The “option ARM” loan program was one of the most popular mortgage choices for borrowers in the United States during the lead up to the mortgage crisis thanks to its forgiving payment flexibility.

This same payment flexibility also made it one of the most scrutinized loan programs in history because of its misleading ability to qualify borrowers for a home they truly couldn’t afford.

It was offered by some of the biggest former mortgage lenders, including Countrywide Mortgage and Washington Mutual, both of which failed during the Great Recession. I believe Bear Stearns also offered the product. They also failed.

What Is An Option ARM?

- It’s a home loan with four payment options

- That provides for greater payment flexibility

- In the event the borrower is paid unevenly throughout the year

- Or simply wants a variety of choices when it comes to paying back their mortgage

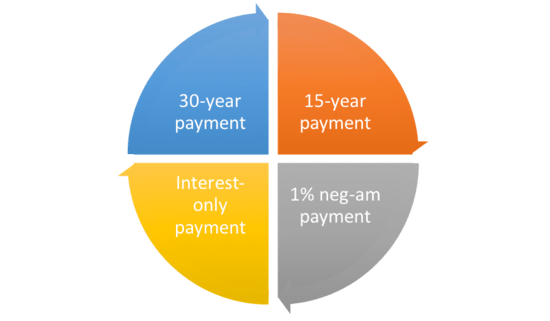

The option ARM, or pick-a-pay mortgage, is a monthly adjustable rate mortgage tied to one of the major mortgage indexes, including the LIBOR, MTA, or COFI. The program allows a borrower to pay off their loan balance using four payment options, including the following:

– 15 year term payment (Principal and interest)

– 30 year term payment (Principal and interest)

– Interest-only payment (Usually available first 10 years)

– Minimum monthly payment (Negative amortization payment)

In other words, borrowers can make the standard 30-year fixed payment, an accelerated 15-year fixed payment, a 30-year interest-only payment, or a negative amortization payment.

That last option was what got a lot of homeowners into a lot of trouble. It allowed homeowners to pay less than the total amount of interest due, thereby pushing many borrowers into an underwater position.

Most Option ARM Holders Make the Minimum Payment

- The problem with option ARMs

- Is most borrowers didn’t understand them

- And simply made the minimum payment each month

- Then couldn’t afford the eventual higher payment

Most borrowers select the option ARM for the minimum payment option, otherwise known as the negative amortization option. The minimum payment option allows a borrower to pay monthly mortgage payments that are significantly less than the actual interest rate.

The minimum payment on most option ARM programs is 1% fully amortized. It seems like a great deal, but every time the borrower elects to makes the minimum payment, the difference between the minimum payment and the interest-only payment is tacked onto the balance of the loan.

A borrower can pay the minimum payment until the loan balance reaches 110-115% of the original loan balance, depending upon the rules of the issuing bank or mortgage lender. This allows the typical borrower to pay the minimum payment for roughly the first five years of the life of the loan.

After the borrower reaches 110-115% of the original loan balance (110-115 LTV), they will lose the minimum payment option, leaving them with the three remaining payment options. After ten years from the start of the loan, the interest-only option typically goes away as well, and the borrower must pay using one of the two remaining payment options.

Typical option ARM programs do not have any caps aside from the lifetime cap of say 9.95%, and the minimum payment generally increases 7.5% each year until it is no longer an available option.

You’re Deferring Interest with an Option ARM

- If you make less than the interest-only payment

- You are deferring interest

- Which means your outstanding loan balance grows

- And eventually it must be paid back in full

What many borrowers may not understand is that paying the minimum payment each month is simply a way of deferring interest, not avoiding it altogether. By making the minimum payment each month, the accrued interest eventually stacks up against the borrower, while effectively building zero home equity.

And after five years of paying the minimum payment, the borrower would have a loan balance above their original balance without the flexibility of the minimum payment option.

This makes the option ARM a dangerous choice for homeowners, as once the minimum payment option disappears the borrower has no choice but to pay the interest-only payment. And many borrowers will likely have trouble making the interest-only payment after relying on a much lower minimum payment during earlier years.

