idea. But if rates are low and not expected to get much better, or even rise, it can make a lot of sense.

Just be sure you actually secure a lower interest rate when paying points.

Those who don’t shop around could wind up with a higher rate compared to those who avoided paying points altogether.

In other words, shop both rates and points! It’s possible to get a good deal on both if you put in the time and effort.

Situations Where Paying Mortgage Points Can Be Worth the Cost

- While rates are low (less likely to refinance because it won’t get much better)

- If it’s your forever home (can be free and clear eventually for a lot less money)

- If you have a retirement goal to pay off the mortgage (as opposed to sell/refi it)

- On a property you occupy now but will rent out in the future (can lock-in a low rate now)

- If deducting points from taxes can save you money in a given year

Benefits of Buying Mortgage Points

- You get a lower interest rate

- Your monthly payment will be smaller

- You’ll pay less interest over time

- You’ll build equity faster

- Points are generally tax deductible

- You can brag to friends about your low rate

Disadvantages of Buying Mortgage Points

- You have to pay a large upfront cost for a lower interest rate

- The monthly savings may be negligible

- It could take a long time to break even

- You’ll lose money if you sell/refinance before breaking even

- You’ll have less cash on hand for other expenses

- Money may earn a better return elsewhere

- Smaller mortgage interest deduction

- Money loses value over time due to inflation

Read more: Are mortgage points tax deductible?

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026