It’s been an uphill battle to sell a home lately, with interest rates through the roof and home prices equally expensive.

But somehow, someway, the home builders have been increasing sales and unloading inventory as affordability continues to hamper existing home sales.

Part of it has to do with mortgage rate lock-in, with existing homeowners less likely to sell and give up their low fixed rate, but that’s just one side of the story.

The builders are also really good at offering incentives to move their product, even if it’s not the “best time to buy.”

They’ve been referred to as efficient sellers compared to the owners of existing homes, who have struggled to woo buyers the past few years. But why?

The Home Builders Are Offering Customers Lower Mortgage Rates

One of the big differentiators lately has boiled down to mortgage rates. After interest rates quickly climbed from their record lows in the 2s all the way to 8%, existing home sales fell off a cliff.

And they haven’t recovered much either since sliding to their lowest point since 1995 last year.

Meanwhile, newly-built home sales are chugging along at a solid clip, in spite of still-elevated mortgage rates.

Sure, mortgage rates have come down a bit from their cycle-highs seen in October 2023, but they’re still way up there.

At last glance, the 30-year fixed was hovering close to 7%, a far cry from the sub-3% rates on offer as recently as early 2022.

Despite this, the home builders are selling homes, snagging a near-15% market share in 2024 when it’s normally only about 10%.

So how are they doing it? Well, one of the best tools in their arsenal has been mortgage rate buydowns.

Instead of simply telling a home buyer they have to suck it up and buy a home with a 7% rate, they’ll offer a special, bought-down rate.

For example, it’s not uncommon to see a builder offer a mortgage rate beginning with a 4 today.

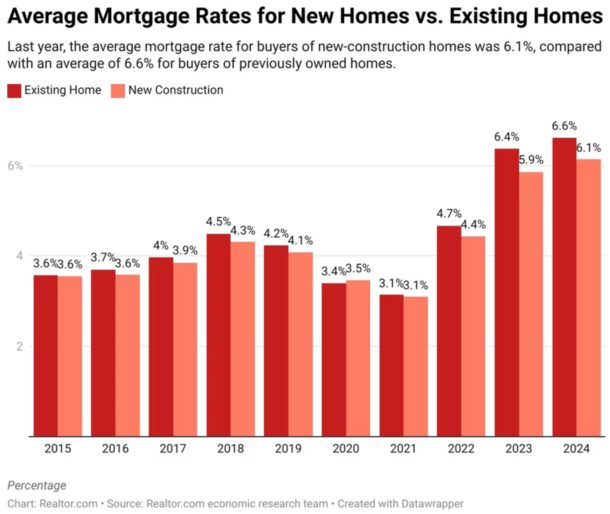

And if you look at the chart above from Realtor, you’ll see that since mortgage rates surged higher, the difference in average mortgage rate for existing home buyers versus new construction home buyers has widened.

It used to be nearly identical, whether buying a used home or a new home, but now it’s clearly lower for new homes.

Home Builders Are Controlling the Financing Piece to Boost Affordability

As you can see, new construction home buyers are winding up with mortgage rates about a half-point lower on average relative to existing home buyers.

Much of this has to do with the fact that home builders often have their own in-house mortgage lender.

Some examples include DHI Mortgage and Lennar Mortgage, two of the biggest home builders in the country with equally big lending units.

Aside from the expected efficiencies of having a one-stop shop, they can also pitch special mortgage rates to their customers.

This includes both temporary mortgage rate buydowns and permanent ones, with many builders offering both to get customers in the door.

For example, you might see a special rate of 2.99% in year one, 3.99% in year two, and 4.99% for the remainder of the 30-year loan term.

Meanwhile, someone buying an existing home might face an interest rate in the high-6s, which at minimum is unattractive. And at worst, makes them ineligible for a mortgage.

So aside from existing home inventory being lower due to lock-in, the sellers of existing homes aren’t doing as great of a job unloading their properties.

If they took out a page from the builder’s playbook, they too could accomplish the same thing.

After all, a 1% drop in mortgage rate is equal to roughly an 11% drop in home price. And the home builders know this.

If You’re a Home Seller, Consider Offering a Credit for a Mortgage Rate Buydown Instead of a Price Reduction

| $500,000 Purchase Price | $20k Price Cut | Permanent Buydown |

| Mortgage Rate | 6.875% | 6% |

| Cost to Seller | $20,000 | ~$10,000 |

| Loan Amount | $384,000 | $400,000 |

| Monthly P&I | $2,522.61 | $2,398.20 |

Those who are struggling to sell their home today might want to consider a rate buydown instead of a price reduction.

Redfin recently noted that nearly half of home sellers were offering seller concessions to buyers, which is just below a record high.

And some of them are offering credits for things like a mortgage rate buydown. This can be a smarter approach than dropping the listing price, as you get more mileage via a lower rate.

As noted, lowering the purchase price often doesn’t move the dial much in terms of monthly payment.

Here’s a quick example. Imagine selling a home for $480,000 versus $500,000. But the mortgage rate is 6.875% instead of 6%.

The monthly payment is actually lower on the $500,000 purchase. It’s $2,398.20 instead of $2,522.61, despite a larger loan amount of $400,000 vs. $384,000.

A good real estate agent can negotiate with the buyer’s agent and their client to illustrate this and offer a credit toward that rate buydown.

Similar to a new-construction home, an existing home can come with a reduced mortgage rate to push the sale through. And both the buyer and seller walk away happy.

- Are Mortgage Rates Approaching a Top? - March 27, 2026

- Better and Coinbase Launch Token-Backed Mortgages - March 26, 2026

- Mortgage Rates Will Soon Be Above Year-Ago Levels - March 25, 2026