Have you ever made a decision you later regretted, only to wish you could have taken it all back? Well, you might be in luck if we’re talking about a mortgage.

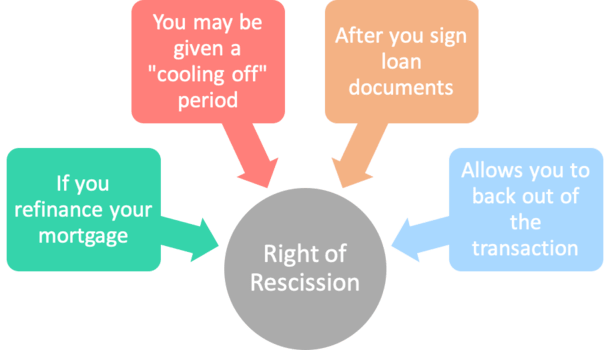

The “right of rescission” period is a provision under the Truth in Lending Act that essentially gives homeowners who are refinancing their mortgages a chance to mull things over before committing to the new loan terms.

Are You Sure You Want to Refinance Your Mortgage?

- When refinancing a mortgage on a primary residence you get 3 days to think it over at the end of the process

- This is known as a “cooling off” period intended to protect consumers from financing they may not actually want/need

- It begins the day after you sign loan documents and ends three business days later (including Saturdays)

- If you have cold feet or simply change your mind you have a right to cancel the loan before it is scheduled to fund

If a homeowner decides to refinance their mortgage, once loan documents are signed, they will have the right to rescind the transaction for a period of three business days.

The right to rescind is essentially the “right to cancel” the mortgage transaction and have any fees refunded if they aren’t happy with the loan for any reason. It’s basically a consumer protection mechanism.

Technically, all fees should be refunded to the consumer if they choose to rescind the mortgage.

This includes all lender fees (application, processing, etc.), broker fees, and third party fees, such as title and appraisal fees, whether paid to the lender or directly to a third party.

The only non-refundable fees are those paid by a consumer to a third party that take place outside of the credit transaction, including things like building and zoning permits.

Assuming the borrower wants to rescind the mortgage, they must provide written notice to the lender during the rescission period.

The bank/lender must then take the necessary steps to indicate that the transaction is terminated by canceling loan documents, filing the release/termination statements in the public record, and refunding fees to the borrower.

This must take place 20 calendar days after receipt of a notice of rescission.

Rescission Period = Time to Change Your Mind

- The rescission period is a time to think it all through for a few days before you proceed to funding

- Take a moment to review your loan and make sure you weren’t pressured or tricked into the transaction

- You can determine if the home loan actually benefits you or the lender/loan officer/broker

- If you want, you can back out without penalty during this time period and get all fees refunded

During the rescission period, the borrower has the opportunity to assess the situation and make absolutely certain they want to go through with the transaction.

At this time, they can think things over and change their mind if need be.

And most importantly, if at any time during those three days they decide they want to back out entirely, they can do so without penalty.

Perhaps you felt pressured by your bank or mortgage broker, or feel you were a victim of predatory lending.

This would be a great time to rescind the mortgage and go someplace else, or not even go through with the transaction at all.

How to Cancel Your Mortgage

You will see instructions on how to cancel your loan on the RoR form, which you’ll receive when you sign loan documents.

There should be a section titled, “How to Cancel” that spells out exactly what to do.

Typically, you just need to sign and date the RoR form and return a copy to the lender (their contact info should be listed on the form) in the allotted time window.

They may also give you the option to send any written statement that is signed and dated that states your intention to cancel.

The deadline should be clearly stated on the form, such as “no later than midnight of January 19th, 2022.”

Ask for clarification if midnight feels ambiguous. They’d probably be better off writing something like 11:59 pm to make it more clear, but I digress.

The good news is you should be able to email the form or statement to the lender within minutes, although fax/mail/in-person options are generally OK too.

However, time will likely be of the essence, so email may be best. It’s also a good way to document that you actually sent it.

Be sure to keep a copy of the form for your own records in case there are any disputes. And follow up with the lender immediately after you send it to ensure they received it.

When the Right of Rescission Period Begins and Ends

- It begins at midnight the day after loan docs are signed

- And ends 3 business days later (it lasts 72 hours)

- This time period includes Saturdays

- But excludes Sundays and federal holidays

The rescission period begins at midnight the day after loan documents are signed, and ends three business days later, including Saturdays, but not Sundays or federal holidays.

It’s essentially three days in between the day you sign and the day the lender can fund the loan.

This amounts to 72 hours, not counting the hours on the day you sign or the hours on the day your loan funds.

Federal Holidays Don’t Count Nor Do Sundays

- New Year’s Day (January 1st)

- Martin Luther King, Jr. Birthday (3rd Monday in January)

- Presidents’ Day (Third Monday in February)

- Memorial Day (Last Monday in May)

- Independence Day (July 4th)

- Labor Day (First Monday in September)

- Columbus Day (Second Monday in October)

- Veterans Day (November 11th)

- Thanksgiving (Fourth Thursday in November)

- Christmas (December 25th)

At midnight on the third business day the rescission period is over, and the signed loan documents become official.

Example of a right of rescission period:

If loan documents are signed on Monday, the rescission period begins Tuesday at midnight and ends Thursday night at midnight. On Friday morning the loan could then fund and record.

