Yes, adjustable-rate mortgages are still available, even though your lender may have hidden them from you for the past few years.

Ultimately, ARMs just didn’t make sense for most homeowners because fixed mortgage rates were at/near record lows.

This made the ARM argument a poor one, as there’d be no reason to take on the risk for little to no reward.

As such, banks and mortgage lenders rarely touted these seemingly forgotten mortgages.

But with the 30-year fixed now priced above 5% for the first time in a decade, ARMs have returned.

Do ARM Mortgages Still Exist?

- Banks and mortgage lenders funded over $600 billion in ARM loans last year

- They accounted for roughly 10% of all mortgages originated in 2021

- The 30-year fixed was the most popular loan choice with a ~70% share

- But ARMs are set to surge in popularity now that fixed mortgage rates are much higher

They sure do, and you’ll be hearing a lot more about them in coming months and years.

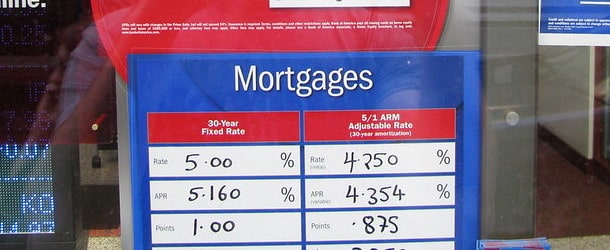

Why? Because the popular 30-year fixed is no longer on sale. A year ago, it averaged 2.99%, per Freddie Mac.

This week, it was pricing around 5.09%, while the soon to be in fashion 5/1 ARM came in at a much lower 4.04%.

During the last several years, ARMs like the 5/1 were priced higher than their fixed-rate counterparts, making them totally useless.

But the spread has normalized and widened in recent months as fixed-rate mortgages have surged in price.

This makes the ARM argument a viable one again for many prospective home buyers.

Interestingly, banks and lenders still managed to fund over $600 billion in adjustable-rate mortgages in 2021.

However, this only accounted for about 10% of overall loan volume, with the 30-year fixed taking a 70% share.

The top adjustable-rate mortgage issuer was Chase, followed by Bank of America, First Republic Bank, Wells Fargo, and U.S. Bank, per HMDA data.

Notice anything about that list? All depository banks! This counters the trend of nonbank lenders dominating the mortgage landscape.

And it’s typically because depository banks will keep ARMs and others mortgages on their books, as opposed to selling them off to third-party investors.

Is Now a Good Time to Get an ARM Mortgage?

The short answer is yes, it can be. The reason being is that ARMs are now a lot cheaper than fixed-rate mortgages.

So if you want to save money on your mortgage for the first five or seven years, it’s possible to do so with an ARM.

As noted above, the 5/1 ARM is priced at about 4%, while the 30-year fixed is closer to 5.125% or higher.

To put that in perspective, a hypothetical $500,000 loan amount would result in a monthly payment of $2,387.08 on the ARM.

After 60 months, you would have paid $95,462.20 in interest and the principal balance would be $452,237.40.

Yes, ARMs pay down your loan balance, despite having a horribly negative connotation from the prior housing crisis.

That is, if they’re not interest-only, which many are not these days.

The payment would be $2,722.43 on the 30-year fixed set at 5.125%, which is $335.35 more each month. That’s a meaningful difference for most folks.

And the loan balance would be $459,951.93 after 60 months, a full $7,700 higher than the ARM.

The total amount of interest paid during that time would be $123,297.73, nearly $28,000 more.

So we’re talking $20,000 more in your pocket after five years, along with a lower outstanding loan balance.

Sounds pretty good, right? The only issue is that the 5/1 ARM can adjust higher after those first 60 months are up.

This may or may not happen, as nobody can accurately predict the future. But if the ARM does adjust significantly higher at that time, it could make the payments unaffordable.

It may also begin eating into the savings enjoyed during those first five years.

Adjustable-Rate Mortgages Are Back, But Know the Dangers

Next time you request a mortgage rate quote, don’t be surprised if you get pitched an ARM, such as the 5/1 or 7/1 ARM.

Simply put, ARMs will sound a lot more attractive because they’re priced lower than fixed-rate mortgages right now.

This allows a loan officer or mortgage broker to give you a better quote than the competition, assuming the competitor only provided a 30-year fixed quote.

But it’s important to know that there are risks involved with ARMs that don’t apply to FRMs.

Primarily, that the interest rate can adjust higher after the initial fixed-rate period.

The good news is the 5/1 ARM is fixed for a full 60 months before it actually becomes adjustable.

And the 7/1 ARM doesn’t adjust until month 85, which again provides a lot of breathing room.

However, that time can go by faster than you think, and it’s important to have a plan in place when that first adjustment does come along.

Those who know they’ll move within that timeframe needn’t worry, but if it’s a forever home you’ll want to make arrangements.

Options include refinancing the mortgage to another ARM or a fixed-rate mortgage, if attractive.

Just be sure you qualify for a mortgage, as life circumstances can change, as can interest rates.

If you’re stuck with an ARM once it becomes adjustable, paying it off early could lessen the blow, assuming you can afford it.

Those who are completely risk-averse will probably want to pass on an ARM, even if it amounts to significant savings.

Either way, put in the time to compare all the options in front of you and make a plan ahead of time.

Read more: ARMs vs. Fixed-Rate Mortgages