The nation’s largest home builder, D.R. Horton, also has its own affiliated mortgage lender known as “DHI Mortgage.”

Recently, new home sales have surged in popularity due to the mortgage rate lock-in effect.

Essentially, existing homeowners aren’t selling their properties because they’ve got ultra-low fixed interest rates on their home loans.

At the same time, mortgage rates have surged higher, resulting in big financing incentives from home builders to move their newly-built home inventory.

Let’s take a hard look at what DHI Mortgage has to offer and whether an in-house lender is the way to go.

DHI Mortgage Offers Purchase Loans and Refis

- Full service mortgage lender offering home purchase loans and refis

- Founded in 1997, headquartered in Austin, Texas

- Parent company D.R. Horton is the nation’s largest home builder

- Publicly traded company (NYSE: DHI)

- Also operate DHI Title and D.R. Horton Home Insurance Agency

- Aim to be a one-stop shop for newly-built home buyers

- Funded roughly $24 billion in home loans during 2024 (latest data available)

- Most active in the states of Texas, Florida, and California

- Licensed to do business in 34 states

DHI Mortgage is a full-service mortgage lender owned by parent company D.R. Horton.

They were founded in 1997 and are headquartered in Austin, Texas.

D.R. Horton is the largest home builder in the United States, slightly bigger than competitor Lennar, which also has a captive mortgage company called Lennar Mortgage.

The home builder got its start back in 1978 when Don R. Horton built his first home in Fort Worth, Texas.

Since then, the company has grown into a near-$40 billion dollar company that is publicly-traded on the New York Stock Exchange (NYSE: DHI).

The company’s shares are owned by legendary investor Warren Buffett, who sees strength in home building given the lack of existing home supply.

Aside from operating their in-house mortgage lender DHI Mortgage, they also run an affiliated title company and insurance agency.

This means home shoppers can use DHI Title for their title insurance needs and D.R. Horton Home Insurance Agency for their homeowners insurance, assuming it’s competitively priced.

The goal is to create a one-stop shopping experience for home buyers and streamline what is often a daunting process.

Last year, they funded about $24 billion in home loans, with about 25% of overall volume coming their home state of Texas, per HMDA data.

They are also quite active in Florida, California, Arizona, Georgia, Nevada, and The Carolinas.

Somewhat amazingly, they were also the seventh largest mortgage lender overall in 2024, which is impressive for a builder’s captive lender.

In late 2025, DHI invested in Tidalwave, which bills itself as a mortgage-technology startup that uses autonomous AI agents to streamline the loan underwriting process.

Most D.R. Horton Home Buying Customers Use DHI Mortgage

Home builders with their own financing divisions tend to capture a lot of the business.

After all, why would a customer go get a mortgage elsewhere if they can do it all under one roof?

Especially if the builder offers an unbeatable interest rate thanks to a massive rate buydown.

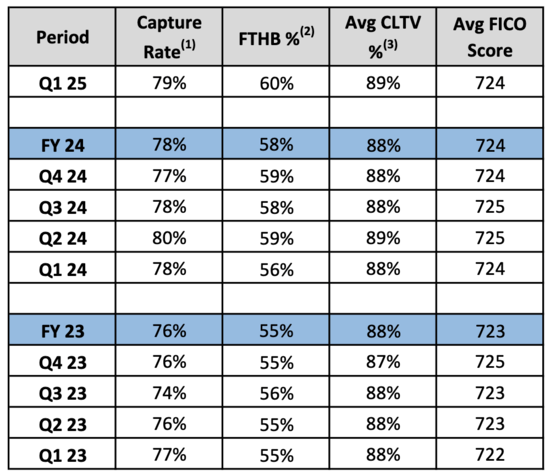

Well, it turns out most don’t go elsewhere, and do use the home builder’s lender. And I have the data to back it up from D.R. Horton’s most recent financial release.

As you can see in the table above, their capture rate was 78% in 2024, meaning roughly eight out of 10 home buyers use them for mortgage financing.

This the percentage of total home closings by D.R. Horton for which DHI Mortgage handled the home buyers mortgage financing.

Given the fact that there are all-cash buyers out there, this might mean that something like only one of 10 don’t use DHI Mortgage.

So if you’re buying a D.R. Horton property, chances are you’ll use this company, and you’ll certainly be solicited to do so. But as always, put in the time to compare lenders!

How to Apply with DHI Mortgage

While you can get pre-qualified for a mortgage online via the DHI Mortgage website, they say to get in touch with your mortgage loan originator to submit a full loan application.

It’s unclear if this means you can still apply electronically after speaking with a loan officer, or if you have to apply in-person.

They do have branch locations and sales offices at their home builder developments, which could facilitate this process.

Unfortunately, their website is a bit limited when it comes to information, so you’ll probably need to speak with a human before proceeding to an application.

Their online system, powered by fintech company Blend, does seem to allow for online refinance applications along with the pre-qualifications.

If you visit their website, it’s also possible to search for a local loan originator by state, branch, or by name.

They say they have digital options for buyers, but don’t make clear what those are. My assumption is they do offer some sort of online loan submission process.

