There’s been a lot of fear lately that mortgage rates could rise back above 7% or even higher this year.

The driver being inflation related to $100+ oil, which increases the cost of just about everything.

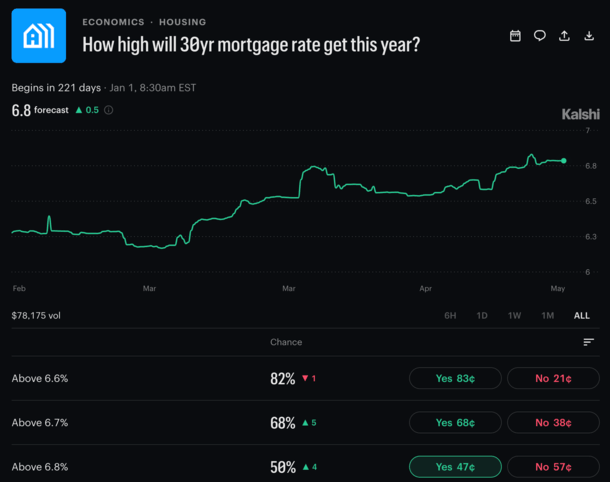

But the so-called “odds” are still pretty split with only a 50% chance they rise above 6.8%, this according to Kashi, which offers and tracks prediction markets.

This doesn’t mean they’re right, but it shows you where pricing is resolving at the moment.

So perhaps there’s limited upside (in a bad way!) for the 30-year fixed, despite all that’s going on.

Will the 30-Year Fixed Rise Above 6.80% Again This Year?

At last glance, Kalshi’s “How high will 30yr mortgage rate get this year” market is at an even 50-50 chance for rising above 6.8%.

This is at any point over the next six months and change that are left in the year 2026.

That’s not much conviction given everyone has been screaming that mortgage rates could surge higher with inflation.

It uses Freddie Mac’s weekly Primary Mortgage Market Survey (PMMS) as the source.

As of last week, the 30-year fixed averaged 6.51%, per the PMMS, so it would have to move about 30 basis points higher to get above that 6.8%.

Kalshi currently sells a “yes” contract for this market for $0.47 each. So $100 worth at $0.47 would buy you 213 contracts.

The way it works is if you were to stake $100 on the 30-year fixed going above 6.8%, and it hits, you would earn $113 in profit.

In other words, those contracts become worth a dollar each if the 30-year fixed goes above 6.8%.

I’m not saying to do it, nor am I doing it, but I thought it was an interesting way of looking at probabilities based on public perception.

The 30-Year Fixed Was Above 6.8% in 16 of 52 Weeks Last Year

I actually looked back on mortgage rates in 2025 based on Freddie Mac data and found that there were 16 weeks where the 30-year fixed was above 6.8% last year.

That’s more than a quarter of the time, nearly a third in fact, when conditions were arguably relatively similar.

And mind you, we didn’t have the Iranian conflict and oil prices above $100, with renewed fears of inflation.

That’s not to say mortgage rates go back there, but it also wouldn’t shock me.

I’ve been saying for a while that rates could briefly touch 7% or even rise above 7% this year.

Of course, it depends on how Freddie Mac captures data.

Their weekly survey is often delayed because they collect mortgage rate quotes throughout the week (prior Thursday through Wednesday) and post them on Thursday.

This means they often don’t capture all the rate movement, especially if it’s brief.

For example, you could get a day or two when rates spike, but then they ease again and Freddie Mac never really captures it. Or it’s diluted by lower days.

Conversely, you’d see that rate movement on a daily mortgage index such as Mortgage News Daily’s.

In terms of when the 30-year fixed was last above 6.8%, it was the week of June 18th, 2025.

The big difference this year versus last though is that mortgage rate spreads have improved tremendously.

This means you need the 10-year bond yield to go even higher this year, all else equal.

It’s certainly still a real possibility, but it will be driven by what transpires in Iran.

If a peace deal or similar resolution is reached anytime soon, we might never get about 6.8%.

If the conflict drags on or worsens, something above 6.8% or even 7% is entirely conceivable.

The kind of good news here is that mortgage rates might have a bit of a ceiling at current levels, so the worst could mostly be behind us.

- Despite Headwinds, Odds of a 7% 30-Year Fixed in 2026 Are Super Low - July 9, 2026

- Just When You Thought 7% Mortgage Rates Were Off the Table - July 8, 2026

- Light Week for Economic Data Means Flat Mortgage Rates Likely - July 6, 2026