It used to be that a 720 FICO score was all you needed to ensure you qualified for the lowest rate on a mortgage. At least credit-wise.

In other words, anything higher than a 720 FICO didn’t really matter, beyond bragging rights, and perhaps a safety cushion if your score dipped a bit prior to application.

Then came the arrival of the 740 FICO threshold, making it slightly more difficult to qualify for the best rate when applying for a home loan.

Now, Fannie Mae and Freddie Mac are upping the ante, and perhaps rubbing salt in the wounds of anyone interested in getting a mortgage.

They have unveiled not one, but two new FICO thresholds for most conforming mortgages. A 760+ bracket and a 780+ bracket.

A 780 FICO Score Matters for Mortgages Now

In case you’re not aware, mortgage lenders have pricing adjustments for all types of loan attributes.

This can include property type, occupancy, loan type, loan-to-value ratio (LTV), credit score, and many others.

Perhaps the biggest factor in loan pricing is the borrower’s credit score, as it plays a major role in potential default rates.

Simply put, a borrower with a higher FICO score is entitled to better loan pricing on the basis that they’re a lower default risk. The opposite is also true.

As noted, you only needed a 720 FICO score to qualify for the best pricing on a conforming mortgage back in the day.

Then came the 740 tier, which made things a little harder.

Now, Fannie Mae and Freddie Mac are going to require a 780 FICO if you want the very best pricing on your mortgage.

In case you’re wondering, a 780 is a good credit score, but it’s not necessarily excellent. Scores go all the way up to 850, so perfection isn’t needed here to access the best mortgage pricing.

Why Are Fannie Mae and Freddie Mac Upping Credit Score Requirements?

In a nutshell, the FHFA, which oversees Fannie and Freddie, wants them to focus more on underserved borrowers.

This means pricing adjustments have been shifted in favor of those more in need, while new pricing tiers have been introduced for all borrowers to boost capital for the GSEs.

The FHFA believes that “developing a pricing framework to maintain support for single-family purchase borrowers limited by wealth or income, while also ensuring a level playing field for large and small sellers…”

In practice, this means borrowers with low FICO scores and/or limited down payments will often see their loan pricing improve as a result of favorable pricing adjustment changes.

Conversely, traditionally strong borrowers (high FICOs, large down payments) may see their home loans get more expensive.

While there are many changes coming, the biggest standout for me is the new tiers for credit scores, with a 760-779 category and a 780+ category.

Prior to this change, which takes effect May 1st, 2023, a 740 FICO was all you needed.

If you apply for a home loan once these changes are implemented, you’ll want at least a 780 credit score.

Mortgage Pricing Will Get Worse for Many Borrowers with FICO Scores Between 700 and 779

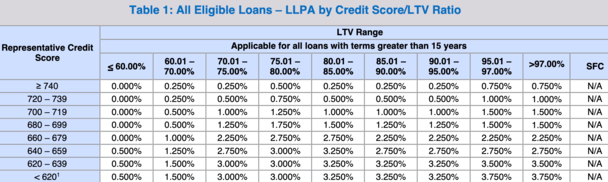

As seen in the second chart above, a borrower with a 740 FICO and 80% loan-to-value (LTV) will see a credit score price adjustment of 0.875%.

That compares to 0.375% for the borrower with a 780+ FICO and 80% LTV. It’s a .50% difference.

On a $500,000 loan, that equates to $2,500 in increased upfront costs or perhaps a mortgage rate that is .125% higher.

So the home buyer who puts down 20% and only has a 740 score (traditionally great credit) will either pay more in closing costs or receive a slightly higher rate.

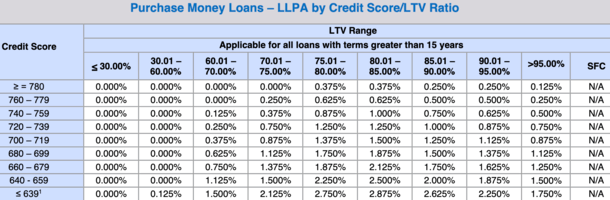

The somewhat good news is a borrower with a 780+ FICO will actually see their price adjustment fall from 0.50% (prior to this change) to 0.375%. See both charts.

It’s bad news for others, such as a borrower with a 739 FICO score and 20% down, who will see costs rise 0.50%.

Note that these adjustments apply to loans with terms greater than 15 years, aka 30-year fixed mortgages.

If we’re talking cash out refinances, the credit score hit for a 780 borrower at 80% LTV will be 1.375%.

Prior to this change, a less creditworthy 740+ FICO borrower got hit with the same price adjustments.

Soon, the 740+ borrower who wants cash out up to 80% LTV will see their price adjustment rise to 2.375%.

That 1% increase in fees is $5,000 on a $500,000 loan, or again, an even higher mortgage rate. Ouch.

And refinances already don’t make a lot of sense given the sleep climb in rates lately.

Do I Need a 780 FICO Score to Get a Mortgage?

Before you get too worried, you don’t NEED a 780 FICO score to get a mortgage. In fact, the 620 minimum FICO score for conforming loans isn’t changing.

However, if you WANT the best mortgage rate, you’ll need a 780+ FICO score. In short, a score 40 points higher than the old top tier.

The change simply requires better credit scores to obtain the best pricing. It’s not locking anyone out.

On the contrary, it’s making mortgages more affordable for those with lower credit scores. And even eliminating the “<620” and “620-639” thresholds, replacing it with a “≤ 639” tier instead.

So depending on your credit score and down payment, it may not affect you. Or it may even lead to remarkably better pricing.

For example, a borrower with a 620 FICO score and a 5% down payment will see their price adjustments fall by a whopping 1%.

That might translate to an interest rate .25% to .50% lower, or simply reduced closing costs. And a borrower with a 3% down payment and 620 FICO will see their pricing improve by an even better 1.75%.

That could result in a mortgage rate .50% or more lower, depending on the lender.

Keep in mind that all LLPAs are waived for HomeReady loans, loans to first-time home buyers with qualifying incomes, and loans meeting Duty to Serve requirements.