Now that Zillow has gone all-in on mortgages, soon you might not be able to compare rates from third-party lenders on their website.

This would be unfortunate as their so-called Zillow Mortgage Marketplace is a great tool to see rates from a bunch of local lenders all at once.

It allows Zillow visitors to quickly get a sense for current mortgage rates and gain exposure to options they might not otherwise see.

Now that Zillow Home Loans is making a big push to originate its own loans, this marketplace has become harder to find (but it still exists!).

For me, it speaks to a bigger trend in the industry, where there’s less and less room for the smaller independent lender or mortgage broker.

Less Consumer Choice When It Comes to Mortgage Rates

I understand that Zillow wants its visitors to go straight to its in-house mortgage lender if they need a home loan (why wouldn’t they?).

Back in 2019, Zillow Home Loans was officially launched after they acquired Mortgage Lenders of America in the fourth quarter of 2018.

Originally, the move was intended to streamline mortgage financing for its now shuttered Zillow Offers platform, which was an iBuying program that struggled to take off.

Despite that setback, Zillow has made an even bigger foray into mortgages in recent years, going on a loan officer hiring spree to grow its business.

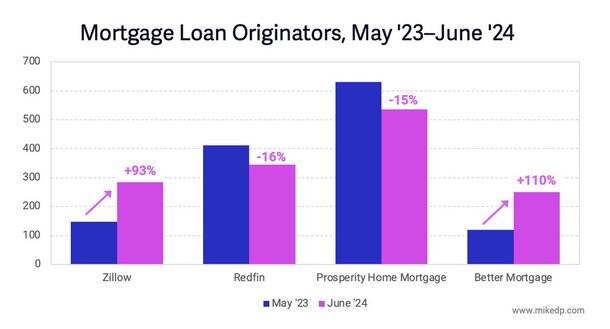

Per industry consultant Mike DelPrete, the company nearly doubled its mortgage loan originator count between May 2023 and June 2024, at a time when other lenders were shedding staff.

Despite a poor lending environment driven by high mortgage rates, the company kept hiring.

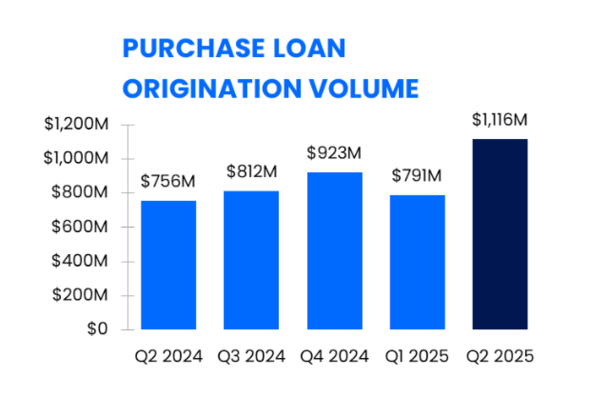

And it finally paid off, with home purchase volume exceeding $1.1 billion in the second quarter of 2025, a near-50% year-over-year increase (see chart below).

This has made it abundantly clear that they’re serious about becoming a major mortgage player, even though they’re still kind of small.

It’s also becoming clear that they may no longer have room in their business model for third-party mortgage lenders.

Many smaller mortgage companies and local mortgage brokers rely upon Zillow for leads.

Now they may have to go elsewhere, though these alternatives seem to be quickly drying up.

What this means is the consumer will ultimately be left with fewer choices and more home loans will wind up with the big guys.

Studies have proven that consumer choice is good for mortgages (and likely everything else), but we’re seeing more and more consolidation and that’s bad for prospective home buyers.

Mortgages Are Going Vertical

Lately, we’ve seen a big push for real estate and mortgage companies to go vertical.

That is, control more of the entire process from start to finish, whether it’s real estate agent selection, loan origination, or loan servicing, once the mortgage funds.

We’ve seen it with Zillow via this home loan push, and also with their rival Redfin, which got acquired by Rocket Mortgage.

Redfin also used to have a mortgage comparison tool, despite the launch of Redfin Mortgage years ago.

Now those who visit the Redfin website or use the Redfin app will be pitched a home loan by Rocket Mortgage.

And once they have a loan, their in-house loan servicer will likely reach out to offer them a mortgage refinance or home equity loan.

It’s becoming tougher and tougher for a third-party lender to break through, and with less choice, expect higher rates/costs.

As I always say, when a lender reaches out, reach out to other lenders. Take the time to compare quotes beyond just one lender.

This is especially important now as we see more consolidation in the industry, and because mortgages are more or less a commodity.

They don’t really differ that much from one company to another, so securing a lower rate with fewer closing costs is key.

In fact, the only real difference might be the loan process. Once the loan funds, it’ll likely operate exactly like any other 30-year fixed mortgage (the most popular loan choice).

Read on: The Gap Between Good and Bad Mortgage Rates Has Grown Wider, Shop Accordingly

(photo: k)

- Beeline’s Self-Service Mortgage Option One Step Closer to Loan Officer Extinction - March 13, 2026

- Mortgage Rates Just Flipped From Trending Down to Trending Up - March 12, 2026

- Mortgage Rates Just Hit Fresh 2026 Highs - March 11, 2026