It seems 1% down is the new zero down in the mortgage world, with San Diego-based Guild Mortgage the latest to join the fray.

The independent mortgage bank, like others before it, will take advantage of a grant to give homeowners instant equity, while requiring just 1% from the borrower’s own funds.

The 1% down home loan program is a new form of down payment assistance, though unlike similar programs that preceded it, the gift doesn’t need to be paid back and the borrower actually gets some skin in the game.

Guild Mortgage’s 97% LTV with a 2% Grant and 1% Down Payment

- Like other 1% down mortgage options available

- Guild is relying on a 2% grant that doesn’t need to be paid back

- But there are lots of guideline restrictions

- Including income limits and credit score minimums

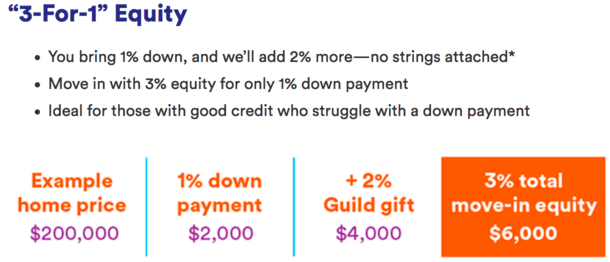

Aspiring homeowners who take advantage of the Guild 1% Down loan program can instantly acquire 3% equity in the property they purchase despite only putting down 1% thanks to a two percent grant that doesn’t need to be repaid.

Quicken has a similar program, as does United Wholesale Mortgage if you go the mortgage broker route.

Guild Mortgage refers to it as “3-for-1” equity with “no strings attached,” and say it’s ideal for those with good credit who lack the necessary down payment funds, a common problem these days.

This gifted grant money is subject to income limits, required homebuyer classes and other criteria, though income limits don’t apply in census tracts that are designated as low-income.

It’s basically intended for low-and-moderate-income first-time home buyers who have difficulty coming up with a down payment, though repeat buyers are also welcome to apply.

The program does require a minimum FICO score of 680, which is slightly below average nationwide.

As far as income, it can be up to 100% of area median income, or without limits in low-income tracts.

Guild Mortgage Allows for Flexible Income Limits and Sources

- The program allows DTI ratios up to 50%

- Along with the use of non-borrower household income and boarder income

- Loan amounts capped at the conforming limit

- And it requires private mortgage insurance to be paid

Speaking of income, Guild Mortgage’s loan program allows DTI ratios as high as 50%, which is pretty forgiving for a 1% down mortgage program.

And to sweeten the deal, they allow non-borrower household income and boarder income, the latter being a tenant/renter that pays you to live in the property.

In other words, if someone agrees to rent one of the bedrooms in your house for $500 per month, you can use 75% of that (to account for vacancy) and apply $375 toward your total income to meet DTI limits.

Loan amounts are allowed up to the conforming limit, which is $453,100 in the contiguous United States and even higher in Alaska and Hawaii, so it sounds like it’s backed by Fannie Mae or Freddie Mac.

The product does require private mortgage insurance, but it is cancellable and offered at a reduced rate. Again, this aligns with the 97% program backed by Fannie and Freddie.

Both single-family homes and condos are allowed, though it’s unclear if more than one-unit is permitted. The property does have to be owner-occupied, obviously.

There’s no mention of loan type, but my guess is they will primarily offer borrowers a 30-year fixed product. Not sure if ARMs are an option here given the implied higher risk of a low-down payment mortgage.

Guild Mortgage originated a healthy $15.9 billion in loan volume last year, up from just $1 billion back in 2008.

The company also services more than 155,000 home loans, and has correspondent lending relationships with credit unions and community bankers in 47 states.

- Soft Jobs Report Takes Pressure Off Mortgage Rates - July 2, 2026

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026