Mortgage rates finally caught a break last week after steadily rising throughout much of 2023.

The 30-year fixed fell about a half a percentage point in the matter of a week as softer economic data eased inflation concerns.

At the same time, the Fed left its key policy rate unchanged and signaled it could be done raising rates.

Now, investors are hoping the next policy move is a rate cut, as data is expected to continue to cool into 2024.

Taken together, that could mean a return to more palatable mortgage rates in 2024.

Lower Mortgage Rates Before the Presidential Election?

The president and CEO of the nation’s top mortgage lender, United Wholesale Mortgage (UWM), is bullish on mortgage rates next year.

During his monthly 3Points video, former college basketball player Mat Ishbia said he expects mortgage rates to drop before the election.

The election in question is the 2024 Presidential Election, which takes place on Tuesday November 5th, 2024.

“And I think it might even happen sooner like March, April, May,” he said in the video.

But how much lower will rates fall? Well, that’s another story, as a return to 3% mortgage rates likely isn’t in the cards.

Same goes for 4% rates, and maybe even 5% rates. However, that doesn’t mean smaller improvements can’t be impactful for the struggling mortgage industry.

“We’re talking about dropping to 5 and a half, 6, even 6 and a half,” he added. “And it’ll be a massive refi opportunity.”

It’s possible we’ll see a return of rate and term refinances if mortgage rates drop enough relative to the rates obtained by home buyers over the past year and change.

Assuming some of these borrowers took out high-7 or even 8% mortgage rates, there might be a case to be made if rates return to the low 6%s or high 5%s.

Generally, you want at least a 1% reduction in mortgage rate, though there isn’t a hard and fast refinance rule of thumb.

Lower Mortgage Rates Will Also Unlock Existing Housing Inventory

Ishbia also noted that beyond the refinance opportunity, there will be more inventory next year as interest rates fall.

“But beyond that, even more purchases, more inventory will open up.”

This speaks to the mortgage rate lock-in effect that has stifled the existing home market.

In short, homeowners with 3% mortgage rates have their hands tied, as moving to a new home at current prices with a 7 or 8% rate just doesn’t pencil.

But if rates come down to more reasonable levels, some of these homeowners will be financially able to sell and move, or will simply be OK with taking on a higher payment.

Rates aside, he believes home purchase lending volume will increase, referencing a recent Fannie Mae forecast.

Fannie expects 2024 home purchase loan origination volume to increase 10% to $1.44 trillion.

Meanwhile, they believe mortgage refinance volume will rebound to $456 billion, nearly double the dismal $250 billion anticipated for this year.

The refinance share is also expected to rise from around 16% this year to 24% next year.

There Is No Mortgage Rate Rescue Plan Coming…

Lastly, he dispelled the idea that some sort of mortgage rate rescue plan was going to materialize.

“That’s not going to happen.” We think the market is what the market is and that we’re going to see things happen as we’ve expected.”

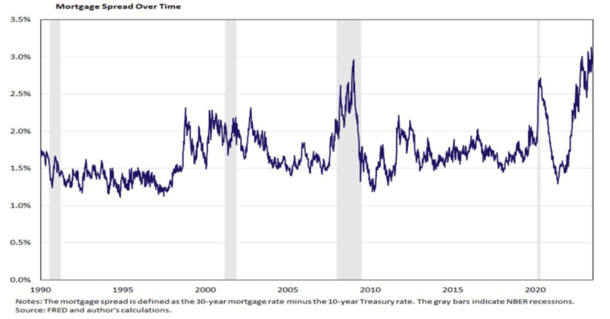

About a month ago, industry groups including NAR and the Community Home Lenders of America lobbied Treasury Secretary Janet Yellen and Fed Chairman Jerome Powell.

They pointed out that mortgage rate spreads relative to the 10-year treasury yield had doubled in recent months.

Typically about 170 basis points, they have exceeded 300 bps for a while now, putting even more pressure on mortgage rates.

In a letter, the groups proposed a plan to allow Fannie Mae and Freddie Mac, on a temporary basis, to purchase their own mortgage-backed securities (MBS).

And/or purchase Ginnie Mae MBS (those backing FHA and VA loans) for a defined period of time.

Additionally, they called on the Federal Reserve to maintain its stable of MBS and suspend runoff until spreads normalized.

It seemed to fall flat as it would completely contradict recent action by the Fed to tackle inflation, which arguably was caused by an overly accommodative rate environment.

In a nutshell, the ultra-low mortgage rates were how we got into this mess to begin with, so lowering them again may actually do more harm than good.

Sure, there’s a happy medium in between 8% mortgage rates an 3% mortgage rates, and the hope is we’ll get back there in the next year or two.

But if rates come down too quickly, or fall too low, you’ve got the bidding wars again, unhealthy demand, and so on. That’s not good for anybody long-term.

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026