If loan documents are signed on Thursday, the rescission period begins on Friday and ends Monday at midnight because Sunday doesn’t count as a business day. The loan could fund on Tuesday morning.

If loan documents are signed on Friday, the rescission period begins Saturday at midnight and ends on Tuesday at midnight. The loan could fund on Wednesday morning.

Assuming there is a holiday in there as well, say Monday for Memorial Day, your RoR will end on Wednesday at midnight, pushing the funding day until Thursday.

In certain circumstances, you may also be able to waive your right of rescission to speed up the loan process, though there must be extenuating circumstances, specifically a “bona fide personal financial emergency.”

It’s not something banks and lenders like to do though so don’t count on it. Instead, plan for a closing date that accounts for the rescission period in advance.

Simply put, in most cases the bank or lender cannot fund the loan until the rescission period is over.

There Isn’t a Rescission Period on All Mortgage Transactions

- RoR only applies to certain types of home loans

- It excludes home purchase transactions

- And all mortgages on vacation homes and investment properties

- Or if the borrower refinances their loan with their existing lender

It’s very important to point out that the rescission period doesn’t apply to all mortgage transactions.

In fact, it is mostly limited to refinances on owner-occupied properties only! Purchase transactions do not have a rescission period.

Additionally, vacation/second homes and investment properties do not have a rescission period, even if it is a refinance transaction!

Also, there is no right of rescission if the borrower is refinancing their loan with the same mortgage lender the loan was originally financed with.

*For cash-out refinances financed with the same original lender, the cash-out amount is the only portion that carries a rescission period.

Home equity lines always have a right of rescission period, unless the entire line amount is used to fund a purchase transaction.

For example, it is quite common for a HELOC to be used entirely as a purchase-money second mortgage, meaning no rescission.

Additionally, reverse mortgages, including HECM loans, generally have a RoR unless it’s used for a home purchase.

Make sure you know your (pardon the pun) rights when it comes to the right of rescission.

Loan officers and mortgage brokers may not give you all the facts, or they may lie to ensure the mortgage funds and they receive their commission, so stay informed.

Lastly, and this goes without saying, be sure you’re 100% clear on the rescission rules for your particular mortgage before you sign, not after.

Don’t be afraid to ask questions early on to avoid any misunderstanding late in the game.

- Rocket Mortgage Completes Redfin Takeover, Offers $6,000 Home Buyer Credit - July 1, 2025

- Mortgage Rates Quietly Fall to Lows of 2025 - June 30, 2025

- Trump Wants Interest Rates Cut to 1%. What Would That Mean for Mortgage Rates? - June 30, 2025

Do I have a right to rescission on my owner occupied 3 family property?

Horace, it depends on the rest of your loan scenario, as discussed above, but whether it’s one or four units is not an issue, so long as it’s owner occupied.

My Wife and I signed our closing docs almost 3 weeks ago. Now the bank requested more documentation before they release the funds and they only gave us 4 hours to provide the documentation, if not we will lose our lock and the rate will go up almost .75%. I know this post is about rescission and our rights, can the banks do this, rescind on us even after we were approved and signed the closing docs?

Henry,

It sounds like the bank is trying to get you to fulfill all conditions and fund the loan before the lock expires. It’s not an issue of rescission.

This can happen pretty frequently – locks expire, are often extended (at a cost to the borrower) when the loan process takes longer than anticipated. If possible, try to work with them to close ASAP to avoid a rate hit.

i signed documents and the rescission started…2 days later, the title company lost some paperwork (a deed from VA) and i had to sign some extra documents. They told me the rescission had to start all over…is this correct?

If the seller wasnt truthful about water leaks on the sellers disclosure & we find mold after closing behind walls do i have the right to rescind the sale? the neighbor confirmed that the seller told him he had water leaks.

DB,

There is no rescission period when it’s a purchase, as noted in the post above. And your issue does not really involve the loan, but rather the purchase itself.

Closed my home refi in Illinois on March 29. Funds were disbursed to original mortgage and I received my cash out. I was laid off and then bank verified employment on April 8th (in which I was not verified). Can the bank cancel my loan???

We had to refinance a line of credit in Nov of 2012. More than a month after signing the loan documents, the bank officer mailed back dated right to rescission forms with a letter asking us to sign and return them to the bank. We did not reply and have now received a second set of these same forms with the same request to sign and return to the bank. Is this legal? What actions, if any can we take against this institution?

Colin, does the right of rescission apply when converting a construction loan (refi) from one lender to another?

Construction loans are generally considered “residential mortgage transactions” and thus not subject to rescission, but ask your lender to be sure. Check out Section 226.23 of Regulation Z. It’s complicated.

Tina,

This article refers to the rescission period associated with new mortgages and refinancing.

can this be abused by borrowers in an attempt to get lower rates?

It’s possible that a borrower could rescind if they no longer wanted to refinance. But going through the process over and over again isn’t something most borrowers are up for.

I signed a home loan purchase agreement for a house. (not a re-fi or investment property). This was on Monday, today is Wednesday. I used the advice of my realtor and found the interest rate I will be paying is going to be 4.75% and the origination fee is $1,200.00. Today I compared rates ( I know, should have done that first) and find I can get a 4.25% rate with a $470.00 origination fee. What would be the next best step?