The only saving grace to this program is housing appreciation and leverage. While the market was hot, real estate investors were using option-arms to keep cash in their pockets, banking on appreciation until they resold the home years, or even months later.

But once every one and their mother was using this type of loan, trouble started brewing. It probably should have never been introduced to the masses.

Let’s look at a simple example:

1 Month LIBOR index: 5.330

Margin: 2.65

Fully indexed rate: 7.980%

Loan amount: $400,000

15 year term payment (Principal and interest) = $3,817.99

30 year term payment (Principal and interest) = $2,929.48

Interest-only payment (Usually available first 10 years) = $2,660.00

Minimum monthly payment (Neg-am payment) = $1,286.56

Minimum monthly payment Year 1 = $1,286.56

Minimum monthly payment Year 2 = $1,383.05

Minimum monthly payment Year 3 = $1,486.78

Minimum monthly payment Year 4 = $1,598.29

Minimum monthly payment Year 5 = $1,718.16

Typical five-year interest-only adjustable rate mortgage at 6.75% is $2,250.00.

Monthly savings making the minimum payment = $963.44

As you can see, the minimum payment is dramatically lower than the interest-only payment, but it won’t be around forever. And the minimum payment increases each year, as well as the accrued interest.

I’ve seen a lot of lender commercials lately offering option ARM programs under the guise of names such as “Super-Saver program” and “Smart Option”. They tend to highlight the benefits, mainly the cost savings without mentioning the negative implications.

The newest option ARM program now is the so-called “assured option arm”, also known as a five-year fixed option ARM mortgage. It combines the safety of a five-year fixed product with the flexibility of an option arm. It can be useful for the same reasons I mentioned above, with the security of a fixed interest rate for a small time period. But it’s still a risky loan product, and one that should be approached cautiously as well.

All that said, the option ARM program definitely has the potential to save homeowners money, and keep money in their pocket during hard times, but it should be approached cautiously.

A loan officer or mortgage broker may recommend the option ARM program as a way to keep your payments down, but if you don’t feel you can make the interest-only payments in the future, and eventually the much higher fully amortized payment, it’s probably best that you look for something more conventional.

If you can’t make the fully amortized payment, you don’t really qualify for the home loan. Bottomline.

Option ARMs Banned Post-Crisis

- The option ARM will go in history

- As the most infamous home loan of all time

- For single-handedly taking down storied financial institutions

- And leading to the largest financial crisis in American history

In early 2014, the Consumer Financial Protection Bureau (CFPB) enacted the Qualified Mortgage (QM) rule, which required lenders to stop making mortgages with what they referred to as “harmful loan features.”

One of these features turned out to be negative amortization, meaning the option ARM as we knew it was a thing of the past. Lenders get certain legal protections if they make loans that abide by the QM rule, and as such most loans are now QM loans.

However, it’s still possible for a lender to offer a similar product in the future, but it’s doubtful because they’ll be assuming more risk. And we all know these are risky loans.

In summary, the option ARM will go down in history as one of the most infamous loan programs of all time. One could easily argue that they did a lot more harm than good, and were probably one of the main reasons everything fell apart.

I am actually looking for a lender who offers option arms? Do you know if anyone still offers these types of loans post-crisis?

Haha…no, I do not. But if mortgage rates and home prices keep rising, a lender might start offering the program again to keep things “affordable.” But let’s hope that doesn’t happen again.

I’m a student who is doing a research paper on ARM mortgages. One thing I’m not clear on, I don’t believe I have found the right source yet, Are Option ARMs still legal to produce?

Heather,

I’ve seen legislation that banned option arms for “high-priced loans,” and more recently loans with negative amortization have been banned under the Qualified Mortgage definition, which looks like it will be the standard going forward. In any case, no lenders seem to be offering option arms these days regardless.

These were the worst mortgages in history…I wonder how many people lost their homes after taking out an option arm.

i am looking for greenpoint credit -suite30017 p.o.box 969079 san diego calif. 921126 1-888-455-1319. thanks for any help you can give me j.a. rich

My present home is currently paid for – I need a larger home and in order to not have to rent an apartment in between the selling process and the buying process – the inconvenience – is there a bridge loan available? Is there a choice of different options for my situation? If so, what are they? My new home will be paid for also.

