This morning, the Job Openings and Labor Turnover Survey (JOLTS report) was released by the Labor Department.

It revealed that the labor market wasn’t running as hot as it was previously, leading to a nice drop in the 10-year treasury bond yield.

As a result, long-term mortgage rates, which track bonds like the 10-year, should also see some much needed relief.

But why does seemingly bad economic news benefit consumer mortgage rates?

Well, when you’re trying to fight inflation, which hurts bonds, any sign of a slowing economy is generally good news.

JOLTS Report Reveals Cooler Labor Market Conditions

As noted, this morning’s JOLTS report came in cooler than expected, prompting a sizable drop in treasury yields.

With inflation and unemployment taking centerstage of late, reports like this have become a lot more important.

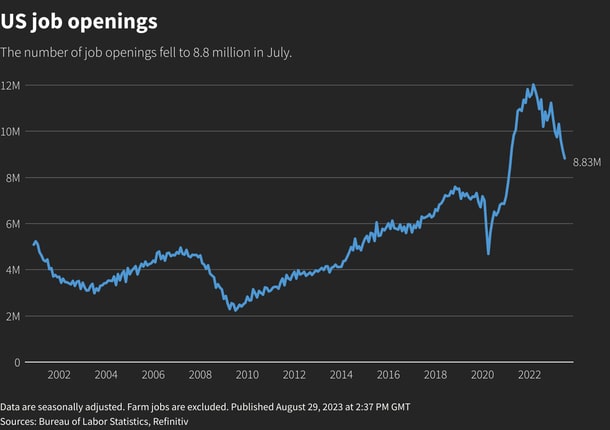

Specifically, job openings dropped 338,000 to a total of 8.827 million as of the last day of July.

This is the lowest level of openings since March 2021, and well below the forecast of 9.465 million job openings, per economists polled by Reuters.

The report is essentially a barometer of labor demand, with fewer openings indicating less need from employers.

At the same time, fewer openings mean it’s more difficult to find work, which could lead to higher unemployment.

Meanwhile, the so-called quits rate fell to 2.3% from 2.4% a month earlier, with totals quits decreasing 253,000 to 3.5 million, the lowest level since February 2021.

The quits are a proxy for labor market confidence, with fewer quitters indicating less hope of finding a replacement job. In other words, sticking with what you’ve got, even if the pay isn’t great.

Together with quits, layoffs and discharges make up what is known as “separations,” which were little changed at about 1.6 million.

Reuters noted that less “job-hopping” could reduce wage inflation.

If workers are making less, or simply aren’t getting pay raises, it means there’s less money sloshing around in the economy. This is a good signal for inflation.

To sum it up, it’s a sliver of good news on the employment/inflation front, which could help the Fed get a better read on the state of the economy.

And more importantly, determine if their 11 rate hikes are beginning to take some steam out of the overheated labor market.

It’s Just One Report, But It Can Be the Start of a Positive Mortgage Rate Trend

While this bad economic news, in terms of less hiring and fewer job openings, is good for inflation, it’s simply one report.

We’ve seen similar reports, whether it was a cool jobs report or a CPI report, which indicated the economy could be slowing.

But until we see a series of reports that point to a clear trend, the Fed isn’t going to back off, let alone cut rates.

That explains their higher for longer stance, despite a rate hike pause at the moment.

Ultimately, they don’t want to let their defenses down, only to see inflation increase again, which could require additional rate hikes.

However, reports like these are very welcome news to the mortgage industry and housing market.

While the Fed doesn’t set mortgage rates, their monetary policy can have an indirect effect, which we’ve seen on the way up recently.

High mortgage rates have exacerbated an already major lack of for-sale inventory due in part to mortgage rate lock-in.

And markedly higher rates have quickly led to dismal refinance demand, essentially bringing the industry to a halt.

Housing Affordability Is Dismal as Supply Remains Tight

At the end of the day, affordability just isn’t there for most prospective home buyers with mortgage rates close to 7% and home prices still near to or at all-time highs.

The hope is consumers might see some relief on the mortgage rate component, even if property values continue to defy gravity.

While demand has dropped, inventory hasn’t increased, creating a one-two punch for buyers.

And though a return to the 2-3% range likely isn’t in the cards anytime soon, revisiting the 5-6% range could give the housing market a much needed shot in the arm.

If that doesn’t happen, the Fed’s rate hikes could eventually free up supply a different way, via distress.

We’ve still got more economic reports coming this week, including the ADP Employment Report, GDP, the PCE price index, and the big jobs report on Friday.

If most or all of these reports also indicate that the economy is slowing, mortgage rates could begin trending back lower.

But thus far, it’s been hard to get a rally going as the economy continues to show signs of strength, making some question whether mortgage rates have actually peaked yet.

Personally, I do think the impact of higher rates and a lack of stimulus is beginning to have an impact on the average American.

It’s just unclear how long it will take to convince the Fed that the worst is behind us.

Read more: Why are mortgage rates so high right now?

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026