I sometimes forget your average homeowner doesn’t know it all when it comes to mortgages.

They’re complex and confusing and what might seem obvious to me isn’t to others.

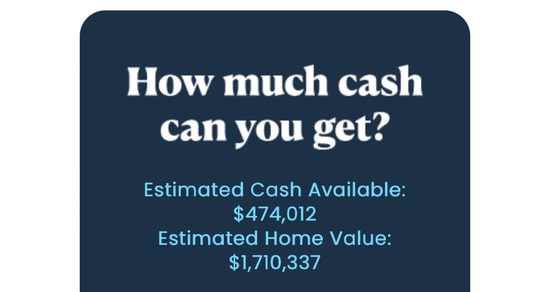

Latest case in point was an email my friend received from his loan servicer about tapping his equity.

It listed his estimated home value and estimated “cash available” if he were to take out a second mortgage, such as a home equity loan or HELOC.

He was confused because the numbers didn’t add up based on what he owed.

Lenders No Longer Let You Borrow 100% of Your Home’s Value

The confusion might lie in how lenders’ risk appetites have changed over the years.

Back in the early 2000s, it was very common for banks and lenders to let borrowers take out loans at 100% LTV/CLTV, meaning every last dollar was cashed out.

For example, if your home was appraised for $500,000 back when, a lender may have let you borrow the entire $500,000!

In retrospect, this clearly wasn’t a good idea for what seems like very obvious reasons today.

Zero skin in the game, high borrowing costs, little reason to stick around if the going gets tough and/or the property value suddenly declines.

And that’s exactly what happened. Making matters worse back then was the prevalence of adjustable-rate mortgages and even negative amortization loans and second mortgages up to 125%!

We all now know it was super bad lending that hopefully never gets repeated. That situation led to one of the biggest housing crashes in history.

It also led to new mortgage rules, including the ATR/QM rule, which puts a lot of guardrails in place to prevent another major crisis.

Without getting too convoluted here, let’s just say lenders are a lot more cautious today, thankfully.

What this means is you can no longer take out a mortgage for 100% of the property value. Lenders want a buffer.

Most Lenders Cap Home Equity to 80% or Less Nowadays

Because of the most recent mortgage crisis, banks and lenders remain a lot more conservative.

They want to ensure the loans they make aren’t too risky, and even if the borrower falls behind, they can recoup any losses.

The best way to accomplish this is to require a buffer between what the borrower owes and what the property is worth.

That way if they have to foreclose, there is hopefully some equity and the property won’t sell for less than what it’s worth.

It was common back then for borrowers to have negative equity, also known as an underwater mortgage, because of the high maximum LTVs/CLTVs and the rapid home price declines.

Today, you’re generally going to be capped at say 80% CLTV when taking out a second mortgage like a HELOC or home equity loan.

This ensures there’s at least 20% in equity if things go sideways. Or perhaps home prices drop!

So when my buddy was doing the math, he was confused because he only owes something like $800,000 and it said his home was worth $1,700,000.

In his mind, that meant he could tap something like $900,000, much more than the $474,000 mentioned.

If we do the math, this means his particular lender is capping the max cash out at 75% CLTV.

Roughly $1,275,000 divided by $1,710,000 is just under 75%. So in this case, a 25% equity buffer.

That’s smart for the lender because it gives them a solid cushion. It’s also good for the health of the housing market if home prices fall and/or borrowers fall behind on payments.

It helps us all avoid another scenario where homeowners get in over their heads and completely sap their equity, which would make a traditional sale very difficult.

Read on: How to compare HELOCs from different lenders.

- Is It Too Soon to Talk About 4% Mortgage Rates Again? - February 26, 2026

- Nation’s Top Mortgage Lender Funded $163 Billion in 2025, a 17% Annual Increase Driven By Refinances - February 25, 2026

- Bed Bath & Beyond Will Soon Offer Mortgages - February 24, 2026