Here comes the mortgage assistance! I honestly thought I wouldn’t be writing about this sort of stuff anytime soon, but here we are. It feels like 2009 all over again.

As previously blogged about, all the major housing agencies have pledged to help homeowners affected by the coronavirus, including Fannie Mae, Freddie Mac, HUD, USDA, and the VA.

Now individual banks and mortgage lenders are stepping up to the plate to put a hold on mortgage payments. Good on them.

Bank of America Offers Mortgage Deferment for Those Affected by Coronavirus

- Bank of America will defer mortgage payments for an unknown period of time

- Company is doing so on a case-by-case basis, may need to prove hardship

- Deferred payments will be added to the end of the loan

- Unclear if interest will be charged during deferment period

First up, Bank of America is offering deferment on basically all loans and credit cards, including mortgages and home equity loans/lines.

The caveat is that the mortgage or home equity loan/line must be held on the bank’s books.

So if you make mortgage payments to Bank of America each month, as opposed to some other loan servicer, you might be eligible for assistance directly from them.

Additionally, you need to make the request, they aren’t just freezing mortgage payments for all customers in advance.

This appears to be on a case-by-case situation as well, which they said is how they’ve approached things in the past during other natural disasters or the semi-recent government shutdown.

In terms of how the mortgage deferment will work, the bank said deferred payments will be added to the end of the loan.

So it doesn’t appear as if you’ll have to pay back the deferred amount once payments resume, either via a lump-sum payment or by increasing subsequent monthly payments until the missed amount is repaid.

Instead, you’ll wind up with a longer loan term or perhaps a balloon payment. One gotcha here is that the bank may continue to charge interest during the deferral period.

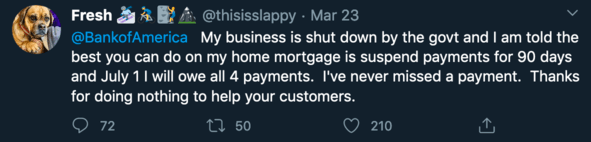

Unfortunately, there are already individual accounts of the payment deferment not working like that at all, and actually being due in full once the three months are up.

Or at least having to pay some portion of the missed payments once the deferment ends, something most in need of assistance probably can’t muster.

Apparently, it’s possible to get a loan mod after the three months are up, at which point the missed payments would be added to the end of the loan, but it’s case-by-case.

In other words, the mortgage relief isn’t as good as it looks.

However, there won’t be any negative credit bureau reporting for clients currently up-to-date on their payments.

Bank of America is also pausing foreclosure sales, evictions, and repossessions.

Ally Home Coronavirus Mortgage Relief

- Ally Home is offering deferred mortgage payments for up to four months

- Interest will accrue will payments are deferred

- Unclear how the deferred amount and interest are to be paid back

- Ally Home Loans Customer Care can be reached at 1-866-401-4742

Then we have Ally Home, which has offered to defer payments for up to 120 days for existing mortgage customers.

While no late fees will be charged, interest will accrue. It’s unclear if the missed payments will be tacked on to the end of the loan, or repaid differently once the forbearance comes to an end.

Again, you are going to have to reach out to them instead of expecting a sweeping motion for all mortgage customers.

Be sure to get all the details of the deferment to ensure it makes sense for your situation, including credit score impact, how it’s paid back, and so on.

Also note that you may need to provide documentation to prove you’ve been adversely affected by the coronavirus.

Quicken Loans Coronavirus Relief

Quicken Loans has also announced a relief effort for those “worried about making” mortgage payments.

Initially, the company is offering the relief option of a forbearance, which they call “a temporary stoppage of your mortgage payments.”

Though there aren’t details in terms of whether you’ll pay interest while payments are suspended, or late fees, etc., you can get the process started on their website.

Quicken notes that those with a conventional loan (non-government loan such as a Fannie/Freddie-backed one) won’t experience any credit score impact due to the forbearance.

It’s unclear what their approach is for government loans, such as FHA loans and VA loans.

Freedom Mortgage Suspends Foreclosures and Evictions

Freedom Mortgage announced Monday that it had suspended residential property foreclosures and evictions for the loans it services.

Additionally, the company said it “has taken additional measures to assist customers, communities and employees grappling with the impact of COVID-19.”

While it’s not clear what that assistance is, Freedom says it “encourages its customers who are facing hardships to call the company toll-free.”

You can reach their customer service department at 855-690-5900.

Just note that they are apparently handling “unusually high call volume,” so patience is needed.

Chase, Citi and Wells Fargo Mortgage Relief Options

- All three have mentioned that mortgage assistance is available

- But some haven’t rolled out plans specific to the coronavirus outbreak yet

- The Chase mortgage assistance phone number is 1-800-848-9380

- The Wells Fargo phone number for mortgage payment issues is 1-800-219-9739

Citi has a notice on its website telling customers there are “a range of hardship programs through our service provider, Cenlar FSB.”

You can contact Cenlar at 1-800-2CENLAR (1-800-223-6527) Monday to Friday from 8:30am – 8pm ET and Saturday from 8:30am – 5pm ET.

This doesn’t appear to be unique to the coronavirus outbreak, but rather their ongoing hardship assistance program.

Wells Fargo mortgage customers are being offering a “90-day payment suspension.”

To request this type of assistance, simply sign on to online banking and email them through the secure Message Center.

They say they’ll respond to you within 3 to 5 days. You can also contact Wells by phone at 1-800-219-9739.

Chase has finally offered specific coronavirus mortgage relief, but it’s only a 90-day payment forbearance, and interest will accrue during that time.

While they won’t report the payments as late, the missed amount is due in full at the end of the forbearance period, which likely won’t work out for most homeowners who lack funds.

The bank also has a webpage dedicated to mortgage forbearance.

If you need mortgage help, you can call Chase at 1-800-848-9380 with questions or sign in and send them a secure message.

My assumption is they will offer better options than the generic ones listed on their websites, given the current situation is not anyone’s fault. And it’s also extraordinary.

In summary, be sure to understand the terms of any mortgage assistance, the impact on your credit (if applicable), how and when you’re expected to pay back any deferred amount, and so on.

While it might be tempting to get a mortgage break, there could be financial consequences.

Tip: If you are active duty military, or perhaps even National Guard, you may be eligible for additional benefits.

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026