Carlan,

There are a few options, including bridge, home equity lines or loans, or iBuyers and similar disruptors that pay cash for your home.

I may be the only mortgagor of an Option ARM from Countrywide (CW) happy with it over 15 + years.

But, I was cheated out of amortization beginning Month 2, through Month 12 in this way:

This loan was promoted and advertised widely as “Special – Year 1 interest 1% with Amortization” with the Index and Margin calculation of monthly interest to commence beginning Year 2. I was impressed and had detailed discussions with CW’s originator in my local CW office (no brokers, they worked directly w CW). I had him and his boss the CW Branch Mgr., confirm, not only that Amortization/Principal Paydown would occur each of Months 1-12, but they told me that with NO Prepayment Penalty, I could refinance by Year 2 after paying down my $650,000 mortgage to $631,268.

However, when the loan contract arrive at my settlement attorney’s office, he quickly called me and said that it was silent on the Y1 am. I had three days Right of Rescission so I called the originator again. His secretary confirmed Y1 am in an email but no one at CW could edit the contract language. Believe it or not, I actually reached CEO Angelo Mozilo’s office, talked to his top aid while Mozilo was right there. Mozilo confirmed “Am. every month, Y1 and connected me with his SVP Anthony Rizzotto who engaged me for about 20 minutes, thanking me for pointing out the “sloppiest loan language I’ve ever seen” and even calculation FV – the future value or PB, Principal Balance after my first 12 on-time payments of Principal and 1% Interest. “I’ll send you an email confirming and this ca serve as an Addendum to your contract with us and you can close in 3 days (while I would be on a business trip), until we can re-write this loan contract and rescind the original one. No email all the next day. Rizzotto’s secretary took my call, “If Mr R told you he” amend, he will!”. 3d/final day of RofR period, still no email, but I had the second half of that day flying home. No email. But, with all the oral confirmations and the email confirmation from the originator’s secretary, I let my escape hatch close.

I continued to call and email Rizzotto, Mozilo and the local originator. No longer were my calls and emails eliciting responses. I was ignored.

I made the first payment @ 1% and Month 2 statement credited a bit of amortization. I made my second payment but a couple weeks later when my Month 3 statement arrived – $0 am! And so it went, month after month; paying at 1%, calling, emailing and ignored.

By Month 1, Y2, instead of paying down to $631,268 my PB was $651,000 & change! Mozilo was disgraced, CW crashed, he survived dozens of lawsuits including by the CA Attorney General, but retired to his mansion unscathed and not 1 day in jail, to this date!

Bank of America took over servicing and they refused to do anything to remedy the situation. My state, Maryland, has a neutered Commissioner of Financial Regulation, laws written by banking lobbyists to strip jurisdiction from our state gov’t over any bank or chain of banks (thanks reagan!) not chartered here. And who would charter here since that protection was taken away from Marylanders?!

Our CFPB- Consumer Financial Protection Board wouldn’t touch it. Since inception, repubs have underfunded/understaffed it and whittled away at its purview. Sickening. I’ve paid down the under $400k but that $20,000 difference, Y1, still haunts me. Welcome again to the ‘Land of the Free’. Freedom of Speech. And lobbing is freedom of speech. ‘Campaign contributions’ congressional/senatorial junkets and use of oceanside condos and yachts – ‘Freedom of Speech’.

I continue to search online for any class action or other event addressing one of the most notorious scams I’ve ever heard of, with no luck. No one to turn to including my reps in the House and Senate.

I would love to hear from someone who knows if any of the $Trillions in TARP Federal $Relief funding made its way past the big banks, Wall Street, BIG: Oil, Pharma, Airlines, etc. and trickled down to individual homeowner/borrower victims. ?? (17 years later- I still have my original hand notes, that email, and supporting documents. But, I did trust Mozilo & Rizzotto and let my Rescission period lapse – my crime against my own finances and family!)

Sebastian ….. Thank you.