The so-called “coronavirus checks” have begun to hit Americans’ bank accounts this week, providing relief to those whose income has been curtailed or completely cut.

It might be especially helpful to those who need to pay rent or make a monthly mortgage payment, the latter of which can be pushed back as late as the 15th of the month in most cases.

But just how far can the stimulus check go toward covering a rent or mortgage payment? Well, that totally depends on where you live.

Those with an adjusted gross income of up to $75,000 get the full $1,200 offered by the government.

It’s even higher ($2,400) for married couples making $150,000 or less, and potentially much higher for married couples or heads of household with young dependents.

Stimulus Checks Go Further on Rent than the Mortgage

- 77% of American renters could cover a month’s housing expenses with $1,200 check

- 47% of homeowners could pay their mortgage with the same check

- Share of homeowners who could make housing payment significantly higher in Indy (66%)

- Check would do very little to pay mortgage for most San Jose, CA homeowners (6%)

First off, 77% of renters could cover one month’s worth of housing expenses with a $1,200 check, versus just 47% of homeowners, per a new analysis by real estate brokerage Redfin.

The median monthly rent in the U.S. is $1,058 – it’s as low as $804 in Cleveland, Ohio, and as high as $2,283 in San Jose, California.

As such, about 93% of renters in Cleveland could cover the rent with their stimulus check and still have money left over, while just 22% of San Jose renters would be able to foot the entire bill.

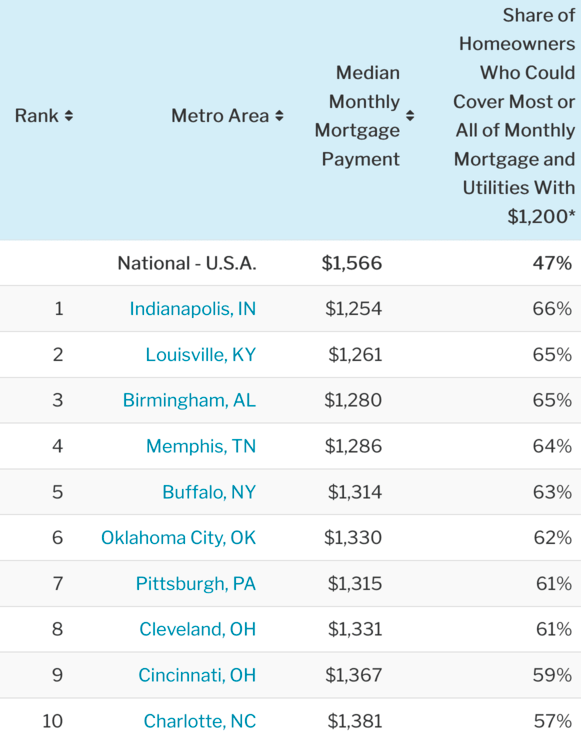

With regard to homeowners, the median monthly mortgage payment is $1,566 – it’s as low as $1,254 in Indianapolis, and as high as $3,371 in San Jose, CA.

That $1,200 would cover the mortgage plus basic utilities for 66% of Indy homeowners, but a mere six percent for San Jose homeowners.

Where the Stimulus Checks Go Far

As you can see, Indy homeowners can mostly cover their mortgages (and basic utility bills) with a $1,200 stimulus check.

The same goes for homeowners in Louisville, KY, Birmingham, AL, Memphis, TN, and Buffalo, NY.

Of course, a mortgage is just one of the many monthly expenses a homeowner must cover, and doesn’t account for things like grocery bills or unexpected home maintenance.

It’s also unclear what basic utilities are covered here – heating and water bills can get pretty expensive.

And what about property taxes and homeowners insurance? A true mortgage payment covers PITI.

Where the Stimulus Checks Barely Make a Dent

Then we have the opposite end of the spectrum, where $1,200 would do basically nothing for homeowners in the Bay Area, NYC, LA, San Diego, and Boston.

And that’s assuming these homeowners would actually receive a check, since it maxes out pretty quickly and folks in those expensive areas might make a lot more than the average American.

If they did get the $1,200, it’d cover most or all of the mortgage for anywhere from 6% to 14% of homeowners.

In other words, it wouldn’t go very far for many, and again, we have to factor in things like grocery bills, all utilities, and other debts like credit card bills and potentially student loans that aren’t on hold.

Ultimately, the stimulus checks aren’t going to provide total relief, though they might allow renters and homeowners to pay some bills or purchase essentials.

Should You Use Your Stimulus Check to Pay the Mortgage?

- For most the stimulus checks won’t cover a full mortgage payment

- Those in need of assistance might be better off requesting forbearance

- And setting aside the stimulus funds for the eventual payback of forbearance

- This illustrates why it’s important to have cash reserves when buying a home

When you take out a mortgage, you are typically required to document asset reserves. The idea is that you have some money set aside to cover mortgage payments should your income evaporate.

So a mortgage lender might ask that you have anywhere from two to 12 months of reserves as a cushion in case things go awry.

However, many home loans don’t require any reserves, which one could call risky. While that’s debatable, it’s times like these that support the argument that reserves are good.

Unfortunately, many Americans barely have enough funds to cover the down payment and closing costs, so asking for reserves on top of that can stop home purchases in their tracks.

Anyway, my tangent about reserves has a point. It might be wise to set aside any stimulus money as reserves, and opt for mortgage forbearance via the CARES Act if the check won’t cover the housing payment and you need financial assistance.

That way once the forbearance period ends, you’ll have some cash reserves to cover the shortfall from the forbearance.

This might be in the form of a repayment plan where you pay a little extra each month for a period of time to cover the missed amounts.

Read more: How is mortgage forbearance repaid?