Gerald,

It sounds like you just signed a purchase contract, meaning you can still shop around anywhere for your mortgage. Obviously the 4.25% rate with $470 fee sounds a lot better than the 4.75% rate with $1,200 fee. But make sure you’re dealing with a reputable lender, and that ALL costs are considered when making comparisons.

In Michigan when does the right of rescission start?

Buying a Freddie Mac home, has 10 calendar day cancellation period re:inspection/condition.

Signed on 3/26. If my 10th day is on on Saturday,then how do I cancel?

Thanks

Mel,

This article is about mortgage rescission, not the inspection contingency related to a real estate contract. Ask your real estate agent.

Does the right of rescission also apply to refinance fees before the papers are signed? We have not signed the closing documents yet, but have paid the app fee, appraisal charges, etc. I’m wondering if we would still be protected under this law and be eligible for the refunds. Please advise, thanks!

It’s supposed to apply to ALL the fees associated with the loan, as mentioned in my article. But most borrowers probably wouldn’t sign loan docs and then rescind just to get those fees reimbursed. They would likely work out a deal with the broker/lender if they were unhappy with anything prior to signing, assuming they still want the loan.

Colin,

i just bought land at eagle rock resort yesterday 28 june, 2014 now i regret buying it. Can I cancel my purhcase and get my deposit back of $2,000

Sandra,

A right of rescission applies to non-purchase loans and the mortgage itself.

Colin,

I had a cash-out refinance on my residence from another lender. I received a letter and a check of 22000 dollars from the new lender which says

:”The truth in Lending Act requires that we notify a borrower at least three business days before a mortgage loan closing if a borrower’s Annual Percentage Rate increases during the application process. We recently discovered that a revised Truth in Lending Disclosure was provided to you at closing, but was not sent to you three days in advance of closing. The increase in the APR resulted in additional Finance Charges to your account.

To address this error, we are refunding the Finance Charges that you previously paid in excess of the amount disclosed to you in the last Truth in Lending Disclosure that you received prior to closing. We have enclosed a check with this letter in the amount of 22000. This check includes the amount of excess Finance Charges you previously paid as well as the amount projected through the life of your loan.

Then I received FORM 1099-Misc which included 21000 under other income.(I am on salary and have no other income)

So when I filed my taxes I included this as Income and had to pay very high taxes on it.

Is this considered income?

Did I have to pay Taxes on this amount?

Is there a way not to pay taxes on this amount or spread it out?

Thanks for your response

George,

It sounds like you need to speak with your CPA or tax specialist to sort out this issue because taxes could be pretty significant on that amount. They should be able to advise you. Sorry I can’t be of assistance.

Thanks for responding to my inquiry.

Your comments on this site is very informative and helpful. I read all the questions and your answers everytime I have questions about real estate and finance.

I wish I did some research and found this site before I refinance, I would have done things differently.

I will recommend your site and your knowledgeable comments and advice.

thanks again for your time.

Thanks for the kind words George, and sorry I can’t be of any help on this specific matter. If you have time, let us know what the issue was so others can avoid similar missteps in the future. Good luck!

What happens after I cancel a refinance with in notice period? Does the current mortgage stay in place?

Your existing mortgage wouldn’t be paid off because no new loan would replace it, so you’d have to continue making payments on your original mortgage.

My question is the total opposite of all the other comments. My home was foreclosed on , and I am being advised by my acquaintance that assisted me with the loan mod and the bk. He assures me that the sale of my home is being rescinded, but there is no proof. He is telling me to stay in the home and become a squatter although, the new owner has taken necessary steps to have me evicted. How am I able to find out for sure if the sale has been rescinded? I’ve already made plans to vacate the premises and rent a home elsewhere because I don’t want a sheriff forcibly removing me.

Sue,

This article pertains to rescission periods on refinances, not home repossessions. Perhaps contacting your county clerk might shed some light.

In 2010 I took out a $40K HELOC on my home through my credit union. I have paid off roughly $15K of that. My house has increased in value and I have completed the paperwork with the same credit union to get a new HELOC for a larger amount – still secured with my primary residence. Since this is a re-finance of a HELOC at the same lending institution…can I waive my 3 day Right of Recision?

My understanding is that there should be a right of rescission because you’re requesting more money (new credit), as opposed to simply refinancing your existing debt. Perhaps just the new money is subject to the ROR. Ask your loan officer to be sure.

Colin,

Thanks anyway. I was just hoping you would be able to help answer what/how we could cancel after the 3 day period. It is a mortgage.

Does interest accrue through the right of rescission?

Colin, Our closing date was set for 1/19/15. The bank called us on this day and said that they had difficulty printing the closing documents and cancelled the closing for that day. They stated in a voicemail that they would not charge us fees to extend our lock and would reschedule. It has now been three days and the lender has not returned my calls asking about when we can reschedule the closing. What rights do I have in this situation?

Thanks!

Anne,

That’s strange but hopefully closing a bit later won’t be an issue for you. There’s no rescission period until after you sign documents.

My husband and I live in Missouri and signed a loan application for a refinance. Now we have decided we do not want the loan. Can we cancel, we have not signed any other papers.

Colin; maybe you can help, but this is similar to George’s issue. I received roughly $14,000 from my mortgage company. The only explanation from them was a letter that said: “We understand that you are unhappy with our services, therefore we are giving you the following checks. You don’t need to do anything but cash them. Although you may want to contact a tax expert.” Nothing else until now it’s tax time & they have provided their tax documents. Can this be considered taxable income? It seems as if this is a “refund” of some sort & should not be taxed again. Can either of you shed any light on my situation?

