I’ve noticed a trend lately. Everyone’s a real estate expert.

It seems the most recent crisis and recovery has turned just about every single person into a guru on all things to do with home buying and selling.

I suppose part of it has to do with the fact that the massive housing bubble that formed a decade ago swept the nation and was front page news.

It also directly affected millions of Americans, many who serially refinanced their mortgages, then found themselves underwater, then eventually short sold, were foreclosed upon, or held on for the ride back up to new heights.

And now with home prices surging and real estate so expensive, it might be conjuring up not-so-distant memories for some that we could be in for another rude awakening.

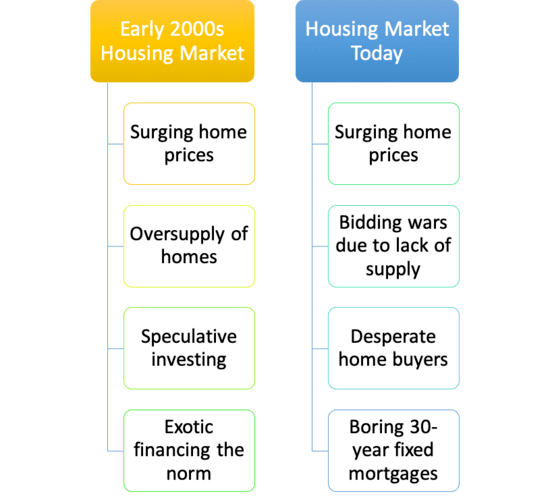

A New Housing Bubble Mentality

- Real estate is red-hot again thanks to limited supply and intense demand

- It can feel like an ominous sign that we’re headed down a dark road again

- But that alone isn’t reason enough for the housing market to crash again

- There have to be clear catalysts and financial stress for another major downturn

It’s a common conversation piece these days to talk about your local housing market.

Thanks to greater access to information, folks are scouring Redfin and Zillow and coming up with theories about what that home should sell for, or what they should have listed it for.

Neighbors are getting upset when nearby listings are not to their liking for one reason or another. What were they thinking?!

Others might obsess over their Zestimate or Redfin Estimate, as if it’s a stock ticker, constantly refreshing it day after day in the hope it has moved higher.

All of this chatter portends some kind of new bubble mentality, though it seems everyone is just basing their hypotheses on the most recent housing bust, instead of perhaps considering a longer timeline.

One could look at the recent run-up in home prices as yet another bubble, less than a decade since home prices bottomed around 2012.

After all, many housing markets have now surged well beyond their previous lofty levels seen about 15 years ago when home prices peaked.

For example, Denver area home prices are about 86% higher than they were in 2006. And back then, everyone felt home prices were completely out of control.

In other words, home prices were haywire, and are now nearly double that.

Meanwhile, the typical U.S. home is currently valued around $273,000, per Zillow, which is about 27% higher than the peak of $215,000 seen in early 2007.

It’s also nearly 70% higher than the typical home price of $162,000 back in early 2012, when home prices more or less bottomed.

So if want to look at home prices alone, you could start to worry (though you also have to factor in inflation which will naturally raise prices over time).

They Say Bubbles Are Financially Driven

While surging home price appreciation can certainly give us all pause, that alone may not be a problem. Well, at least in terms of an impending crash.

They say bubbles are financially driven, and we’ve yet to see a return to shoddy underwriting.

I will say there’s been a lot of near-zero down financing, with many lenders taking Fannie and Freddie’s 97% LTV program a step further by throwing a grant on top of it.

This means borrowers can buy homes today with just 1% down payment, and even that tiny contribution can be gifted from someone else.

So things might be getting a little murky, especially if you consider the big increase in prices over the past four or five years.

However, most new home buyers need larger down payments to “win” homes these days when there are multiple bidders.

One could also argue that affordability is being supported by artificially low mortgage rates, which history tells us won’t be around forever.

There’s also a general sense of greed in the air, along with a feeling amongst homeowners that they’re getting richer and richer by the day. And that it won’t let up.

That type of attitude sometimes breeds complacency and unnecessary risk-taking, and trouble usually follows.

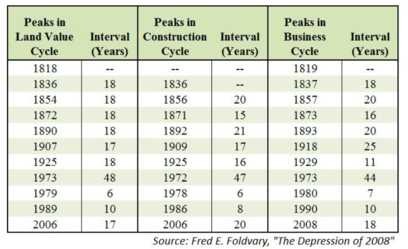

But When Will Home Prices Crash Again?!

- If you believe in cycles, which seem to be pretty evident in real estate and elsewhere

- We will see another housing crash at some point relatively soon

- There appears to be an 18-year cycle that has been observed for the past 200 years

- This means the next home price peak (and then bust) might begin in 2024

All of those recent home price gains might make one wonder when the next housing market crash will take place.

After all, home prices can only go up for so long before they drop again, right? Well, the answer to that age-old question might not be as elusive as you think.

