In an effort to make life a little easier for its mortgage customers, Chase has launched a new suite of “flexible automatic payments,” including a biweekly option.

If you happen to have a home loan serviced by the banking giant, you should receive information regarding the new payment options, all of which are free.

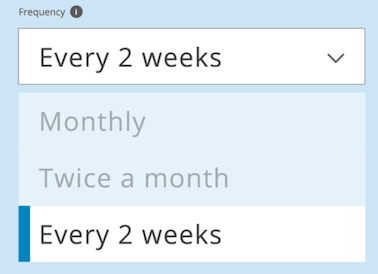

Chase now provides customers with three payment options that are automatically deducted either once a month, twice a month, or every two weeks.

That last option is a biweekly setup, with 26 half payments resulting in 13 total monthly payments annually.

Customers can also continue to make payments manually as well.

Chase’s Flexible Automatic Mortgage Payments

If you had been interested in a biweekly payment program, you can now do it hassle-free thanks to this change.

You can also choose to make payments automatically and/or split your monthly payment into two to correspond with a paycheck.

Once a month option: Choose any date within your mortgage payment grace period and monthly payment is automatically deducted.

Twice a month option: Split your mortgage payment into two to be withdrawn twice monthly, paid once the total amount due is remitted.

Every two weeks option: Make half a mortgage payment every two weeks, funds applied once total monthly payment collected. Results in at least two extra half payments annually with extra applied to principal.

The first two options just allow borrowers to make automatic payments, which can be handy to avoid missing a mortgage payment.

But neither actually save the borrower any money. If anything, option number two could technically cost you money because you’re effectively parting with half your monthly mortgage payment early each month.

While perhaps splitting hairs, that money could be earning interest elsewhere during that time.

However, the third option does result in savings because it’s a biweekly mortgage payment setup.

Because half-payments are made every two weeks, that results in 26 half payments, or 13 full payments, annually.

The additional amount collected is automatically applied to the outstanding principal balance, providing both interest savings and a quicker payoff.

Note that the twice a month and every two weeks payment options may not be available for all loan types.

How Much Can You Save Making a Mortgage Payment Every Two Weeks?

Chase provides an example of the potential savings on a hypothetical $250,000 30-year fixed loan set at 4.5% with escrowed taxes/insurance of $475 per month.

Paying $1,742 once a month results in:

Loan paid off in 30 years

Total interest of $206,016

Paying $871 twice a month results in:

Loan paid off in 30 years

Total interest of $206,016

Paying $871 every two weeks results in:

Loan paid off in 24.5 years

Total interest of $162,094

As you can see, the savings can be pretty tremendous over the course of a couple decades if you elect to take them up on the biweekly option.

The loan would be paid off roughly 5.5 years early and the borrower would realize nearly $44,000 in interest savings.

If your home loan is with a different servicer, be sure to inquire about similar payment options if you’re interested in paying off your mortgage early.

Some may offer similar programs free of charge, while others might do the same in exchange for fees (potentially a setup charge and monthly costs).

It’s also possible to set up your own free biweekly mortgage payment schedule, though you do have to ensure that servicer accepts partial payments and applies them properly, with any excess going toward the principal balance.

Good to see a big lender like Chase being proactive and offering these payment options to their customers.

- Chase Is Advertising Mortgage Rates With Nearly Two Discount Points to Keep Them Looking Attractive - August 4, 2026

- War De-escalation = Lower Mortgage Rates - August 4, 2026

- Mortgage Rates Get Much Needed Relief Thanks to a Taco? - August 3, 2026

I don’t get it.

If the every-two-weeks payment value is basically dividing the original monthly payment value by 2, it means that you are not saving by paying half of the original cost two weeks IN ADVANCE. That is, the mortgage company is the one making more money because they receive half of the payment EARLIER. The interest you’re paying per month is THE SAME.

Might as well save that one month payment value yourself and just add as an extra payment towards principal at the end of each year…

What am I missing here?

John,

The twice a month option just results in a single payment paid at the normal time, as noted in the post. It’s just a preference for someone who might to break up their payments for whatever reason. The every two weeks option actually saves the homeowner money because it results in 26 half payments, or 13 full payments annually.

My question is, does that mean I pay additional interest in that extra payment? If part of my payment is still principal and the other part is still interest, only the extra principal is getting applied to my loan. Wouldn’t it be better to add extra money to my loan so that I don’t give Chase another interest payment? It seems to me that there is an added fee of interest being charged here. Also, I am providing an extra payment, this would be the same as adding extra to your principal without getting charged interest, correct?

Jo,

Any amount above the total due each month would go toward the outstanding balance of the loan, aka principal. It wouldn’t be applied to interest. And because you’d be paying off more of the outstanding balance, subsequent monthly payments would accrue less interest (due to that smaller balance), which is exactly how you save money. While your monthly payments wouldn’t be lower as a result of paying more, the composition of future payments would be more principal-heavy, thereby saving you money on interest.

What is your fee

Chase doesn’t charge extra for biweekly payments.

Why doesn’t chase apply the bi-weekly payments to principal and interest immediately? I can hold my own money for half a month. I’m still on the monthly plan if you’re not applying it immediately.

Bobbi,

It might seem unfair, but mortgages are calculated monthly, not daily, so it doesn’t matter when funds are applied throughout the month. Additionally, Chase or any other lender wouldn’t see it as fair to let you make a partial payment ahead of time to save interest. As you said, you can keep the money in your account all month and just make a larger than necessary payment to accomplish the same thing if you wish.

I already have 26 half-payments paid in a year. I still did not see the two extra half-payments applied to the principal.

Alam,

Is there leftover money in your account? Remember your monthly payments won’t change, just the principal balance. So it might be hard to tell.

A requirement of the loan for the first month is to pay the full amount plus two additional half payments. My question is, do the two additional half payments immediately reduce my principal when Chase receives the payments?

Brad,

If that’s the requirement, I would assume the two half payments would be applied to principal along with the full payment at the time it is due. But I don’t know for sure nor understand why you’d need to make two full mortgage payments initially.

My general understanding is only a full payment amount (or greater than a full payment amount) can be applied, as opposed to a half payment, which sits until the full amount is paid. So if the full amount is there, it should be applied. Not sure why Chase would just hold onto it.

I set up my mortgage for bi-weekly payments. The payments were not handled correctly so I had to call Chase. I was explained what happens with the bi-weekly payments and the twice monthly payments in detail. WHAT A SCAM! The second payment, in both the bi-weekly and twice a month options, will sit there doing nothing “Unapplied” until they get the full payment when the second half comes in at the beginning of the month. No different than if you paid the full amount due at the beginning except that you just gave Chase interest free money to use and you shorted yourself the money two weeks early! The only advantage to the twice monthly plan is that there are 52 weeks in the year so you end up paying an extra mortgage payment every year. You can do this many ways, like paying a certain amount extra every month. Do not fall for Chase’s scam!