Brenda,

It sounds like you just applied and have not actually signed closing documents. If that’s the case, it may just entail a cancellation as opposed to a rescission, though it may be subject to forfeiture of non-refundable fees as determined by your contract.

Nina,

I’m not sure what the check was for…probably best to contact your CPA/tax advisor on that.

Colin,

I had a 2nd deed on my home due to a Business loan my wife took. I went to get a HELOC. For some strange reason the lender approved it and we signed the docs. I did n’t want to get into trouble so I told the banker that we have a second deed. Can the lender come after me for their fault of not checking the title report on their end ? they said everything was verified and the HELOC was approved.

Any insight would be helpful

Ravi

Ravi,

Does the lender care about the existing loan? Is it being paid off with the new loan? If they’re aware of it and still approved your loan it doesn’t sound like it’s an issue for them. What did they say?

if full disclosure has not been given, then the time to rescind has not started yet.. Until they do everything they are supposed to and disclose everything they are supposed, then the time hasn’t begun because the transaction isn’t complete.. and I can promise you… they are not going to disclose the truth to anyone.. no sir! you can bet on that!

I’m in the process and will be signing the final closing papers this Saturday, March 7, 2015. Can I rescind before I sign the final papers so I can save the company and myself time? Also….I signed a paper a few days ago re: the Appraisal saying it’s NON REFUNDABLE. The house was appraised and $395.00 charged to my credit card.

But isn’t it Refundable if I rescind within the guidelines of Truth and Lending (Rescission)?

It sounds like if you cancel, the appraisal fee won’t be refunded, but if you rescind and your loan is in fact rescindable, the appraisal should technically be refundable per Paragraph 23(d)(2) of Regulation Z.

How long do I have to give a Lender before I need to cancel and get someone else to do my loan. I feel they are dragging the processes. Also my lock rate have expired and they are not keeping me up to date with progression. I started the end of February now it is the middle of April.

It is just a simple refinance, lower my interest rate, take my daughter’s name off Deed, and no cash out. All my documents have been submitted and accepted

Hi Venita,

You should be able to cancel the loan at any time, just be aware that there may be non-refundable fees unless you actually rescind the loan after signing.

California right of 3 day recession. Regarding a refinance loan, my Credit Union placed my new loan to start 3 days before closing out my old loan with them, allowing interest on both loans for 3 days. Why not start my new loan, replacing the old loan the day after closing the old loan? Can I be charged 2x in interest for 3 days on the same home? Why do they benefit financially for these 3 days and why was I not told till after the 3 days was over that I would have to pay double interest for 3 days? I was told the week before that this was considered padding the loan, that this would be refunded. A week later, the loan officer told me that they have a right to charge me this extra 3 days. Is there anything in California regulation to prevent this from happening. New loan replaces the old loan. Lets say my loan is for 300K. So Im paying interested for 3 days on 600K for my home. This cant be legal. Cant they start the loan 3 days earlier, interest accrues after the old loan is paid off, the next business day.

Hi Colin:

In order to waive the right of rescission, what is typically considered a “bona fide personal financial emergency”? My wife and I were originally set to close on a refinance with cash out tomorrow (May 5th). However, my wife’s mother has had a serious medical emergency (is having a heart catheterization tomorrow morning), and my wife had to leave the country (her family lives in Canada) to attend to her mother. We had to reschedule the closing with the notary for May 7th after my wife returns. But now the lender is saying that due to the right of rescission period, if we close on the 7th they won’t be able to fund our loan until May 12th. Our rate lock expires May 11th, and rates have gone up significantly since we locked in…enough that we may have to consider not going through with the closing. But that cash out money would be helpful to allow my wife to travel to Canada to tend to her mother.

Would this scenario qualify as a bona fide personal financial emergency? It does to me, since the lender won’t fund the loan without re-pricing it if we can’t waive it, and the cash out money would be helpful for travel due to that medical emergency. The only solution the lender provided was to try to obtain POA for my wife and have the closing on May 6th, but I’m not sure if I can get a POA that quickly, and I don’t like that option very much, anyway.

Your thoughts?

Mark,

My understanding is that lenders don’t like to waive the ROR to avoid any scrutiny from regulators so it might be difficult. Best to speak with your lender directly.

Obtaining a loan on our primary residence.

Interest in our property is held in our Trust. My husband & I are co-trustees of our joint revocable trust. I am the sole applicant/borrower. We both signed the mortgage & TIL/Agreement. I was the only one that signed the notice of right to cancel. Shouldn’t my husband also have signed the notice of right to cancel since he is a co-trustee of the trust too? If so, I understand the 3 day right of rescission period does not begin until all that have an interest in the property is provided the notice. Is that correct? If that was correct & my husband was not required to receive & sign the notice of right to cancel, why?

My husband and I refinanced in March. The loan said we would get $2000 at signing because they kept the loan amount the same as when we first applied for the loan last October, and we paid several months of mortgages after that. We never got the $2000 back, despite several phone calls and an email. The lender claims they can’t give cash back due to the type of loan, but he keeps giving us the run around that we will get the money (first after the first month was paid, now after 3 payments). What can I do to get this money that is clearly owed us and is in our loan documentation?

Kara,

If the lender is giving you the run around you could mention making a complaint with the CFPB.

