What I’ve seen and heard through the years is certain lenders not being so forthcoming with existing customers wanting to refinance their mortgage.

For example, when a homeowner goes to inquire about the “awesome low rates,” their first instinct may be to pick up the phone and call the lender who gave them their current home loan.

Or perhaps they make contact with their loan servicer, the company that collects their mortgage payments each month.

The problem is some lenders may respond with, “you’ve got a killer rate already.” Or, “why would you refinance, your mortgage rate is already the lowest in history!”

They’ll say this in their most convincing tone, though it’ll be pretty clear they’re lying through their teeth, assuming your rate is much higher than today’s going rates.

So why are they throwing up roadblocks, as opposed to quoting you a new low rate and getting your loan application started?

Well, it could be that it’s not in their best interest, regardless of the fact that it may benefit you.

Your Mortgage Rate Could Be Substantially Lower

- Mortgage rates have hit 13 record lows so far this year

- And they might not be done going down yet!

- You need to keep an eye on rates to see if a refinance could be beneficial, even if you recently refinanced

- Always take the time to look beyond your current lender/loan servicer for pricing

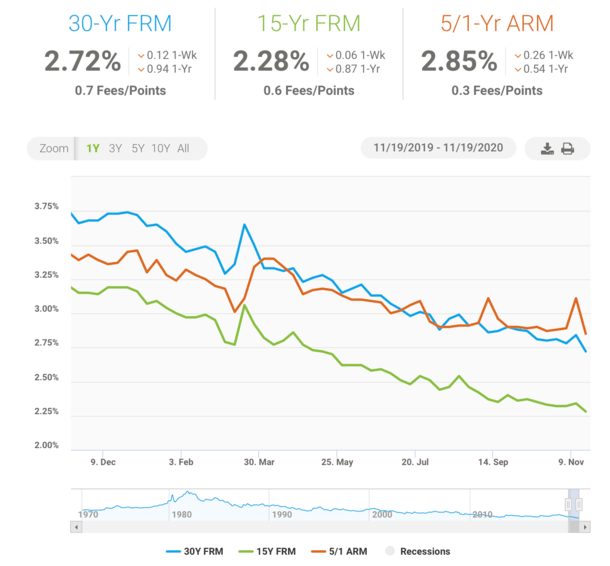

At last glance, mortgage rates have hit 13 new all-time record lows this year, per Freddie Mac. And we’ve still got another 40 days or so left until 2021.

For perspective, a homeowner may have refinanced into a 30-year fixed back in January 2019 when rates were close to 4.5%.

Today, that same loan scenario may be pricing closer to 2.75%. That’s a whopping 1.75% difference in rate, surely convincing enough to refi.

Heck, even if you refinanced your mortgage back in January of this year, there’s a good argument to give it another look and refinance a second time.

At the start of the year, the 30-year fixed averaged 3.60%, which puts it nearly a point higher than today’s levels. Just look at that chart above!

In other words, if you got your mortgage two years ago, or even just six months ago, when the 30-year fixed was hovering close to 3.5%, you could be overpaying on your mortgage.

Today, lenders are dishing out 30-year fixed mortgages around 2.75%, so clearly a refinance can benefit a ton of homeowners, even those who refinanced during a period they thought was the lowest point EVER.

Now who exactly is telling borrowers not to bother with another refinance?

Well, this tends to be more of an issue for those who call the bank their home loan got sold to, as it wouldn’t really benefit the lender to offer a lower rate.

Or if you revisit your loan with the bank or mortgage broker who just refinanced you a few months ago, they may be at the mercy of commission recapture (essentially they forfeit their earnings if you refi too quickly).

Simply Shop Your Mortgage Elsewhere

- Loyalty often doesn’t get you anywhere in the mortgage business or elsewhere

- Take the time to get multiple mortgage quotes from a variety of lenders

- Even if your original lender/broker is willing to help, get other quotes as well to compare pricing

- Also watch out for those who are constantly telling you to refinance

If you encounter any resistance when inquiring about a refinance, it’s not the end of the world, not by a long shot.

For example, if you call your lender and ask about a rate and term refinance, thinking it could save you money, they may tell you to not to bother.

No worries. All you need to do is call a different bank, credit union, or mortgage broker and have them price your loan instead.

It’s pretty darn simple really. Your current lender may not want to lift a finger to help you save money, but there will be many others champing at the bit to get you that refinance.

So don’t be discouraged if you are told otherwise. Simply say thank you, hang up the phone, and get in touch with other lenders.

After all, if you could stand to save hundreds to thousands of dollars annually, it’d be pretty imprudent not to inquire about a refinance.

Heck, even if your current lender does offer to refinance your mortgage, you should shop around. Not shopping means you won’t know what else is out there.

It’s something you should do no matter how wonderful or easy to use your current lender is. They may have had the best pricing last year or six months ago, but not today.

This is why I recently said if your lender reaches out, reach out to other lenders.

At the same time, be sure it makes sense to refinance your mortgage. It isn’t always going to be the right move for a variety of different reasons.

Lastly, watch out for overzealous loan officers looking to serially refinance your mortgage every time rates drop by some minimal amount, which may benefit their pocket but not yours.

Read more: When to refinance a mortgage?

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026