The latest monthly national housing survey from Fannie Mae revealed an interesting contradiction.

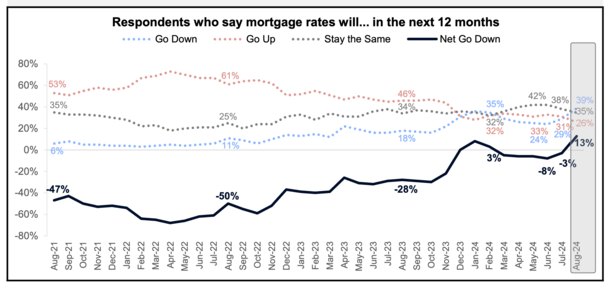

Last month, a new survey-high 39% of respondents said they expect mortgage rates to go down over the next 12 months.

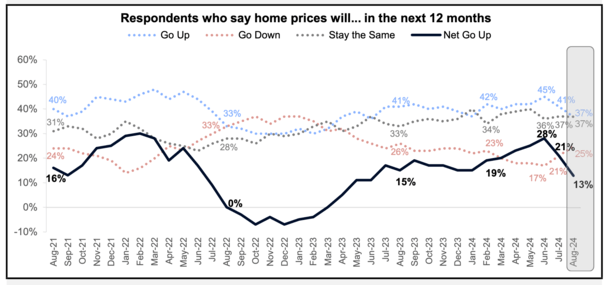

At the same time, fewer expect home prices to go up over the same period. And more believe home prices will fall.

So despite a home purchase becoming more affordable thanks to a lower interest rate, consumers don’t think prices will increase.

What does this say about home buyer demand as mortgage rates go down?

But We Were Told Bidding Wars Would Return When Mortgage Rates Fell

Fannie’s monthly Home Purchase Sentiment Index (HPSI) did increase very slightly (0.6 points) to 72.1 in August from a month earlier.

But it remains very low, with most of the 1,000 respondents saying it’s a poor time to buy and also an increasingly bad time to sell.

Just 17% said it was a “good time” to buy a home in August, which has remained relatively flat for several months and remains just above all-time survey lows.

Meanwhile, 83% said it was a “bad time” to buy a home, the highest share since the survey’s inception.

At the same time, only 65% say it’s a good time to sell, while 34% say it’s a bad time. Since August 2021, the “net good time” to sell has fallen from 54% to just 31%.

So it appears no one is happy with the current state of the housing market, which continues to be characterized by a mismatch between buyers and sellers.

Sellers are being told they aren’t realistic in terms of what they’re asking, and buyers are saying it’s too expensive. But nobody is budging.

There’s also a lack of inventory in most markets, so there’s little to choose from and often not what a prospective buyer is looking for.

Taken together, we’ve seen a big drop in home sales, especially once you factor in the ongoing mortgage rate lock-in effect.

It’s also odd to see this sentiment given the narrative we’ve heard for some time that the housing market would turn into a frenzy when mortgage rates fell.

Well, they’ve fallen from around 8% a year ago to just above 6% at last glance. You’d think that would be enough to get the ball rolling.

It’s the Economy (and Maybe High Home Prices Too!)

As I wrote last week, it’s no longer a mortgage rate story. Most consumers are on board the “rates are going lower” bandwagon.

Yet they’re also saying it’s not an ideal time to buy. So then you need to look elsewhere for your answer.

Are home prices just too high, even with mortgage rates nearly 2% below their peak a year ago?

Or is the economy becoming more of a concern, with the Fed dancing with a recession and lots of rate cuts now expected over the next year and change?

Most of the consumers surveyed by Fannie Mae said they weren’t concerned about a job loss (78%), which has drifted down from 82% in 2021 but remains high.

But respondents have been more pessimistic about their household income compared to a year ago, with more saying it’s “significantly lower” than “significantly higher.”

This could also reflect the purchasing power of their dollars, which have eroded thanks to the inflation of just about everything.

So you start to wonder if consumer outlook is worsening as the economy shows signs of slowing, all while unemployment is rising.

This is what matters more than rates. And really explains why mortgage rates and home prices don’t have an inverse relationship.

If mortgage rates are expected to fall due to slowing economic conditions, couldn’t you argue that home price growth might also?

I’ve argued that home prices and rates can fall in tandem for this reason, despite nominal declines being rare.

But it at least bucks the idea of a home buyer frenzy when rates fall. Of course, rates have fallen during the slower time of the year. And they’re still markedly higher than they were as recently as early 2022.

So perhaps we just need rates to continue falling and for the 2025 spring home buying season to come about.

Then we’ll have a better idea of where this housing market goes next.