Can the Mortgage Lender unilaterally thrash the signed refinance mortgage closing agreement without giving a reason and ask the customer once again after a month to sign almost the same document (after making little changes to lower the benefits to the customer)? Does the promises made regarding the benefits through an official email during the initial sign-off process by the Loan Officer and the earlier signed document vanishes in thin air? Do the customer legally has any right to know the status of the earlier signed agreement?

Colin, we closed on a loan (VA) in mid April, and it was funded. I received a phone call 16 July (approaching 90 days after signing) from mortgage broker indicating VA is rescinding or is declining our loan due to not meeting all qualifying measures. I asked how could that happen, where did I not meet qualifying criteria. I received no answer except it had nothing to do with financial means. Can I loose my house? Are there any avenues I can pursue if this falls apart? I will say broker was very cordial at the time and said the loan would have to be restructured into conventional at no expense to me.

Colin-

We own a rental home in MO and are currently refinancing it to avoid a couple months of mortgage payments. I would like to list it for sale before the refinance closing. Can I do this or do I have to wait until after closing to list?

Colin,

Can a lender take back their loan months later? Title deed is complete, i pay on time. The thing is they are asking for payroll stubs and bank statements and it has been months since the loan. Legally if i dont give to them can THEY TAKE BACK THEIR LOAN?

Colin, I have a friend who took out a VA mortgage with Bank of America…several years later it was transfered to Nationstar mortgage…. he had some financial problems…nearly lost the home to foreclosure…VA stepped in and had Nationstar do a loan modification with new terms, etc… (seemed more like a new loan)… he paid on it for 16 months and now he has decided to Rescind the loan under the Truth and lending Act… allows up to 3 yrs to make notice to the bank… he feels this Federal law will prevent the bank from Foreclosing on his primary home… According to what I have found… under this Act… lender must repay any fees paid by the owner back to the owner with in 20days… and make the loan null and void… Can this be true.. not have to pay the bank back??

James,

That three-year rule may apply if the lender didn’t provide your friend with the proper disclosures. Normally it’s three days if the correct disclosures are sent.

Is there rescission on a 2nd mortgage refi of the primary residence?

Becky,

There could be if the conditions are met.

I thought that there was no ROR on a construction loan, but our lender has us doing one. Additionally, we are doing this prior to signing any loan docs. It’s been my understanding that you sign the closing docs and then the ROR begins, not the reverse. I’m confused with the process.

Hi Colin,

Maybe you could give me insight on any recourse I may have.

My husband and I refi our FHA loan with QL (they happen to also be the original lenders also an FHA loan). We actually signed and closed on 11/7. Almost a full week later 11/13 they told us there was an error in the taxes and the amount we would receive in cash would be less. They also said that disbursement would be delayed until they could straighten it out. The QL rep also said they were looking into it and would let us know. After a few days and still not hearing from them on 11/16 we told them to just cancel it. Mind you the “official” date to cancel had come and gone (we were not told of this issue until 2 days after the “official” date). The day before Thanksgiving QL called and said the refi (we thought we had cancelled already) was going thru and there was nothing we could do about it. They are disbursing the funds as I type this and I don’t know what recourse I have.

Due to their error I imagine the figures on the disclosing statement have changed from the papers we signed at closing. All in all nothing has been sent or given to us about the new numbers. Wouldn’t they also need us to sign new papers if they made changes AFTER closing?

Colleen,

It sounds like an honest mistake, not an extra fee thrown in at the end or worse terms than what you signed for. That being said, if it’s a large enough difference to make the refinance no longer attractive you could try to stick to your cancellation and fight them on it but I’m not sure if that would be successful. You could also look into filing a complaint with the CFPB if you feel you’ve been wronged by Quicken and perhaps let them know you’re going to be contacting such bureaus.

I closed (Refinanced) and funded my loan 3 weeks ago.. But the broker emailed me and wanted me to back date documents that were attached. as I looked at the documents they were for a different dollar amount..(over 2k) and the payments were a bit higher by $220. I have been reluctant to sign Me because of that she is now threatening to suspend loan if I don’t.

I went to closing on Monday evening. It was after I signed the papers for closing I heard about the 3 day rescission. I want to know. . can I still get the keys to move into the home while this 3 day rescission is in affect?

Nina,

The RoR doesn’t apply to purchase transactions.

If a mortgage is dated May 14 and filed as such, and the closing takes place on May 17, is the 3-day right of recission negated? and what is the remedy?

COLIN,

I am refinancing to combine a first at chase and a second (home equity) at my credit union. I am financing through the credit union. They are very slow and it looks as if we won’t close by the end of lock. I am fed up and don’t want to pay additional fees. If I call it quits at the end of lock I loose my 390 app fee. What happens if I sign to pay to extend my lock to close and then recind. Will I get back all of the fees?

Yvette,

You could ask that they extend the lock a few days as needed in good faith if it is indeed their fault for running over the allotted lock period. If you rescind they technically should refund all costs but then you have to start over elsewhere.

Hi Colin,

I have a refinance for a mother, father and daughter. The property is the primary residence for the daughter. Mother and Father took out an equity on their primary to purchase daughter’s home.

Now they are refinancing the daughter’s home to paydown the equity and do home improvements. Is there a rescission on this mortgage?

Debbie,

Sounds like a refinance on an owner-occupied residence, which per the rules of RoR should apply if a new lender involved.

