Real estate Q&A: “Why Is the Housing Market So Expensive Right Now?”

If you asked me this same question a few years ago, I would have had the same basic answer I’m about to explain.

And since that time, home prices have surged much, much higher, which basically tells me the same fundamentals have been at play for quite a while now.

Additionally, they may continue for more years to come.

Similar to a market downturn, when things are hot, they remain hot for years, which is why it can pay to hold on, just like those who didn’t sell their bitcoin at first-profit.

Reason #1: There Is Very Limited Inventory and Lots of Buyers

- Housing supply is at record low levels meaning few homes are available to buyers

- And 45 million Americans are hitting the median first-time home buyer age over the next decade

- While home building has increased lately it’s still stubbornly low and insufficient

- This has allowed a seller’s market to persist for nearly a decade simply because demand outweighs supply

The top reason why the housing market is so high right now has to do with limited inventory, or supply.

It’s one of those fundamental concepts even a child can comprehend. When you have a small or finite amount of something, and people want it, its value goes up.

This is basically what’s been going on with real estate since the market bottomed in 2012.

In reality, supply has been tight ever since the market peaked and the foreclosure crisis took hold because banks were careful to flood the market.

Even back then, it was difficult to scoop up a property because many of them were either foreclosure sales, which aren’t for novice home buyers, or short sales, which took bank approval and months and months to close.

I remember looking at homes in 2012 and it wasn’t much different than today. Sure, home prices were significantly lower, but inventory wasn’t all that great.

Much of what was listed either needed work or wasn’t in the most desirable area. For me, that hasn’t changed over the past decade.

Yes, a good property comes on the market here and there, but if and when it did/does, it becomes a “hot home” and a bidding war ensues.

It’s for this main reason that home prices are at all-time highs nationwide, with the median home valued at roughly $273,000, up from $215,000 in early 2007, per Zillow.

Reason #2: Record Low Mortgage Rates

- Despite a recent uptick mortgage rates are lower than they were a year ago

- This has allowed purchasing power to stay strong while home prices rise

- The only increased burden is a higher down payment for prospective buyers

- It may remove some buyers from the picture but not enough to lower prices

Now if reason number one weren’t reason enough for real estate to be booming, sprinkle in some record low mortgage rates.

To get this straight, there’s a short supply of something people want and it’s on sale from a financing point of view. No wonder everyone is going wild.

While the listing price might be quite a bit higher than it was five or 10 years ago, the fact that mortgage rates are roughly half the price they were then is huge.

This has kept home purchasing power intact despite a big run-up in home prices, basically only making the required down payment an issue for some prospective buyers.

And remember, because there’s a limited supply of homes available, it doesn’t really matter if some would-be buyers are shut out of the market due to affordability constraints.

There are still enough willing and able buyers to come in and pick up any slack, of which there isn’t much of to begin with.

So the bidding war might only have 20 participants instead of 30 – that’s not going to make any impact whatsoever on the final sales price.

Reason #3: Rising Incomes and Inflation

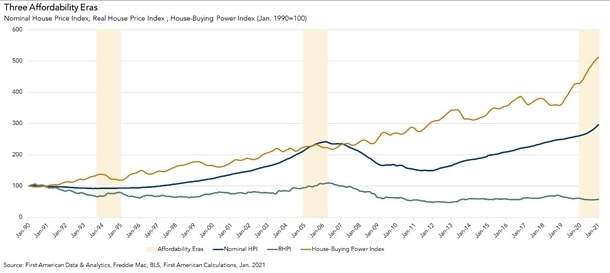

Lastly, we can’t simply look at unadjusted (nominal) home prices and say whoa, they’re even higher than they were back in 2006 when real estate was in a massive bubble. They must crash!

Yes, unadjusted home prices are about 22.2% above the peak seen in 2006 when the housing market last boomed, per First American (see the blue line above).

But that alone isn’t enough to determine whether the market is overvalued or not.

Ultimately, you have to factor in inflation, mortgage rates, and wages to get a complete picture.

Speaking of wages, median household income rose 6.2% year-over-year in January and is up 74.8% since January 2000.

Meanwhile, real house prices (those adjusted for inflation) were about 25.6% less expensive to begin the year than in January 2000.

And so-called “house-buying power-adjusted house prices” are still 47.8% below their 2006 housing boom peak, meaning rather incredibly, there’s still a lot of room to run.

Just check out the chart above – from October 1993 to December 1994, nominal home prices barely budged one percent, but the Real House Price Index (RHPI green line) increased over 20% because purchasing power decreased by 16% due to rising mortgage rates.

Then from January 2005 to March 2006, nominal house prices surged about 13% while mortgage rates remained mostly steady, pushing the RHPI up a big 15%.

At that time, affordability was eroded because nominal home price appreciation far outpaced purchasing power.

Finally, nominal home prices increased more than 13% year-over-year in January 2021, but house-buying power (yellow line) jumped 19% as the RHPI fell nearly five percent.

Why did housing affordability improve despite rising home prices? Because median household income increased and the 30-year fixed fell from 3.62% in January 2020 to 2.74% in January 2021, per Freddie Mac.

In other words, you can’t look at nominal home prices in a vacuum, aka firing up the Redfin app and saying OMG, that $500,000 home from last year is now selling for $600,000!

You need to consider the big picture and factor in wages and how cheap/expensive financing is.

If you look back at that chart, nominal home prices (blue line) have risen steadily since around 2012, and are now above the scary 2006 housing peak levels.

But the RHPI has reached its lowest point since the series got started in 1990, and at the same time the House-Buying Power Index has surged higher, especially recently.

All of this may explain why despite double-digit year-over-year gains and nominal home prices that might be up nearly 100% from 2006, the buyers are still coming. And they’re bidding over asking!

It also supports the idea that the next housing crash (or beginning of a decline) won’t happen for a while still, perhaps my longstanding prediction of 2024.

In other words, if you’re a prospective home buyer, don’t get your hopes up for a discount anytime soon, though if mortgage rates do rise, we might see a moderation in home price appreciation and perhaps less competition.

But the only real relief will come from increased home building, which is beginning to ramp up as housing starts and housing completions are both up significantly year-over-year.

As to how real estate could go from red hot to ice cold again, picture a scenario a few years out when home builders overshoot the mark and mortgage rates are back at 4-5% for a 30-year fixed.

Oh, and asking prices are up another 10-20% from today’s levels. That’s where you can start to imagine another major correction, especially if the wider economy hits another snag.

Read more: 2021 Home Buying Tips

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026