Today we’ll check out “Own Up,” a new technology company that wants to be your mortgage co-pilot.

By that, they mean help you comparison shop for a home loan without having to jump through hoops or get badgered by salespeople. And stick with you every step of the way.

Aside from making the process faster and easier, they can apparently save you some serious dough too – to the tune of $27,102 in interest over the life of the loan (on average).

How Own Up Works

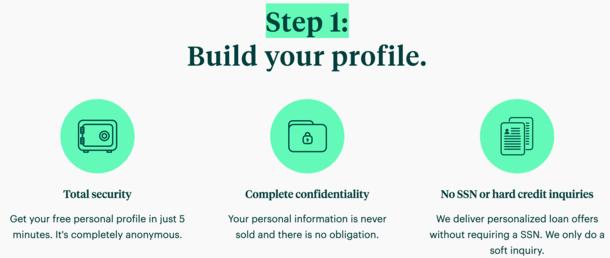

- Complete an online profile on the Own Up website in about five minutes

- Schedule a call with a dedicated home advisor to discuss your mortgage goals

- Compare rates and fees from partner lenders on their platform and select the one you like best

- Fill out the lender’s application and they’ll process, underwrite, and fund your loan

Instead of going to a bank or calling a lender to get a mortgage, you begin by creating a profile on the Own Up website.

While they refer to themselves as a tech company, they’re technically a mortgage broker, just on a larger scale, as opposed to a mom and pop shop.

They seem to be similar to Credible, the Fox-owned brokerage that operates a comparable mortgage marketplace for homeowners.

What this means for you is that Own Up acts as an intermediary between borrowers and mortgage lenders.

After you complete your anonymous online profile, you’ll be assigned a dedicated home advisor who will discuss your needs/goals, along with what to expect during the loan process.

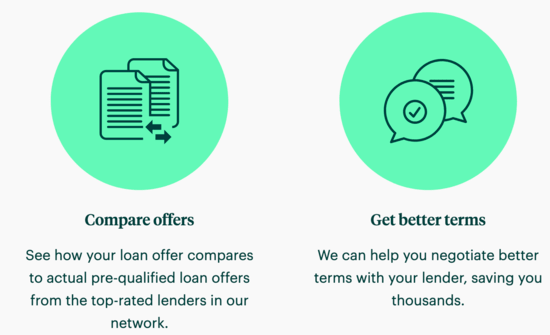

You’ll then be able to compare lenders on the Own Up network and see loan offers (mortgage rates) from partner lenders in real-time.

They’re able to deliver personalized offers without requiring your social, and they only perform a soft credit check so your scores aren’t affected.

If you like what you see, simply fill out the corresponding lender’s digital mortgage application to formally apply.

The lender you select will then process, underwrite, and close the loan in typical fashion, with your Own Up home advisor standing by if and when you need them.

Why Use Own Up to Get a Mortgage?

As to why you would employ two companies instead of one to obtain your home loan, the answer appears to be savings.

Whether you’re buying a home or refinancing an existing mortgage, their customers save an average of $27,000 over the life of their loan.

They say they’re able to save customers money by charging much less than what the typical salesperson earns per loan.

Own Up charges participating lenders a flat 0.40% (40 basis points) of the loan amount, which is only due after the loan closes. They do not charge customers anything directly.

This compares to the industry average of 1.15% that the company says is typically charged by banks and lenders.

And because Own Up is able to streamline the origination process and effectively lower costs for its partners, they claim many of their lenders reduce their rates for their customers.

In other words, it might be possible to get your mortgage from the same exact company but obtain a lower mortgage rate via Own Up.

They negotiate terms with their lender network so you don’t have to, and because all lenders pay the same exact fee every time, they show you every offer exactly as they see it.

What Types of Loans Does Own Up Offer?

Because they act like a mortgage broker, they’re able to offer just about any type of home loan that their partner lenders originate.

This means you can get a home purchase loan or a refinance loan, along with a fixed-rate mortgage or an ARM.

You can get financing on a single-family home, condo, townhouse, or multi-unit investment property.

Similarly, you can choose from a variety of down payment options, including no- and low-down payment loan programs like FHA loans, VA loans, and so on.

They also claim to offer the industry’s first automated pre-approval letter, which allows you to generate updates on-demand from any device like your smartphone.

So if you’re shopping for a home, you can update any necessary information on the fly in minutes and present the listing agent with a tailored approval to strengthen your offer.

Which Lenders Does Own Up Work With?

As to who Own Up partners with, they say they handpick mortgage companies that are “reputable and financially secure.”

To ensure that, lenders must undergo what they refer to as a “rigorous screening process,” while agreeing to Own Up’s service level standards.

Additionally, they share all customer feedback and reviews with their lenders to improve performance going forward.

Since they offer a turnkey digital solution for lenders, their partners might include companies that aren’t as technically savvy, yet still want an online presence to target Millennial and Gen Z home buyers and homeowners.

This means you might get additional lender options that you may otherwise wouldn’t have considered.

That’s a good thing because more lender choice means the potential for a lower interest rate and/or reduced closing costs.

At the moment, Own Up is only available in a select number of states, including Colorado, Connecticut, Florida, Georgia, Maine, Massachusetts, Michigan, New Hampshire, Pennsylvania, Rhode Island, Tennessee, and Texas.

Should You Use Own Up?

The company’s goal is to save you time and money, and make it easier to get a home loan. Those are admirable goals and if they can accomplish them, they could be worth using.

But it should be noted that Own Up does not actually take formal mortgage applications, make credit decisions, or originate loans.

Rather, the information you submit to them acts as an inquiry to be matched with a lender that does the aforementioned things.

This isn’t necessarily a good or bad thing, but you should know what you’re getting.

Assuming you do find a lender using their service, you’ll need to complete a formal application and go through the typical home loan process. That’s pretty much unavoidable.

The good news is that their service, at a minimum, seems to allow you to comparison shop without much heavy lifting, similar to how a mortgage broker works.

The difference is that you can shop anonymously with Own Up and simply decide not to use any of their partners if you don’t like what you see.

Aside from the built-in comparison shopping, you also get a loan guide who can provide unbiased guidance and feedback without the usual sales pitch.

Additionally, even if you already have a loan offer or two, they say they’re able to negotiate better terms with your lender. I’m not sure how they do that, but it sounds pretty good.

In summary, Own Up might be a good choice for someone looking for multiple mortgage quotes who doesn’t want to put in all the work or get bombarded with emails and phone calls.