My bank is running past the rate-lock date with my owner-occupied refi. (their fault, not mine) Rates have dropped since we signed our rate lock, but they’re refusing to honor the new, lower rates at our closing date, telling me that “the locked rate will still apply regardless of the timing.” This is definitely not what my rate lock says. Is this a case where I could rescind after closing to get my fees refunded and start again?

Carrie,

You might try to negotiate with them a little harder to get them to meet you in the middle…it sounds like they’ve agreed to extend your rate lock on their dime at the original terms so it makes sense and is fair in their eyes. Lowering your rate just because they dropped probably isn’t in their agreement, though lenders often play nice and work something out to keep the loan and make the customer happy.

Heather,

Generally the ROR is hard to waive because it is a consumer protection and from what I’ve heard banks don’t like to mess with that.

I am doing a cash out refinance and expect to close today. This mortgage has been delayed several times and had it’s closing rescheduled twice already due to the lender not having correct information in the CD. I have been patiently waiting for this to close so I can help my son purchase a car. His care was totaled during some flooding and we have been juggling cars since. if we don’t get him a car soon he may lose his job due to being unreliable. We will need to finance the car but I of course don’t want to do anything to upset the refi. My questions is after you sign the closing documents but before the rescind period ends can the lender still pull your credit report and cancel the loan based on a change such as an inquiry. I know a new loan won’t show up for some time but the inquiry will.

Robert,

It’s generally best to wait for loan to fund and record before messing with anything just in case…

I am in the process of refinancing my home for a shorter loan period – 15 years – the initial loan estimate was reasonable and we started the process. Have gone through lots of hoops and today I received a notice that said please sign a new load estimate – that they adjusted the loan estimated to ensure I did not need any funds at closing. The initial loan estimate indicated that I did not need any money at closing, costs were being added to my current principal. Even though is was a couple thousand dollars it was still worth it, as I had planned to take the payment that I would be able to miss and apply it directly to the principal.

Long story short, I am not happy with the new loan estimate as it would add $7000 to my principal.

My question is that I’d like to just walk away from this whole deal and not go through with the financing. Can I legally do that? I have not signed any formal loan closing documents yet.

Thanks in advance for your advice.

Myra,

Generally you can walk away at any time if you don’t want to complete the refinance, though you might lose any upfront fees paid for that are non-refundable. With the ROR it’s possible to get those fees reimbursed if you actually pursue the ROR, but that requires getting to the finish line then rescinding…

Ive recently exercised my right to rescind. The 20th day after reciept of recission is approaching. Should I be recieving a refund for the appraisal fees? If so who is responsible for the refund? I gave my card information to the broker but the appraisal mangement company are the ones who charged the card. So is it the lender, broker, or amc? Thanks

Hi, I am at the end of a refinance loan. My question is this, during the rescission period, can the lender pay off credit cards, etc.? I thought the lender has to wait to fund anything until the end of the rescission period. I am asking because I signed the closing docs on Tuesday, but the lender paid off one of my credit cards on Friday (1 day early). I’m only asking because I have attempted to call and email the lender but have been ignored on a constant basis. I am now worried. Your speedy response would be greatly appreciated. Thank you.

Paula,

I’m probably too late on this but let us know what/why it happened if you’re interested in sharing. Strange they would do that, did you want to rescind?

If the disbursement was on the 3rd of the month (Jan), the 1st payment would be Mar. 1, right?

Jennifer,

Depends if you prepaid interest for the month of January…best to ask lender.

Do I have an ability to renegotiate fees with a lender during the rescission period if I think they’re too high or find a better deal and the current lender wants to keep me, or is the only way to start over?

Michael,

The purpose of the RoR is a cooling off period for the borrower to make sure they want to go through with the loan, not to tell the lender they want to change things because it only becomes an option to rescind once everything has been read, agreed to, (hopefully understood) and signed. Before that point you would have ideally expressed any issues you had with costs/fees.

Typically when someone rescinds they either go elsewhere to get a loan or just cancel altogether.

Thank you for your advice, Colin. After doing some additional reading, I realized what a drastic move rescission is, and stuck with my loan, which is actually quite a good one, I think. I appreciate your help and generosity with your time and insight.

We are closing on a house on Monday, we are using our primary residence as collateral and are doing a bridge loan to purchase a new home. I scheduled a week of vacation to move and do some improvement to the new house. I am now being informed that due to our right of recession that the sellers will not receive their check until friday. We have no intentions on exercising our right of recession. My question is when are we allowed occupancy, when we close or after our right of recession has expired?

Brad,

Best to review your paperwork and/or speak to your lender/escrow company directly to be sure.

Does the bank losing the mortgage to another lender receive interest monies during the recession period and how? Is it, perhaps included in the payoff amount?

Colin,

I cancelled my refinance process because the rate went too high. I did not pay anything upfront and now the mortgage broker sent me the bill for credit report and appraisal, do I need to pay for it?

Jay,

Canceling vs. exercising your rescission might be two different things. If it was the former, did you sign anything with the broker regarding fees and refunds?

