It’s been a while since my last mortgage match-up, so let’s give it a whirl again: “Mortgage vs. cash.”

Today, the focus will be on taking out a mortgage versus simply using cash when purchasing a home and skipping the lender piece altogether.

Of course, it’s not that simple for the majority of the population to throw a few hundred thousand dollars (or more) down on a property. So for many, this won’t even be an option.

But it’s worth visiting regardless to see how even the very rich often opt for a home loan when they’ve got plenty of cash to spare.

Buying a Home with Cash Has Its Benefits

- Cash buyers are more attractive to home sellers

- The home buying process can be a lot faster without a mortgage

- Don’t need to abide by any mortgage lender’s rules

- No property restrictions or inspections to worry about

- Don’t have to pay interest to the bank for several decades

First let’s talk about buying a home with cash. This is almost certainly the favored approach of real estate investors and perhaps the mega-rich, though billionaires like Mark Zuckerberg still take out mortgages.

And investing gurus like Warren Buffett think the low mortgage rates are a great deal…especially when you get to lock in a low fixed rate for 30 years.

But for a large swath of the population, this either/or question doesn’t even get any consideration because most of us can’t afford to buy a home (or even a small condo) with cash.

Heck, many Americans can’t even afford to buy a property with a mortgage.

Anyway, there are some advantages to buying a home with cash as opposed to taking out a mortgage.

The most obvious is that you don’t pay any interest when you buy with cash. That’s right, no mortgage, no costly interest payments.

Additionally, you don’t have to make any payments to principal each month either, seeing that you own your home free and clear right off the bat.

However, that doesn’t mean you won’t have recurring costs. You’ll still need to pay homeowner’s insurance (unless you’re really brave), along with property taxes and possibly HOA dues depending upon where the property is located.

The insurance thing becomes optional when you own your property outright. Not so if you have a mortgage because you don’t really own your home. Your lender does, until that loan is actually paid off in full.

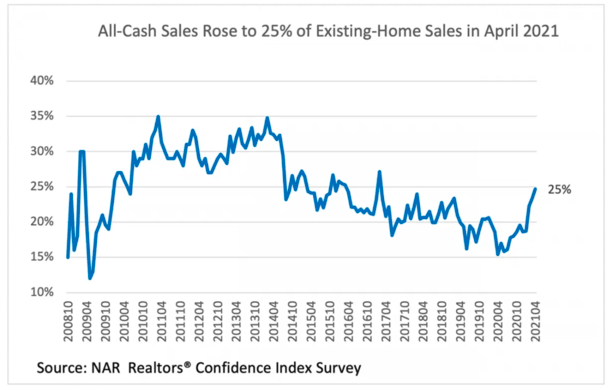

Cash Buyers Have Negotiating Power in Competitive Markets

Another plus to paying with cash is the negotiating power you gain when making an offer, especially in a competitive housing market.

As seen in the chart above, all-cash sales have spiked recently as the housing market has heated up.

Simply put, the more competition there is, the more all-cash home sales, which become a necessity to those who must win the property.

If you’re going up against some other would-be buyers that need to finance the purchase with a home loan, you’ll have the upper hand in pretty much every situation when paying cash.

Sure, you could get outbid by another buyer willing to offer more for the home, but your cash offer should be king if all else is equal.

And it may still be king even if you offer less than the competition because the sellers will like the assurance tied to an all-cash offer, especially if the appraisal becomes stretched.

Once your offer gets accepted, you won’t have to worry about dealing with a bank or mortgage lender, or an appraisal at value.

That means it doesn’t matter if your credit score is in bad shape, or if you don’t have the necessary income to qualify for a mortgage.

Or if you’re self-employed or a foreign national who might otherwise have difficulty getting a loan.

There is still a process to purchasing the home, but you can cut out the middleman, otherwise known as the lender.

And that means you won’t have to pay lender fees, including a costly loan origination fee, or lender’s title insurance, processing and underwriting fees, and so on.

But you might not want to skimp on the inspection or home appraisal, even though it’s not a requirement.

It’ll also buy you some time to determine if the house is in good shape and worth what you agreed to pay.

That lack of a mortgage also means you’ll be able to move in sooner, or rent out the property sooner.

Speaking of renting it out, you won’t have to worry about occupancy issues, or a higher mortgage rate because it’s an investment property, which is another big plus.

Taking Out a Mortgage, Even If You Don’t Have To

- A lot of very rich people take out mortgage loans strategically

- Not because they have to, but because they know home loans are cheap money

- Instead of tying up all their hard-earned money in a single property that is essentially illiquid

- They put their excess cash to work in other investments that can yield better returns

On the other hand, there’s the traditional approach to buying a home, with the help of a mortgage loan.

This is kind of the default option more out of necessity than preference. As I alluded to earlier, most of us can’t afford to buy real estate with cash. We need a mortgage to get the deal done.

In fact, many Americans need a sizable mortgage to get the job done, with practically zero-down FHA loans a popular choice for a large number of prospective home buyers.

So like it or not, a mortgage is often just a fact of life.

The number one downside to a mortgage is all that interest paid throughout the life of the loan.

For example, a 30-year mortgage with a $200,000 loan amount set at 4.5% will result in about $165,000 in interest over the loan term.

Yeah, you pay nearly double what you agreed to pay for the home. Sounds pretty rough, doesn’t it?

But like I said, this is the price of not having a substantial amount of money to put down.

Along with all that interest, you also have to pay a bunch of lender fees, which can certainly add up.

And if you put down a very small amount, you’ll also be subject to paying mortgage insurance premiums, possibly for life if you go with an FHA loan and never take the time to refinance.

Oh, and you don’t just get a mortgage. You need to qualify for a mortgage, and not everyone qualifies for countless reasons.

