While there has been some debate about the so-called mortgage rate lock-in effect, it appears to be a pretty legit force in the housing market today.

As the logic goes, existing homeowners aren’t moving because their mortgage rates are so low.

But it’s not only that they’re so low, it’s also the cost of replacement, with prevailing market rates now edging closer to 8%.

So it just doesn’t make a lot of financial sense for homeowners to move unless they absolutely have to.

And for many, it’s probably not even doable, thanks to a massive increase in costs if exchanging a 3% rate for a near-8% rate.

Is Mortgage Rate Lock-In a Real Thing?

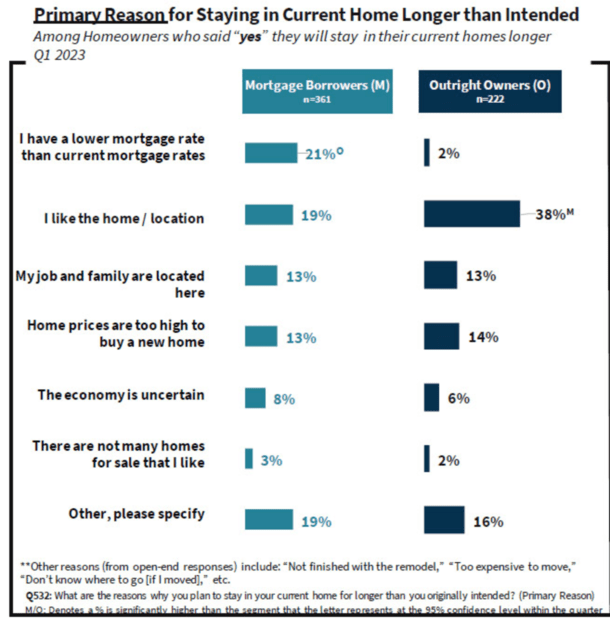

A new survey from Fannie Mae explored mortgage rate lock-in and found that while it is certainly a reason for staying put, it’s not the only reason.

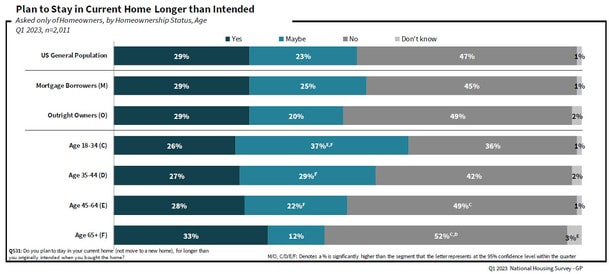

The company asked homeowners via their National Housing Survey if they planned to stay in their current homes longer than originally intended. And if so, why.

They found that an equal 29% share of owners with a mortgage (mortgage borrowers) and outright owners (homeowners without a mortgage) planned to stay put longer.

Of the mortgage borrower population, 21% indicated the decision was primarily due to having a low mortgage rate.

But Fannie points out that this subset of homeowners only represents 6% of all mortgage borrowers.

“These survey results lead us to conclude that there are multiple factors contributing to the historically low supply of existing homes for sale.”

“While the lock-in effect is real for many consumers, the full range of reasons provided by mortgage borrowers and outright owners for planning to stay in their homes longer paints a significantly more nuanced picture.”

There Are Many Reasons Why Housing Tenure Has Increased, But a Low Mortgage Rate Still Tops the List

The Fannie Mae researchers argued that even if mortgage rates were to decline by a meaningful amount in the intermediate term, they would not expect to see a big surge in for-sale listings.

They believe there are a “confluence of factors and trends contributing to the lack of housing inventory in the United States,” with the mortgage rate lock-in effect one of several.

Still, it did top the list for those with a mortgage. As you can see in the chart above, 21% of homeowners with a mortgage cited their lower mortgage rate as the primary reason for staying in their current home longer than intended.

That was the number one response, though it was trailed fairly closely by a homeowner simply liking their home/location.

Of course, one could argue that it’s easier to like your home if you’ve got an ultra-low mortgage rate attached to it.

And let’s not forget that these folks also likely got in when home prices were significantly cheaper.

When the 30-year fixed mortgage hit a record low back in 2021, home prices were also a lot lower. In some areas, home values may be up nearly 50% over that time.

So these homeowners have very cheap housing payments relative to what’s on offer today, between their smaller loan amount and significantly lower mortgage rate.

If you don’t believe mortgage rate plays a role, simply look at homeowners without a mortgage.

These free and clear borrowers are focused on other things, like the location, proximity to job and family.

Mortgage Rate Disparity Affects Everyone, Even Cash Buyers

But that doesn’t mean they don’t care about mortgage rates because it’s also makes a move for them more difficult.

Assuming they can’t pay for a home with cash, they too would have to face the higher mortgage rates currently on offer.

So for them, it may also be “too expensive to move,” factoring in a higher asking price and steep mortgage rate.

One could also blame the lack of for-sale inventory on the disparity between mortgage rates then versus now.

Fewer for-sale listings mean it’s harder to find a replacement property. This too could contribute to homeowners determining that they like their existing properties more.

They could be resigned to the fact that moving is out of question, and/or put more work into making their existing digs better.

At the end of the day, you could argue that this speaks more to the general lack of affordability in today’s housing market than anything else.

And until we see more supply hit the market, it’s not going to change, even if mortgage rates do come back down to more reasonable levels.

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026