It’s time to talk about silly mortgage products!

So I was driving out in Los Angeles today, listening to ESPN radio or some other sports station, when a mortgage ad came on the air.

It was for “Crestline Funding’s MyFi,” which allows mortgagors to choose their own loan term.

When I got home I did a quick search on Google, but didn’t see anything about it, so I don’t know the exact guidelines, or even if it’s spelled that way. Or if it’s offered outside California.

But they did mention a few details on air. Essentially, they let you choose any mortgage term you’d like, ranging from five to 40 years, instead of being confined to the typical 15- or 30-year term.

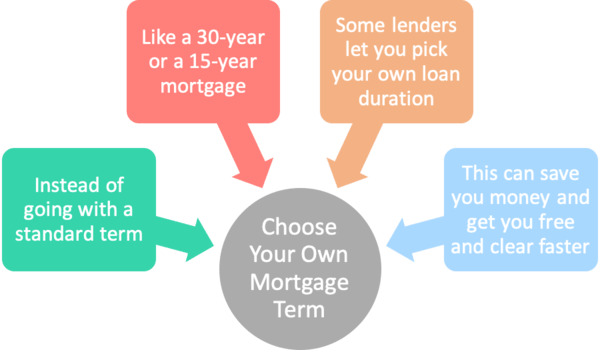

MyFi and the Quicken YOURgage

- Some mortgage lenders let you pick your own mortgage term

- Instead of simply offering a standard 30- or 15-year fixed

- This can be beneficial if you have a specific goal in mind

- Or want to save even more money on your mortgage

For the record, I did come across a similar product offered by Quicken Loans known as the “YOURgage.”

It’s an unfortunate name to say the least, but apparently the same idea as the MyFi, though you can only choose a term between eight and 30 years.

Simply put, if you don’t want a standard 30- or 15-year loan term, you can ask them to refinance your mortgage into an 18-year fixed or a 24-year fixed loan. Or anything else in between.

Presumably this will save you money because the interest rate should be slightly lower if you take a shorter term.

For example, a 15-year fixed will always price lower than a 30-year fixed. In fact, 15-year fixed mortgage rates are about 0.75% cheaper than 30-year rates at the moment.

(30-year fixed vs. 15-year fixed)

So if you choose a 13-year fixed, you may be able to save a little bit more money than if you went with a 15-year fixed.

Even if the interest rate isn’t discounted, you’ll also save money with a shorter loan term as less interest will be paid over a shorter amount of time.

However, the monthly mortgage payment will be higher if the loan term has a shorter duration, so there are some drawbacks as well.

Shorter Term Mortgages Can Save You Big Money

- The shorter the loan repayment period

- The less interest you’ll pay over the life of the loan (all else being equal)

- So if you can manage to pay your home loan off in a shorter amount of time

- You have the potential to save a lot of money

That got confusing, so let’s sum it up real quick.

Shorter mortgage term = lower mortgage rate.

Shorter mortgage term = faster amortization.

Shorter mortgage term = less interest paid.

As you can see, there are two benefits to going with a shorter-term mortgage. You can often snag a lower interest rate, and you pay less because the loan amortizes faster.

So it’s a double reward. But is it really necessary to pick a loan term in between the standard stuff that’s offered?

Why Choose Your Own Mortgage Term?

- To match your unique budget

- Or to meet a specific time goal like retirement

- To avoid extending your mortgage term when refinancing

- And to simply stay on course if you wish to pay off your mortgage in full

Well, Quicken’s argument for its YOURgage is that you can choose a term based on your budget, or a term that matches up perfectly with specific life events.

For example, if you plan to retire at a certain age, you can set the mortgage term to finish right as you’re retiring.

Or you can pick a certain term that comes with a mortgage payment that works seamlessly with your budget.

And if you’re refinancing but don’t want to “reset your mortgage,” you can choose a term that keeps the combined term at the standard 30 years.

So if you’ve had your existing mortgage for seven years, you can refinance into a 23-year fixed.

The big question remains whether the savings justify the unconventional loan term. How much will going with a 13-year fixed vs. a 15-year fixed really save you?

And are these lenders your best option? If mortgage rates are cheaper with another lender, you don’t need to pick a funky term to save money.

Additionally, you can set your own payment schedule manually and make larger payments to pay off your loan in a certain period of time if need be.

Simply pay X amount more each month toward principal to pay off your mortgage by Y date. It’s pretty straightforward.

In other words, you may be better off shopping around and gathering more mortgage quotes to obtain the lowest rate rather than worrying about term.

Read more: How to pay off your mortgage early.

- Soft Jobs Report Takes Pressure Off Mortgage Rates - July 2, 2026

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026