Having the lender pry into your personal and financial life may also be extremely annoying and frustrating, but if you need to borrow hundreds of thousands of dollars, they’ve earned that right.

You Get to Write Off the Interest and Mortgage Rates are Super Low!

- Those who itemize can write off their mortgage interest and get a tax break

- Mortgage rates are super low at the moment, making home loans an attractive financing vehicle

- You can also lock in a low interest rate for 30 years and watch your payments get cheaper thanks to inflation

- And it shouldn’t be too difficult to earn a better return for your money in the stock market or elsewhere

The good news is that you can write off all that mortgage interest as long as you itemize deductions and they exceed the standard deduction.

So even though mortgage payments are stuffed to the gills with interest, paying it can result in a lower tax bill each April, which lessens the blow pretty significantly.

Additionally, mortgage rates are dirt cheap compared to just about every other type of loan out there, and can be locked in for a full three decades.

Yes, you pay a lot of interest over that period of time, but it’s only because the loan amounts are so large.

A home loan with a 3% mortgage rate that is fixed sure sounds better than a credit card’s APR at 20% or higher, which is often variable to boot.

What this means is there’s a decent chance you can invest the money that would otherwise be locked up in your home (if you paid cash) at a better return elsewhere.

It’s not too difficult to beat a 3% annual return in the market or elsewhere, which explains why the ultra-rich elect to take out mortgages.

Having a mortgage on your home also means you’ve got more liquidity and less at risk, assuming something goes wrong or the housing market tanks.

Imagine something devastating happens to your home that isn’t covered by insurance. Would you rather have 20% invested, or 100%?

Also consider the housing bust that took place a decade ago – a lot of homeowners were able to walk away from their homes relatively unscathed because they didn’t have much invested.

Those who purchased all-cash could maybe cut their losses, but they couldn’t walk away without losing a lot of money.

There’s also that old saying about putting all your eggs in one basket.

If you don’t have money in other places, it certainly shouldn’t all be tied up in your home.

[Mortgage affordability calculator]

Can You Get the Best of Both Worlds with a Mortgage/Cash Hybrid Approach?

- Most home buyers put down a small amount of cash and take out a mortgage

- The sweet spot might be a 20% down payment

- This allows you to avoid costly mortgage insurance and obtain a low mortgage rate

- You can invest your excess funds elsewhere or prepay the mortgage if that’s your goal

Absolutely. Most people buy homes with cash and a mortgage, not just either or.

In other words, when you put 20% down on a house, you’re still paying a decent chunk of cash and financing the rest.

As a result, you avoid the requirement for mortgage insurance, you get a lower rate of interest, and you have an equity investment.

Putting down 20% or more should also put you in a pretty good position when it comes to a bidding war, though an all-cash buyer willing to make a good offer will always have the upper hand.

Additionally, you can always pay your mortgage off earlier than planned seeing that most mortgages don’t have prepayment penalties anymore.

Sure, you will subject yourself to the closing costs associated with a mortgage, along with the qualifying process, but you don’t have to pay off your mortgage over 30 years.

If you decide your money isn’t earning as much as you’d like, you can move more of it towards the mortgage balance anytime you wish.

Got plans to retire in 10 or 15 years? Start prepaying the mortgage faster so you’ll be free and clear by the time you’re on a fixed income. Or go with a 15-year fixed mortgage instead.

Remember, it doesn’t have to be an either/or discussion. You can make adjustments based on your financial standing as time goes on.

If you decide to go all-cash, you can also pull equity via a cash out refinance. So both options provide flexibility.

Advantages to Buying a Home with Cash

- No need to qualify for a mortgage

- No need to shop for a mortgage

- No mortgage payments (good if you lose your job or are close to retirement)

- No interest due

- No lender fees

- Homeowner’s insurance isn’t required

- You don’t need to pay for an appraisal

- More negotiating power when making an offer

- Lower purchase price possible

- Faster closing process

- Could be a better return for your money than a low-yielding CD or bond

- Set it and forget it investing (don’t have to manage your investments)

- Can tap home equity if and when needed

- Can always sell or take out a mortgage

- Less hassle overall (one less thing to manage)

- Sense of security because it’s your home!

Disadvantages to Buying a Home with Cash

- Most of us don’t have the money required to buy a home with cash

- Mortgage rates are a cheap source of financing

- Real estate is an illiquid asset (not easy or free to sell)

- The property could lose substantial value

- You could lose a lot of money if your home is destroyed and not covered by insurance

- You miss out on the mortgage interest deduction

- Your return on investment might be poor relative to other options

- Poor diversification if a lot of your money is in one single property

- House rich and cash poor if savings get depleted

Advantages to Buying a Home with a Mortgage

- Mortgage rates are very low

- Mortgage interest is tax deductible

- Inflation should make future monthly payments “cheaper”

- You only need to bring in a small down payment

- More cash on hand for anything else

- Getting a mortgage isn’t really that difficult

- A mortgage can actually improve your credit score

- You can prepay your mortgage whenever you want in most cases

- You can invest your money elsewhere for a better return

- Your money is more liquid

- Forced savings each month

- Less risk if something happens to your home or if values drop

Disadvantages to Buying a Home with a Mortgage

- Tons of mortgage interest must be paid

- 30 years of monthly payments (maybe less, but still a long time!)

- You need to shop for a mortgage

- You need to get approved for a mortgage

- You could get declined

- More (lender) costs associated with a mortgage

- Closing process more work and more time

- You may buy more house than you should (get in over your head)

- Harder to sell the property if little or no equity

- You can lose your home if you fall behind on payments

- You don’t actually own your home

Read on: What is the downside to taking out a mortgage?

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026