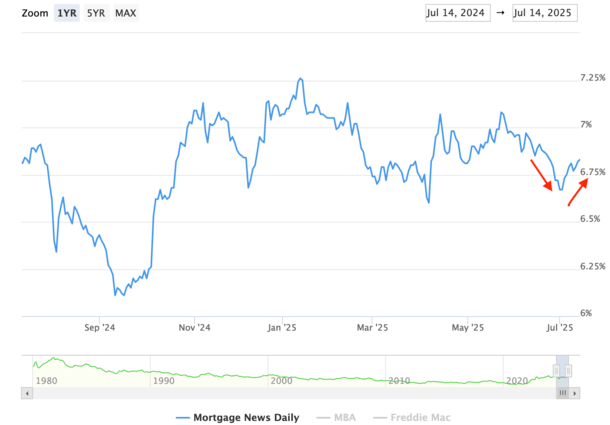

What a difference a month makes. Mortgage rates were close to eight month lows about two weeks ago.

Today? They’re only 17 basis points (0.17%) away from 7% again, which explains the ongoing shift to a buyer’s market.

It seems whenever we make some solid progress, it’s another step back to where we started.

The latest drivers of higher mortgage rates have been resilient jobs data and another round of tariff drama.

If this continues, it’s going to be difficult to see any sustained improvement any time soon.

Resilient Jobs Data and Tariff Drama Pushes Mortgage Rates Back Toward 7%

The 30-year fixed began the month of July at a relatively attractive 6.67%, before marching back up toward 7%.

At last glance, it stood at 6.83% after suffering another series of setbacks, the first being an unexpectedly hot jobs report.

That’s been the culprit for a while now, as labor has yet to really break, and the Fed has noted it’s labor they’re looking at most closely.

There have been scattered reports on the upside and downside, but we’ve yet to see consistently bad labor data.

Until that happens, it seems we’re kind of stuck at higher levels. Though before the June jobs report beat (147k vs. 110k), mortgage rates were beginning to show some real promise.

In fact, the 30-year fixed had fallen to 6.67%, per Mortgage News Daily, its lowest point of 2025 other than a blip in early April related to tariff drama.

Before that, you had to go all the way back to October 2024 to see lower mortgage rates.

And if you recall September 2024, when mortgage rates slipped very close to 6%, it was an entirely different housing market.

One full of promise and excitement that the high mortgage rates could finally be behind us. We also experienced a mini refi boom that had lenders feeling a bit more optimistic.

However, it was yet another head fake as hot jobs and now renewed tariff pressures push rates back up.

The latest being a 35% tariff on Canada, 30% on the EU and Mexico, and a tariff threat to Russia as well via “100% secondary tariffs targeting Russia’s remaining trade partners if a peace deal with Ukraine” isn’t reached within 50 days.

So if you thought the tariff stuff was over, welp, it’s not. And who knows what’s next.

Perhaps I spoke too soon when I said the tariff stuff was in the rear-view mirror.

CPI Report Tomorrow Could Shed Light on Tariff Impact

Speaking of the tariffs, tomorrow we get the ever-important CPI report, which will be the first time we get to see the impact of tariffs.

Though some have argued that “many companies stockpiled goods in advance of the tariffs,” meaning any price increases might not make their way into the data until that inventory is sold off.

And with new tariffs being threatened once again, some beginning August 1st, it continues to make it difficult to determine who exactly is/will pay for the tariffs.

Between the stockpiling and the fresh tariff threats, we might have to be even more patient than we already have been waiting for a possible uptick in inflation to no longer be a concern.

But the Fed has made it clear this is why they haven’t cut their own fed funds rate, which has increasingly frustrated the Trump administration.

So much so that FHFA Director Bill Pulte issued a statement about Powell supposedly considering an early resignation.

Those reports haven’t been substantiated to my knowledge, and will likely do nothing to deter Powell as he waits for more data to be collected.

This is kind of the irony of the current situation as the admin stokes inflation concerns while simultaneously asking for rate cuts.

You can’t have it all, but if you still want it all, at least provide some clarity on tariffs and don’t keep making new threats and raising the stakes.

Surely that’s no way to get bond traders to ramp up their purchases and bring yields down.

The good news is the 10-year bond yield seems to be back toward the top of its range (4.50%) at about 4.43%.

And the longer this goes on, the more mortgages we’ll originate with higher rates, which at some point will be ripe for a refinance.

Read on: Mortgage Rates Are Still Expected to Come Down by the End of 2025

(photo: Scouse Smurf)

- Big Weekend Ahead for Mortgage Rates - April 10, 2026

- Will Mortgage Rates Move Higher in May and June as They Do Historically? - April 9, 2026

- Mortgage Rates Drop on Ceasefire, But Beware of the Bounce - April 8, 2026