We closed on a house we were reluctant to buy. After initial inspections, the list of repairs was to broad. At the behest of our realtor we gave the list to the seller. After a lot of haggling between our realtor and the seller (whom was also a realtor) it was decided they would do all the repairs. After this we decided to walk away, because they hadn’t included us in the process or provided us the covenants. Once the seller did we definitely didn’t want the house. We e-signed the cancellation of the contract and the seller refused to sign saying he would give the docs to his lawyer. We ended up closing on the house, but the seller did not complete all irsa items, or have proof of completion of all repairs. We did not sign the irsa, but did sign all other docs. The seller finally furnished a invoice, and the irsa was signed the day before the rate lock expired. I checked the website for the mortgage company and found out that i am a “non-borrower”. What does that mean? And, how long do I have to wait to put the house on the market?

I signed papers with Quicken Loans, but we havnt closed yet and the appraiser is due here in a week, can I get out of this loan(refinance).

Kev,

There are generally two ways to get out – by canceling and possibly having to eat any upfront fees, such as appraisal, or rescinding, which requires signing loan docs and then exercising your RoR. But I’ve mentioned before that it’s somewhat disingenuous to go through the entire process if you just intend to rescind.

I’m curious, if the seller does not want to sign his or her papers until the three days are up, can the lender still disperse the funds the same day if the buyer waits and signs their paperwork on the day of disbursement? Example, Closing will be on Monday the 26th, therefore the lender will disperse the funds on Friday the 30th. The sellers do not want to sign until the 30th. Can the funds be disbursed on the 30th, or will we have to wait another three days after the 30th?

There is a right of recission “RoR” on your primary residence refinance, and always has been. I have been an LO for 13 years, and underwrote for 3 years. The only time I have heard of no RoR aside from NOO or purchase, was with streamline refinances with the current lender (FNMA & FHLMC HARP but it expired, VA IRRRL, or FHA streamline.) This is still a lender to lender business practice, and because it is ultimately the investors guideline and the investor doesn’t purchase the loan/mortgage backed security(MBS) immediately; the lender can make the RoR call to allow recission when it is not. You will not find the word “recission” in the FHA guideline handbook 40001, FNMA selling guide updated 2/6/19, or FHLMC website.

you can do a recission on the loan after 3days and after 3 years if they failed to give you the recission documentation…facts

We signed loan papers on Monday evening and then on Tuesday after looking over the paperwork we had questions. I emailed the mortgage company and they did not respond. I emailed 2 people there. Wednesday, I overnighted the Notice of Right to Cancel. I also faxed and uploaded a copy to the spot we uploaded other documents. I then emailed the guy that was processing the loan that I had mailed, faxed and uploaded the document to cancel, I also included a letter stating that i wished to cancel my refinance with them. The paper said it had to be rescinded by Midnight Thursday. The tracking shows it was signed for on Wednesday. They went ahead and funding on Friday anyways. What can we do?

Shelly,

Did you ever actually speak to anyone since signing, such as a manager, someone senior at the company, or the escrow company involved to see what’s going on. Seems peculiar that no one responded to any of your emails given the gravity of the situation. The CFPB has a complaint process, but maybe getting someone on the phone first could resolve things. Good luck.

Can a lender take back their loan months later? Mortgage was funded and the Title Is deeded, i pay on time. The thing is they are asking for payroll stubs and bank statements and it has been months since the loan. Legally if i dont give to them can THEY TAKE BACK THEIR LOAN?

Lisa,

This can happen and you may find that you signed an errors and omissions agreement (compliance agreement) to resolve any issues post closing.

I just got my final dollar amount for my refinance and I am not happy. It went up. I am supposed to be closing in a couple of days. Do I have too? Should I not close?

Lisa,

Assuming your loan has a RoR, you can walk if you choose to within the cooling off period.

Colin,

If we recind today and our appraisal was done 1st or 2nd week of August can we use it, if we decide to find a different lender?

For how long is that appraisal good from the date it was done?

Brenda,

Check out my article on appraisals and appraised values – it depends on a number of factors, but in many cases they aren’t portable from one lender to the next.

does a rescission period apply to a construction to perm refinance?

Isabel,

Shouldn’t be a ROR as both phases (the initial construction and the permanent financing) would be considered residential mortgage transactions, which are exempt from rescission.

what if the broker adds a separate general contract stating that if you back out of a lock etc you are responsible for his commission etc basically going against right of rescission. Is that legal and hold up in court?

David,

Paragraph 23(d)(2) of RoR discusses refunds including amounts already paid by the consumer that must be refunded, such as broker fees, application fees, appraisal fees, etc. Chances are a broker wouldn’t want to go to court over a few hundred bucks.

I called lender stating I will be opting out of my mortgage. I sent in the required paperwork postmarked before midnight. They went ahead and paid off my mortgage. Now I have a loan I do not want. What are my rights?

“Additionally, vacation/second homes and investment properties do not have a rescission period, even if it is a refinance transaction!”

Does that mean I can rescind at any time without penalty? (beyond the 3 days)

Ayanna,

That means they don’t have a rescission option. So you don’t even get the chance to rescind.

I 100% own a parcel of land in MN and I have hired a builder to build a house on the land. To finance the home, my bank said this would be a refinance since I already own the land, but that it would need to be rolled into the loan with the house. This is because if it ever came to it, the bank would be able to foreclose on both the house and the land under it. I do not currently reside on the land. I am told that I will have a RoR and will not get the keys to the new house until the end of the 3-day period. Does this seem correct? Can I get out of having a RoR?

Kevin,

All I can say is banks are generally averse to forgo the RoR, so generally tough to get out of it.