The real estate market apparently moves in cycles that some economists think can be predicted to a relatively high degree.

While not a perfect science, there seems to be “a steady 18-year rhythm” that has been observed since around the year 1800.

Yes, for over 200 years we’ve seen the real estate market follow a familiar boom and bust path, and there’s really no reason to think that will stop now.

It puts the next home price peak around the year 2024, followed by perhaps a recession in 2026 and a march down from there.

How much home prices will fall is an entirely different question, but given how much they’ve risen (and can rise still), it could be a long, long way down.

And we might not have super low mortgage rates at our disposal to save us this time, which is a scary thought.

You’ll Never Get Back Into the Housing Market…

- There are four main phases in a real estate cycle

- A recovery period and an expansion period

- Followed by hypersupply and an eventual downturn

- Don’t believe the hype that if you don’t buy today, you’ll never get the chance!

Another housing bust in inevitable, despite folks telling us we’ll never get back in again if we sell our home today, or don’t buy one tomorrow.

There are four phases to this predictable cycle, including a recovery phase, which we’ve clearly experienced, followed by an expansion phase, where new inventory is created to satisfy demand. This is happening now.

At the moment, home builders are ratcheting up supply to meet the intense demand in the market, with some 45 million expected to hit the average first-time home buyer age this decade.

The problem is like anything else in life, when demand is hot, producers have a tendency to overdo it, creating more supply than is necessary.

That brings us to the next phase, a hypersupply period where builders overshoot the mark and wind up with too much new construction, at which point prices plummet and a recession sets in.

The good news (for existing homeowners) is that according to this theory, we won’t see another home price peak until around 2024.

That means another three years of appreciation, give or take, or at least no major losses for the real estate market as a whole.

So even if you purchased a home recently and spent more than you would have liked, it could very well look cheap relative to prices a few years down the line.

The bad news is that the real estate market is destined to stall again in just three short years, meaning the upside is going to diminish quite a bit over the next few years.

This might be especially true in some markets that are already priced a little bit ahead of themselves, which may be running out of room to go much higher.

But perhaps more important is the fact that home prices tend to move higher and higher over time, even if they do experience temporary booms and busts.

So if you don’t attempt to time the market you can profit handsomely over the long term, assuming you can afford the underlying mortgage.

And remember, there’s more to homeownership than just the investment.

Read on: Will the housing market crash in 2025?

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026

- Light Data Week Means Mortgage Rates Will Be Dictated by Middle East - July 20, 2026

I think you are spot on!

Very interesting, the chart is very helpful. As an investor, opportunities come even when the market is high, just have to analyze better.

Senad,

Indeed, in the past few years you could essentially buy anything, anywhere and still do quite well. That’s beginning to change.

By 2018, the housing market will crash… and it needs to crash. Realtors want you to think it’s all about supply and demand but it’s not. Over 75,000 homes in the bay area are already in pre forclosure stage. (Of course realtors don’t tell you this, as well as banks….. profit earnings) interest rates are also going up, healthcare costs going up as well as living in general. Sadly, people’s income is staying stagnant while everything else is in an upward trend. Also you need to realize that FHA loans cap out at $631k in California. Because the Feds don’t recognize California’s housing prices to be accurate at all. So they won’t lend more than the 631k threshold. We’re over 30-40% above the national average (way off balance) just like the made up valuations (pulled from thin air) of tech companies who sell nothing tangible…. the housing market is also smoke and mirrors. (Just got my MBA from Anderson @ UCLA and have been studying the market here for 2 years now)

I agree the market will peak in 2 years with the decline starting in 2020.

Angela,

Hopefully a little longer than that…or at least a plateau for a while…I think everyone always thinks peaks (and recoveries) will happen sooner than they actually do.

Totally agree with Wokkawokka 7, the housing hyper bubble is about to burst and sooner than many think. I watch market trends very closely as well, and have for years, with accurate predictions. I’ve noticed not only the staggering number of foreclosures, but pages of price drops on listings in locations that were hot six months ago. A flurry of inventory coming on the market too, and so late into the summer is unusual and most likely a sign that sellers want to get out while they still can.

Suzanne,

Why is it going to burst? What will be the catalyst? Very few people have ARMs or unaffordable mortgages, nor do they have better options if they move/lose their current homes.

So my question to you GUGU’S is;

When do i purchase a home? Do wait until the market crashes so i can buy the home at a low price? or do i buy a home now, as the price goes up? If i buy now while prices are rising, im just going to lose market value when i sell in 5 years… so wait until everything crashes, buy, then it only goes up from there…. right ?

Ariane,

Remember, a home isn’t just an investment decision, it’s also a lifestyle choice. You should want the home for reasons beyond the investment, assuming you plan to live in it. And why are you selling in five years? Ultimately, nobody knows for certain when home prices will peak, nor do they know when home prices will fall. Everyone is just guessing and making calculated decisions based on their own interests and risk appetite. I will say that home prices are probably no longer on sale, as they were a few years ago, but that doesn’t necessarily mean they’ve topped out either. Or that they’ll fall anytime soon. Lastly, consider the alternative to buying a home? Is there a better investment right now?