And likely the ability to complete tasks electronically, whether it’s satisfying loan conditions or checking loan status.

However, I would like to see more information in this department.

Loan Programs Offered by DHI Mortgage

- Home purchase loans

- Refinance loans

- Conventional loans including Fannie/Freddie 3% down

- FHA loans

- VA loans

- USDA loans

- Fixed-rate and adjustable-rate options

- Temporary buydowns

- Affordable housing loans

DHI Mortgage offers the most popular loan options out there, whether it’s 3% down conforming loan backed by Fannie Mae or Freddie Mac or an FHA loan.

You can get both a home purchase loan or a mortgage refinance, though I doubt many existing homeowners would use them for a refinance unless mortgage rates were ultra-competitive.

The full menu of government-backed mortgages is offered, including FHA loans, VA loans, and USDA loans.

And both fixed-rate and adjustable-rate options are available, including the 30-year fixed, 15-year fixed, 7-year ARM, and 5-year ARM.

They also appear to offer jumbo loans that exceed the conforming loan limit in pricier regions of the country.

However, they don’t appear to offer any second mortgages, such as HELOCs or home equity loans.

But temporary buydowns, such as 2-1 buydown, are offered, as well as other affordable housing loans if buying in specific locations or with low-to-moderate income.

DHI Mortgage Rates

Speaking of mortgage rates, DHI Mortgage doesn’t have a page on their website dedicated to rates or lender fees for that matter. Meaning daily rates aren’t posted anywhere.

So you’ll be a little bit in the dark there. Be sure to ask your loan originator what fees they charge, such as loan origination fees, application fees, processing and underwriting, etc.

The good news is I did see special interest rate offers on the D.R. Horton website, which is typical of the home builders.

They often offer special incentives to their home buyers who also use their affiliated lender.

If you want to check out D.R. Horton mortgage rates, first visit the D.R. Horton website, then search for your desired home community.

From there, you’ll be able to see which homes qualify for or offer a “Special Interest Rate.”

I came across a 4.99% fixed rate FHA loan offer, which was also available on VA and USDA loans.

And a 5.50% fixed rate conventional loan offer that only required a five percent down payment. Those are about 1% below market.

So chances are they can offer some pretty competitive rates if you buy a D.R. Horton property and use DHI Mortgage.

DHI Mortgage Home Buyers Club

Those with imperfect credit can take advantage of the “DHI Mortgage Home Buyers Club.”

It pairs in-house credit consultants with prospective home buyers to prepare them for homeownership.

While it doesn’t guarantee loan approval or improved credit scores, they will work with you to boost your overall credit profile.

They’ll also ask you to complete a HUD-approved homebuyer education course while your credit consultant comes up with a credit profile improvement strategy.

This might entail removing inaccurate items on your credit report, paying down high balances, and getting current on any past due accounts.

The goal is to clean up your credit history and improve chances of mortgage approval, and potentially snag a lower mortgage rate depending on credit score improvement.

DHI Mortgage Reviews

As always, I try to track down customer reviews online to see what past customers think of the lender in question.

And they don’t appear to be great, based on what I could find. Their headquarters in Austin has a 2.6/5 rating from about 40 Google reviews.

Over at WalletHub, it’s a similar 2.6/5 rating from just over 30 reviews, with some customers citing poor communication and delays.

You can also find reviews for individual loan officers if you go on Zillow and search by name or location.

DHI Mortgage currently has a ‘B+’ rating with the Better Business Bureau (BBB), which isn’t fantastic and likely due to customer complaints.

They also have a 1.14/5 rating on the BBB website based on customer reviews.

To sum things up, their website could do with improving and their mixed reviews raise some questions about customer service.

On the bright side, they offer a good amount of loan programs and might have financing specials that beat out the competition.

Ultimately, it would probably come down to price if deciding between them and a different lender.

Though I assume most DHI Mortgage customers are also likely D.R. Horton home buyers, so there will likely be a big push to stay in-house.

Just be sure to speak with other mortgage companies, independent mortgage brokers, and so on to weigh your options.

Convenience is great, but not at the price of higher closing costs and/or interest rates. So definitely shop around.

Lastly, note that DHI Mortgage sells most of the loans it originates, meaning it’s likely your loan will be sold and transferred to a new loan servicer shortly after closing.

Read more: Should I use my home builder’s preferred lender?

DHI Mortgage Pros and Cons

The Good

- Special financing incentives to D.R. Horton home buyers

- Might be a quicker/easier home buying process using affiliated companies

- Branch locations allow borrowers to work with in-person if preferred

- DHI Mortgage Home Buyers Club helps credit challenged buyers

- Free mortgage calculator and homebuyer education resources online

- Lots of loan programs to choose from including fixed-rate loans and ARMs

The Perhaps Not

- Only licensed in 34 states

- No mention of mortgage rates or lender fees online

- Clunky website with limited information

- Don’t seem to able to apply for a home loan electronically

- Do not offer second mortgages or home equity products

- Do not service the majority of their loans

- B+ BBB rating and poor customer reviews

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026

- Chase Is Advertising Mortgage Rates With Nearly Two Discount Points to Keep Them Looking Attractive - August 4, 2026