Lately, the home builders have been struggling to sell homes. And the culprit has been affordability.

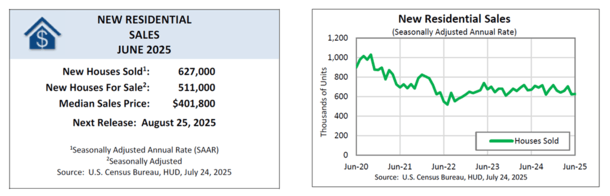

In June, new single-family home sales fell to an annual rate of 627,000, per the Census Bureau.

That was up slightly from May, but down the June 2024 sales rate of 671,000.

At the same time, the supply of newly-built homes climbed to 9.8 months at the current sales rate, up from 8.4 months a year ago.

This has sparked a lot of worry about a possible repeat of the early 2000s, but the way they’re selling homes has changed tremendously.

Home Builders Are Motivated Sellers, But It’s Getting Harder to Sell

I’m not going to sugarcoat the current situation. The housing market is tough right now. It’s hard to make the numbers work if you’re a prospective buyer.

Home prices are steep, mortgage rates are way up relative to the past decade, and inventory remains constrained due to post-GFC underbuilding and mortgage rate lock-in.

New home inventory has basically doubled from pre-pandemic levels, from a five month-supply to a near-10-month supply.

Supply was closer to seven months a couple years ago, and as low as three months during the pandemic.

It spiked to 12 months in 2009 in the aftermath of the 2008 financial crisis before steadily declining for about five years.

But it has become clear that homes are no longer flying off the shelves. The same is true of existing inventory, which is now becoming fairly balanced as well.

The National Association of Realtors (NAR) reported that existing home supply climbed to 4.7 months in June, up from 4.0 months a year earlier.

That points to a balanced market between buyers and sellers, at least nationally.

But much of that is homes sitting on the market for longer, not so much new listings coming to market.

Sellers are equally cautious to list, and many who have seem to be would-be sellers, meaning they list “high” and lack motivation to drop their price.

How Home Builders Used to Sell Homes

That brings me back to the builders and their motivation to sell. They aren’t occupying the homes, so once they’re built, they want to unload ASAP.

Back in the early 2000s, they were doing this with 100% financing and questionable lending, which we all know didn’t turn out too well.

For example, a buyer back then may have received an 80% first mortgage and a 20% piggyback second mortgage, with the deal only subject to stated income underwriting.

To make matters worse, the loans may have been adjustable-rate loans, or worse, option ARMs that allowed for negative amortization.

The cherry on top was these homes were selling at the height of the market, with shoddy wild west appraisals backing up the valuations.

To summarize, you had a home buyer in way over their head who often had no business getting to the finish line.

You also had a flood of inventory, half-built housing tracts, and all the “used home” homeowners alongside them, who were overleveraged as well.

They were doing the same thing, taking out cash-out refinance loans to 100% LTV to fund discretionary purchases.

How Home Builders Sell Homes Today

Clearly we don’t want to repeat history and do what we did back in 2006. The good news is we have rules in place, namely ATR/QM, which prohibits many risky loan features.

Today, the vast majority of mortgage loans have to be underwritten with proper documentation and the loans themselves have to fully-amortized, max 30-year loan terms, sans negative amortization, etc.

Simply put, there are guardrails today that only exist because of the early 2000s housing crisis.

That means the home builders unload their inventory in a different way today.

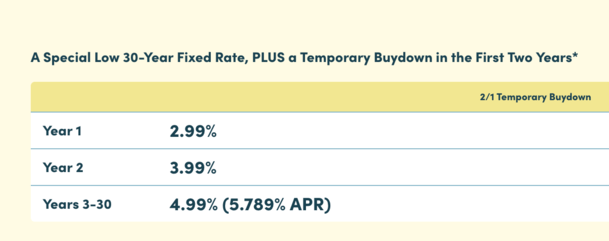

But how? Well, they lean heavily on mortgage rate buydowns that lower the interest rate on the loan, typically permanently.

While there are both temporary and permanent buydowns, many builders have relied on both to make deals pencil.

For example, a home builder’s lender will offer a 30-year fixed bought down to 4.99%, with a temporary buydown of 2.99% in year one, 3.99% in year two, and 4.99% for the remaining 28 years.

Not only does this make the monthly payment way lower for the home buyer customer, it also makes it sustainable.

They’re not stuffing the buyer into a bad loan that will blow up in a few years. They’re reworking the numbers to get to a spot where it’s affordable.

This doesn’t mean everyone should run out and buy a newly-built home. Or that it’s necessarily a “good deal.”

But at least the way the builders are selling today is on the complete opposite end of the spectrum compared to back then.

It means things are different this cycle versus last, even if it feels like we’re so back.

Read more: One Major Reason Why the Housing Market Is Much Better Off Than It Used to Be

- Mortgage Rates Hit 2026 Highs, Look Headed Back to 6.50% - March 19, 2026

- A Home Builder Is Offering to Cover Your First 12 Mortgage Payments - March 18, 2026

- Pending Home Sales Eke Out a Beat Thanks to Lowest Mortgage Rates Since 2022 - March 17, 2026