There will not be an 18 year cycle this time. The cycles will be shorter and faster on average due to technology pacing all things faster in our economy.

Maybe return that degree. Lol

The housing market is ridiculously out of balance. Homes that were built in the 50’s, with out of date plumbing and disgusting cabinets and tiny closets and sagging floors are being sold for $300k. I’ll be glad when it does crash. OR wages should go up. How are people supposed to pay these outrageous prices on $30,000.00 a year?

Wokkawokka7 saying the market would (and needed to) crash in 2018 and that s/he just got his/her MBA from Anderson lol. More like the opposite I would say. It’s now going up faster than ever since 2006.

Wishful thinking doesn’t tank markets.

Max,

Yep, these things always take longer to play out than people think. Just as it takes a long time for a market to bottom, it takes a long time for it to top as well. But we are running short on time…2-3 more years maybe?

Catalyst is going to be lots of homes owned by small time landlords getting foreclosed on as people start having to pay rent / mortgages again. There will also, inevitably be an increase in interest rates. Even a few points over the next 2-3 years to try and curb the massive inflation we’ve already been seeing since the beginning of the pandemic will be enough to slow it. Builders won’t realize soon enough and will keep building while people can’t afford and demand drops. Just an opinion.

Brian,

Not a bad take. I too have been trying to wrap my head around the cause of the next housing downturn. Certainly will be overbuilding, perhaps exacerbated by REO inventory. But we’ve yet to see the shoddy financing that makes things go sideways fast, which tells me we are still a few years out, as crazy as that sounds.

Are the new builds actually affordable for first time homebuyers? When I look at Redfin all the new builds are 350K or more and some of those are high end townhouses instead of detached homes. Thoughts or resources for finding the elusive affordable entry level home? I’m looking for a house and trying to figure out if I pay these 10-15% offers over asking price and capping out my budget, going for a complete fixer upper, or holding out for a new build in the next few years that I *might* afford.

I have about half the cash I need for building a house and the other half will come when I sell the home I now live in, in the form of my equity. Last year I was quoted $420k for a 2000 sf house. This spring I am quoted $560k for the same. Are prices truly this fast moving or are builders realizing they can take advantage of the situation? I am trying to determine whether to build my new home or not. I already own the property on which to build. Sure, my current home value has gone up, which is great, but the cost of building has surpassed that increase. So I can no longer call it a lateral wash, so to speak. If building prices are only going to get worse in the next couple of years, I will bite the bullet. But if I’m just being a chump by building now, I had rather wait. What are your thoughts on this matter?

Lisa,

I’m of the mind (and have been for a while) that I’d only buy a house in this market if I absolutely couldn’t live without it. In other words, I wouldn’t be casually buying a so-so house. At the same time, you could argue for a lateral move if you unloaded a so-so house at a great price and bought one you wanted more, even if also expensive. But the other wrinkle now is higher mortgage rates…

As of this day 3/26/2022, interest rate on a 30 yr is tickling 5% again. Fed only did one rate hike last week and at least 3 more this year to come.

Higher interest rates is the pin to the home value balloon.

Funny to see how here we are in May 2022 and all these predictions were off. The big elephant in the room no one is addressing is simply put, manipulative tactics by the fed to price renters out (persuade to buy due to crazy rent) OR price out new home buyers.

Guess who is behind these agendas to swoop in and buy up properties to create a perception of a housing shortage? Organizations like BlackRock.

Dig deeper and you will see the markets, housing and stock, have been completely artificially manipulated and propagandized to cause a frenzy. Didn’t millions of people die during covid? So, who’s buying all these houses? How is there suddenly a “shortage?” Or is is just perception….me thinks the latter. Too many brainwashed sheep listening to so called “experts” who really are jamming ideas down their throat to create an artificial bubble.

Either way, I think there will be a lot of people regretting overpaying 120k++ on a house in 5 years from now – lots of short sales coming in the future folks!!!

Your theory of an 18-year cycle was correct (within 2 years or 15%) 5 times and incorrect 4 times. Pretty close to a coin flip. The other aspect, that seems to be ignored, is that people do not buy homes based on price. They buy a monthly payment. If the price is $1M but the payment is $3000 or $500k with a monthly payment of $3000, to the buyer the “price” is the same. So, the biggest factor is not time or price appreciation but interest rates. When rates rise, sales and prices collapes. When rates decline sales and prices increase. The amount of time between those events is irrelevant. If rates are 1.5% in 2024, no collapse. If rates are 9.5% collapse. And no one can predict where they will be in 2024 but that’ll get you zero clicks.

H,

The P&I might be the same, but taxes and insurance can be a lot higher if the price tag is double. Not sure prices “collapse” as rates rise, though sales might. The rate of appreciation may slow or collapse as you say, yet still be nominally positive.