We signed refinance docs on 10/05/20 and it hasn’t funded for two weeks. How much time does the lender have to fund before it becomes a voided contract? Are we forced to wait and not be able to drop it and start again with another lender? How long is too long to wait for funding before the lender is in default?

Lori,

If you signed docs more than two weeks ago and the loan still haven’t funded, you should find out what’s causing the delay. Are they requesting any funding conditions from you? Seems like quite a long time obviously between signing and funding. And if there’s a roadblock, either resolve it or cancel the loan and move on.

Hi I closed on a refinance in September however I submitted my Notice of Right to Cancel (rescind) within the 3 day window of time (due to various issues with the refinance company). They acknowledged they received it but they still released funds 5 days later and paid my original mortgage loan. They have also acknowledged that I did everything correctly but that on their end they messed up. Now their attorney has finally sent documents with an offer to refinance that refi but there are some numbers not adding up. It is a settlement and release document that they want me to sign before I get to see the actual disclosure for the new loan. And since it’s a legal document it has lots of legal verbiage that is over my head. I’ve been trying to resolve this with them for 2 months. I am getting collection calls now etc and the new loan is on my credit report. It has been very stressful. I have been the one making the advances to resolve it with them but I don’t feel they are still being clear on the loan numbers. Advice? I’ve left msgs with a local real estate attorney however this is such a time sensitive urgent matter and I don’t know how much they will damage my credit etc while I’m trying to get this resolved. (Because I am not paying them the mortgage since I rescinded)

Shelly,

That’s a tough situation. The real estate attorney sounds like the right path, given all the implications and the need to get it resolved correctly/fairly. Sorry I can’t be of any help, but hope you get it taken care of. The silver lining is rates have gone down over the past couple months, so maybe you’ll get an even lower payment when all is said and done…

My husband and I are at the end of a ridiculously mismanaged refi that has taken 5 months to complete and want to rescind this loan. We have e-signed 12 disclosures and haven’t e-signed the latest 2 disclosures nor the closing docs. They want to set an appt for closing but we would like to go with a different lender for a different re-fi loan (10 yr fixed/1.875% instead of a 15 yr fixed/2.5%). How can we rescind this loan without being charged anything?

Hi Molly,

The 3-day rescission window begins once loan documents are signed, which is kind of the tricky aspect of RoR. Without getting to the finish line you don’t actually get to that cooling off period. Alternatively you could ask them just to refund any upfront fees as you intend to rescind. Good luck.

Hi, My mother applied for a reverse mortgage which was supposed to close January 19, but is still ongoing due to one excuse or another. The loan servicer is now being short and rude with her when she calls to get status and they keep asking for more additional documents. She wishes to cancel the application and seek another lender. Would she be responsible for any fees aside from those she has paid up front if she cancels?

Lori,

In order to enact the RoR, she’d need to receive/sign closing documents, then notify the lender at some point during the 3-day cooling off period. If she wishes to cancel before then, it’s clear what fees would be refundable as that might vary by lender.

We signed most of the closing documents for refinancing on our co-op and provided the check to the closing agent last week but later found that a few docs were missing including the recognition agreement. A few days later, we received the agreement but with some errors on it. Now, it’s been past a week and haven’t received the revised one. Since the agreement is unsigned, can we still consider backing up, exercise the right of rescission and get all the money back?

Question: I am in a predicament! I allowed my home to be used as collateral for a business loan. I am not the borrower. Does HOEPA apply?

Some friends of mine invoked their right to cancel, as it was clear the broker hadn’t and wouldn’t explain the points they were paying. The broker told them never to contact him again, but did send a letter with some fees listed as owed to him. These would be credit application and notary fees. My questions is if these weren’t collected up front are they owed? How do you know which fees like the notary, or credit application would still be owed if they were not collected up front? This broker seems like a real piece of work trying to bully these women into signing.

Jason,

My understanding is all fees should be refunded, whether collected or not if the loan is rescinded.

Why is there a different rescission period for investment and primary homes

Kets,

Investment properties do not have a rescission period.

I signed the RoR within 3 days on a Delayed Financing (Cashout) loan and the bank funded my account anyway. I have requested a $500 refund for an apprasial fee taken from my credit card. According to the RoR form the bank has 20-days to to reflect that my home does not secure the increase of credit and to refund my fees. Neither of which has occured and the 20-days expires tomorrow. Today I sent via certified mail a letter offering to return the banks money by allowing them to withdraw the initial amount wired minus the $500. Per the RoR form, if the bank does not take possession of the money (withdraw) within 20 days of my offer to return the money, I may keep it without further obligation. I don’t expect this to occur, however, as inept as this bank is, should the 20-days expire without withdraw do I need to proceed with further action before assuming the money is mine to spend?

I signed for my refi on a Monday the funding date as noted was to be Friday on Friday morning my refi agent informed me that the lenders found a discrepancy something to do with $10,000 that was added to the cash out and that it was too much due to my credit i am lost in this issue and my refi agent is telling me they are bonded and cannot change a signed contract is this true.

What recourse do we have against a bank that recorded a lien on our property for a HELOC transaction that we rescinded within the legal period, however, it has been over 45 days past the notice sent to us acknowledging our cancellation request? (We are trying to close with Lender B yet are at a stand still, because Lender A’s customer service department insists that no one can speak with the mortgage department and no copy of the lien release was ever mailed to us.)