A “1031 exchange,” also known as a real estate exchange or a tax-deferred exchange, was created by the IRS in 1990.

Simply put, the exchange occurs when the proceeds from one sale are used in the subsequent purchase. It is named after IRS Code section 1031.

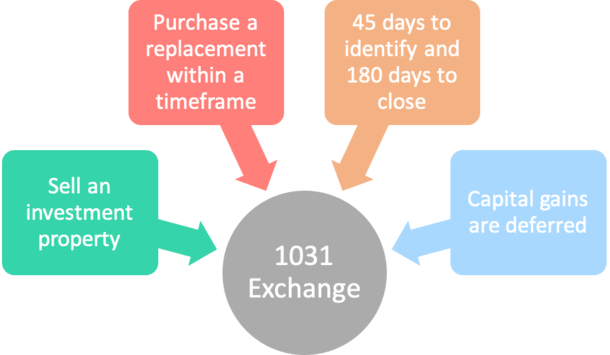

In terms of real estate and/or mortgage, when a homeowner sells one investment property to buy another, like property, they can offset or even fully defer capital gains tax.

The main idea here is you shouldn’t have to pay capital gains if your intention is to immediately turn around and buy a similar property with the proceeds.

How a 1031 Exchange Works

- If you plan to buy another investment property shortly after selling one

- It may be possible to defer any capital gains taxes from the sale

- Replacement property must be identified within 45 days and purchased 180 days from prior sale

- Process must be overseen by a qualified intermediary

In a 1031 exchange, the property sold is referred to as the “relinquished property” and the property acquired is called the “replacement property”.

Prior to the introduction of the 1031 exchange, a homeowner had to simultaneously sell one property while purchasing the new property, a practice which proved to be very difficult.

The IRS finally proposed a solution with the introduction of the 1031 exchange, which effectively allowed a homeowner to sell their relinquished property and use the proceeds to buy the replacement property later.

However, for the exchange to work, it must be overseen by a qualified intermediary and certain rules must be followed.

What type of property qualifies for a 1031 exchange?

- Two types of property qualify for a 1031 exchange

- Including property held for business use

- Such as a rental property

- And land held for investment

Real estate is divided into four classifications, including property held for business use, land held for investment, property held for personal use, and property held primarily for sale.

The first two categories qualify for a 1031 exchange, while the last two do not.

To completely offset capital gains, all proceeds from the relinquished property sale must be invested in the replacement property.

The properties exchanged must be of like-kind, meaning that they are of the same classification, not based on their condition or quality.

However, this category is broad, and can mean selling a farm to buy a house. Or selling a condo and buying a mini-mall.

Time Requirements of a 1031 Exchange

- There are strict timelines for a 1031 exchange to work

- Including an identification period of 45 days

- In which you must identify a replacement property after selling your old one

- And an exchange period of 180 days

- Which spans from the date you sell your old property until you must close on the replacement property

There are also certain time requirements that must be strictly followed.

The identification period of the 1031 exchange begins the date the relinquished property is transferred (or deed recorded) and expires after 45 days.

In other words, you must identify a replacement property within 45 days of selling your old (relinquished) property and do so in writing to either the seller or the intermediary.

The exchange period begins on the date you transfer the relinquished property and ends after 180 days or earlier if tax returns for the taxable year in which the transfer occurred are submitted before those 180 days.

This means you get 180 days from the date of the sale of your old (relinquished) property to close on the replacement property.

Additionally, there must be an actual exchange overseen by a qualified intermediary, and not just a transfer of property for money only.

Knowing the rules is a good first step, but it’s always wise to seek the services of a professional early on to avoid any costly mistakes when executing a 1031 exchange.

Reverse 1031 Exchange

There is also such a thing as a “reverse 1031 exchange,” which as the name implies, allows you to purchase a replacement property before selling the relinquished property.

If effectively works like a 1031 exchange in reverse – go figure – with similar rules regarding timing and the use of an intermediary.

Once the new property is purchased, you get 45 days to identify a property to sell. And you get a total of 180 days to actually complete that sale.

This might come in handy if you come across a great investment property and realize it’s also a good time to unload a different property, all while deferring your capital gains.

Here are those 1031 exchange rules again in a condensed format:

- the property exchanged must be of like-kind (pretty broad, e.g. exchange a commercial building for a rental condo or single-family rental home)

- the property must conduct business (e.g. investment property)

- property should be of equal or greater value

- the exchange must occur in the allotted time frames

- must use a qualified intermediary or facilitator

- it’s possible to exchange one property for multiple cheaper properties

- you can also do things the opposite way via a reverse 1031 exchange

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026

The 1031 exchange seems daunting, but I am interested in pursuing it. The essential question is financing, as with all real estate. When one investment is sold to be replaced by a similar investment (though different location), the income from the original property is lost. It seems that getting approved for a loan for the replacement property would be difficult as only the personal income of the buyer and the net proceeds from the relinquished property is all that can be counted toward the new purchase. Since it is not enough to assume the new property will bring in income, or enough to meet the required loan, what would a lender require of a borrower in these circumstances?

Jane,

A borrower would likely seek out a tenant to move into the investment property at closing and use that income to help qualify, and/or get a comparable rent schedule to project rents for the property.

Looking for 1031 exchange administrator. Sale of CA property and purchase of a MT property. Sale revenues-$365,000, purchase costs-$265,000 + $40,000 improvements. What will my costs be to the administrator?

I owner financed a property I sold a few years ago. The buyers are getting ready to pay the mortgage off. Can I do a like kind exchange for another mortgage?